We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Green, ethical, energy issues in the news

Comments

-

theharebreaks said:NedS said:Netexporter said:I gather solar will be compulsory on all new builds in future.Although that would be progress, at least in helping reduce bills for homeowners, without battery storage it will only further exacerbate an already overstretched grid by increasing the midday over supply saturation. Without battery storage to shift some of that oversupply to offset/reduce the evening peak, it just makes things worse from a grid perspective. Solar and some form of BESS really need to go hand in hand, and how effective will solar be in reducing the energy bills of typical households once SEG rates fall off a cliff due to oversupply from all this additional solar. Solar makes far less sense without high SEG rates and/or battery storage.

In terms of the midday over supply. Does anyone know if any systems exist, to say only charge batteries during the peak, while also meeting the house demand? During the summer my battery would be fully charged by around 10am, with my system exporting the rest of the day. I would be more than happy to have my battery charge say from midday onwards during the peak solar generation perdiod, as long as the features were available and it did not financially disadvantage me. This would mean that during the early morning period all my generation is exporting (after meeting house demand) rather then charging my battery, with the battery being charged midday onwards, reducing the export to the grid during peak generation. No idea what would be involved in terms of updates to inverter/battery systems to allow setup.Yes, many batteries can be set up in this way. You would need to consult your documentation, but as you say such operation would net you the same amount but be more beneficial to the local grid.If SEG payments change in the future to pay different amounts at different times of the day, it may become financially beneficial to store as much as you can during the day when export rates may be low and export later when rates are higher, such as is already the case with tariffs like Octopus Flux where they reward you for exporting when the grid most needs it.I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.2 -

NedS said:Although that would be progress, at least in helping reduce bills for homeowners, without battery storage it will only further exacerbate an already overstretched grid by increasing the midday over supply saturation.Whilst more battery storage will no doubt be needed, and that seems to be happening anyway as costs come down, other things will no doubt help, especially if pricing mechanisms are altered. Use of timeswitches to kick off laundry appliances, maybe even increased use of AC particularly in big cities, don't forget the batteries in electric cars, and so forth.I'm on Agile so aware of my usage and also have PV. There's a learning curve in having both of those but more widespread changing customer behaviours may well help as well in the future. I've an EV as well, so will be using V2L tomorrow evening for cooking as the price will be about 38p and charged last night at around 11 to 13p.4

-

I was going to post this on the BEV news thread, as the news that China has hit 50% BEV for heavy truck sales is astonishing. Note, author said Dec 2026, but meant 2025 and is revising.

But, as I read on, the article (as per title) is far broader, looking at how the transition away from FF's may be sooner/faster than assumed.

Lots of paragraphs that could be posted to summarise, but in truth, too many. So I've just copied a few to give an idea of the article, but really worth a read as thnigs start to transition faster than expected.The Assumptions That Broke: China, India, and the End of Fossil Growth Models

The idea that heavy freight would be the last redoubt of diesel has been repeated for decades, often with confidence and rarely with evidence. In December 2026, that idea finally collapsed. Battery electric heavy duty trucks crossed 50% of new sales in China, a segment that had long been treated as immovable because of weight, range, duty cycles, and the presumed need for liquid fuels. This was not a pilot program, a niche urban category, or a short term policy artifact. It was a market-wide shift in the most energy-intensive road transport segment in the world’s largest vehicle market. If battery electric trucks can dominate new sales in China at that scale, then many of the assumptions that have shaped global energy debates are no longer fit for purpose.Fuel imports told the same story. Coal imports into China fell around 10% year on year even as domestic production barely inched up. LNG imports declined by low double digit percentages, roughly 10% to 15% depending on the data source, despite years of projections that gas would surge as a bridge fuel. Crude oil imports grew modestly, but that growth was increasingly disconnected from transport fuel demand and tied more closely to petrochemicals and exports. Diesel demand, in particular, came under pressure as efficiency improved and electrification expanded. Remember, this is against a backdrop of 5% growth in GDP, so this is not a story of economic malaise, but economic restructuring.China crossing the 50% threshold for battery electric heavy duty trucks in December 2026 did not happen because it was politically fashionable. It happened because the economics flipped and the system was ready. India is following a similar path with its own characteristics and constraints. The uncomfortable possibility for Western analysts is that some of the assumptions long applied to China and India are now obsolete, while assumptions about the pace and difficulty of transition in the West may be aging just as quickly.

Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.6 -

From that same article:It’s worth drawing out the nuclear vs renewables comparison. Since 2014 I’ve been tracking the natural experiment of nuclear vs renewables in China. It’s a natural experiment because it’s running in the real world. It’s a good one for the west to assess because the constraints that western nuclear advocates claim are blocking sensible nuclear barely exist in China: the country has nuclear generation as a national strategy that is nationally funded, the ability to override local concerns, and no real equivalent of the western environmental movement that grew out of the hippies and peaceniks of the 1960s and 1970s. The country has had a nuclear generation program for close to 50 and a wind and solar program for about 20 years, yet wind and solar are outstripping nuclear radically. 2025 wasn’t an especially big year for hydroelectric in China, but it outstripped nuclear too. The country, despite the narrative about China’s massive nuclear generation build out, only managed to connect a single 1.1 GW nuclear reactor to the grid last year. China’s decarbonization will be based on wind, solar and water, not nuclear, which merely plays a helping hand at still significantly less than 2% of grid capacity.Here's the chart that goes with the text (please let me know if you can't see it):

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 37 MWh generated, long-term average 2.6 Os.3 -

@QrizB can’t see it , unless I use quote your post, then it disappears when i reply ???

https://cleantechnica.com/wp-content/uploads/2026/01/Cumulative-Additional-TWh-Generation-Per-Year-in-China-1.png

4.8kWp 12x400W Longhi 9.6 kWh battery Giv-hy 5.0 Inverter, WSW facing Essex . Aint no sunshine ☀️ Octopus gas fixed 5.07 + Octopus Intelligent Flux leccy

CEC Email energyclub@moneysavingexpert.com0 -

QrizB said:From that same article:It’s worth drawing out the nuclear vs renewables comparison. Since 2014 I’ve been tracking the natural experiment of nuclear vs renewables in China. It’s a natural experiment because it’s running in the real world. It’s a good one for the west to assess because the constraints that western nuclear advocates claim are blocking sensible nuclear barely exist in China: the country has nuclear generation as a national strategy that is nationally funded, the ability to override local concerns, and no real equivalent of the western environmental movement that grew out of the hippies and peaceniks of the 1960s and 1970s. The country has had a nuclear generation program for close to 50 and a wind and solar program for about 20 years, yet wind and solar are outstripping nuclear radically. 2025 wasn’t an especially big year for hydroelectric in China, but it outstripped nuclear too. The country, despite the narrative about China’s massive nuclear generation build out, only managed to connect a single 1.1 GW nuclear reactor to the grid last year. China’s decarbonization will be based on wind, solar and water, not nuclear, which merely plays a helping hand at still significantly less than 2% of grid capacity.Here's the chart that goes with the text (please let me know if you can't see it):

Yes, and thanks for posting as it reinforces my own understanding of the value and need of new nuclear.East coast, lat 51.97. 8.26kw SSE, 23° pitch + 0.59kw WSW vertical. Nissan Leaf plus Zappi charger and 2 x ASHP's. Givenergy 8.2 & 9.5 kWh batts, 2 x 3 kW ac inverters. Indra V2H . CoCharger Host, Interest in Ripple Energy & Abundance.2 -

debitcardmayhem said:@QrizB can’t see it , unless I use quote your post, then it disappears when i reply ???OK, here's it shared a different way (using MSE's own hosting rather than linking from CleanTechnica):Is that visible now?

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 37 MWh generated, long-term average 2.6 Os.2 -

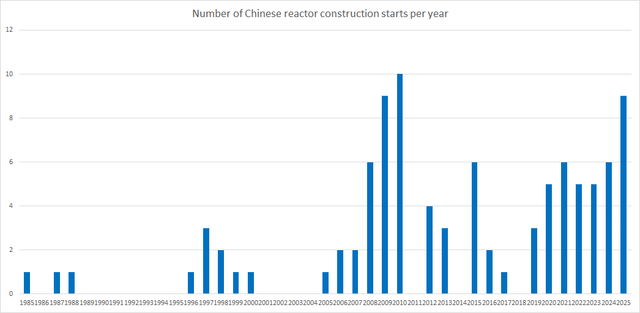

It's worth noting that reactor construction has picked up again in China in the last few years with construction starting on 9 new reactors in 2025, 6 in 2024, 5 in 2023, 5 in 2022 and 6 in 2021. So the lack of new reactors coming online recently is a legacy of the patchy starts in the years following the Fukushima disaster. The first reactors started in 2019 and after are now coming online so that lull is ending (it's recently taken China 5-6 years typically from announcing construction start to bringing a reactor online).

It doesn't change the fact that solar and wind are going to contribute a lot more electricity than nuclear in China, but the the lack of new reactors coming online isn't going to be typical for the next years.

Another thing that is striking is just how much China dominates new nuclear, much more than new solar and wind. China has almost twice as much new nuclear capacity under construction (41 GW) than the rest of the world put together (27 GW)! Second is India with just 4.7 GW, and India takes a lot longer to build it's reactors so the difference is even more stark. I think nuclear, like other megaprojects (high speed rail, large hydroelectric dams etc) is something that China's economic system is just much, much better at building, and therefore of less relevance to what is possible in the rest of the world.Solar install June 2022, Bath

4.8 kW array, Growatt SPH5000 inverter, 1x Seplos V3 battery 15.2 kWh, 1x Seplos V4 battery 16.1 kWh.

SSW roof. ~22° pitch, BISF house. 12 x 400W Hyundai panels. Hyundai Kona 64 kWh EV.2 -

THe Martyn1981 said:

I would have thought there would be much less politics/preference/FUD when it comes to choosing trucks, all the above being trumped by commercial logic, so surely we should expect to see the same thing happening in all markets?I was going to post this on the BEV news thread, as the news that China has hit 50% BEV for heavy truck sales is astonishing. Note, author said Dec 2026, but meant 2025 and is revising.

But, as I read on, the article (as per title) is far broader, looking at how the transition away from FF's may be sooner/faster than assumed.

Lots of paragraphs that could be posted to summarise, but in truth, too many. So I've just copied a few to give an idea of the article, but really worth a read as thnigs start to transition faster than expected.The Assumptions That Broke: China, India, and the End of Fossil Growth Models

The idea that heavy freight would be the last redoubt of diesel has been repeated for decades, often with confidence and rarely with evidence. In December 2026, that idea finally collapsed. Battery electric heavy duty trucks crossed 50% of new sales in China, a segment that had long been treated as immovable because of weight, range, duty cycles, and the presumed need for liquid fuels. This was not a pilot program, a niche urban category, or a short term policy artifact. It was a market-wide shift in the most energy-intensive road transport segment in the world’s largest vehicle market. If battery electric trucks can dominate new sales in China at that scale, then many of the assumptions that have shaped global energy debates are no longer fit for purpose.Fuel imports told the same story. Coal imports into China fell around 10% year on year even as domestic production barely inched up. LNG imports declined by low double digit percentages, roughly 10% to 15% depending on the data source, despite years of projections that gas would surge as a bridge fuel. Crude oil imports grew modestly, but that growth was increasingly disconnected from transport fuel demand and tied more closely to petrochemicals and exports. Diesel demand, in particular, came under pressure as efficiency improved and electrification expanded. Remember, this is against a backdrop of 5% growth in GDP, so this is not a story of economic malaise, but economic restructuring.China crossing the 50% threshold for battery electric heavy duty trucks in December 2026 did not happen because it was politically fashionable. It happened because the economics flipped and the system was ready. India is following a similar path with its own characteristics and constraints. The uncomfortable possibility for Western analysts is that some of the assumptions long applied to China and India are now obsolete, while assumptions about the pace and difficulty of transition in the West may be aging just as quickly.I think....1 -

Any links where the details have been shared? WE might like to add additional solar and batteries and might qualify as low income but previously had an EPC that wasn't bad enough to get a grant.gefnew said:UK households to get £15bn for solar and green tech to lower energy bills - BBC News

Seems like it will be a costly effort so the sham companies win again.I think....0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards