We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Early-retirement wannabe

Comments

-

It was a fairly simple statement for someone withdrawing 6% and ending up on their starting figure. For a 50/50 (US Centric) portfolio at nearly -11% it was the second largest drawdown in the last 20 years. It was about -24% for a 80/20 global portfolio and also the second largest. We all can expect worse in future but for someone like me who will be mainly relying on a SIPP for retirement income, it is a as good a stress test as any I hope to (not) have.BritishInvestor said:

"You have done well to come through one of the worst drawdown periods in the history "nirajn123 said:

You have done well to come through one of the worst drawdown periods in the history and so early in your drawdown journey, fair to say the central bankers deserve huge credit. 6% withdrawal is certainly higher than what I am targeting myself but as long as it works for you in the long term good for you!gadgetmind said:Dunno if anyone is interested, but I took my 1st pension payment from my SIPP in November 2018, have now taken 26 payments at a rate of just over 6% pa, and have 2.9% more in my pot than when I started. It peaked at 6.5% up in August 2019 (slightly higher late January 2020 but I only record once per month) and troughed at -10% in April 2020 as lockdown one started. I'm at a 50:50 equity to bond ratio, with rebalancing twice per year as I have to sell something to get enough cash for another six months' of payments. ISTR on one occasion doing a small purchase too but would have to check my records.

Balanced portfolios are a good thing!

If you don't mind sharing what do you use for the 50/50 portfolio? Some one decision fund or DIY of all world equity + global aggregate bonds?

It depends how you define worst. In terms of retirement portfolio sustainability, it was insignificant.0 -

This book has got *lots* of charts and I really don't think it would work too well on a Kindle.barnstar2077 said:It is a shame there isn't a kindle version available though. I use the app on my tablet so I can change the font size to something that doesn't give me eye strain.I am not a financial adviser and neither do I play one on television. I might occasionally give bad advice but at least it's free.

Like all religions, the Faith of the Invisible Pink Unicorns is based upon both logic and faith. We have faith that they are pink; we logically know that they are invisible because we can't see them.2 -

I'm pleased to say that I went 95% passive/trackers well over a decade ago. I've had numerous arguments with people hereabouts (some of whom I suspect work in the fund industry) with their arguments often boiling down to "No-one has ever gone wrong with Woodford, and look how much better than your trackers he is!"nirajn123 said: Moved away from active after the Woodford saga.

Quite.I am not a financial adviser and neither do I play one on television. I might occasionally give bad advice but at least it's free.

Like all religions, the Faith of the Invisible Pink Unicorns is based upon both logic and faith. We have faith that they are pink; we logically know that they are invisible because we can't see them.2 -

Marine_life said:I would like to create a topic (don't see it at the moment - other than the NUMBER thread).

Who is aiming for early retirement (or who has retired early already)? Hopefully me @ 55 and the OH @ 60 (currently 42 and 41 respectively -she wants to work longer)

When did you begin planning and what drove the decision? Realising that we didn't need a big house in a 'posh' area, and, with the kids leaving home now, we can move to a 'smaller' or 'cheaper' area that is near the best schools etc.

What is the strategy for getting there? mortgage paid off in 5 years (fingers crossed), already have a pension paying £12,000 per year till 55, then it'll increase to around £20,000 then with RPI or whatever is being used then. Paying extra into a second career pension so to provide about £4-5k a year. OH pension will pay around £15,000 per year.

How much of a relative decline in income are you prepared to take / did you take? will be about 55% drop

What are your main concerns? getting bored!

For those already in early retirement - how is it progressing? What have been the good and bad surprises (financial and otherwise)?30th June 2021 completely debt free…. Downsized, reduced working hours and living the dream.1 -

I think you forgot to make a point - for me tax and safe withdrawal planning is a big part of the number and entirely consistent with OP. I'm sorry if you disagree, but Marine_life hasn't been seen for a while and I think it reasonable for threads to follow where the wind blows without attracting tut-tutting Dolores Umbridge styleI think I saw you in an ice cream parlour

Drinking milk shakes, cold and long

Smiling and waving and looking so fine0 -

Over 10 years after my first post in this thread (with annual updates every April since then), this will hopefully be the last update at the start of a financial year before taking early retirement

") Quick reminder, myself and my wife are now 43 with no children. We plan to retire around Christmas this year, aged 44. This is quite a long and analytical post, as I have comprehensively updated analysis to ensure everything is taken into account accurately.Expenditure over the last year has been lower than previous years at 15% of gross household income (usually about 20%), which is not a surprise given COVID restrictions. We did manage one trip away for 12 days in August 2020, traveling through France, Spain and Gibraltar but that was all, and expenditure on UK activities has been very limited.

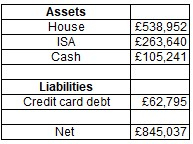

Quick reminder, myself and my wife are now 43 with no children. We plan to retire around Christmas this year, aged 44. This is quite a long and analytical post, as I have comprehensively updated analysis to ensure everything is taken into account accurately.Expenditure over the last year has been lower than previous years at 15% of gross household income (usually about 20%), which is not a surprise given COVID restrictions. We did manage one trip away for 12 days in August 2020, traveling through France, Spain and Gibraltar but that was all, and expenditure on UK activities has been very limited. The chart above shows the strategy up to 2015/16 was to focus on pension saving, putting all income which would be subject to higher rate tax into pensions. In 2016/17 I wanted more liquidity, so didn't focus much on either pensions or ISAs. From 2017/18 the focus has been on ISA saving, and our mortgage was paid off early in 2020/21. Note that both my wife and I are in Defined Benefit pension schemes, and the chart above does not show the employer contribution, only individual contributions. We also inherited around £60K in 2020/21, which isn't included in the chart above - this was part of the reason I prioritised pension and ISA over debt repayment, ensuring that if an inheritance happened it could be put to good use whenever it occurred and would not result in unwrapped assets.Our annual household consumption (commonly referred to as The Number on other threads) - measured as a residual after taking the major categories shown above from gross household income - has averaged about £28-29,000 (adjusted by price change to bring to current year, and also tested by adjusting for earnings growth for sensitivity).Current balance sheet, excluding pensions, is below. Next week £40K of the cash balance will go to ISA. The credit card liabilities are all 0%, so the cash balance is now just conventional (albeit not very profitable) Stoozing. Previously this costless borrowing (it was all nil-fee, 0% interest credit cards) was used to accelerate pension and ISA investment. Over the coming months all the credit cards will get paid off as the 0% offers come to an end and will not be renewed.Plan for the coming years is:

The chart above shows the strategy up to 2015/16 was to focus on pension saving, putting all income which would be subject to higher rate tax into pensions. In 2016/17 I wanted more liquidity, so didn't focus much on either pensions or ISAs. From 2017/18 the focus has been on ISA saving, and our mortgage was paid off early in 2020/21. Note that both my wife and I are in Defined Benefit pension schemes, and the chart above does not show the employer contribution, only individual contributions. We also inherited around £60K in 2020/21, which isn't included in the chart above - this was part of the reason I prioritised pension and ISA over debt repayment, ensuring that if an inheritance happened it could be put to good use whenever it occurred and would not result in unwrapped assets.Our annual household consumption (commonly referred to as The Number on other threads) - measured as a residual after taking the major categories shown above from gross household income - has averaged about £28-29,000 (adjusted by price change to bring to current year, and also tested by adjusting for earnings growth for sensitivity).Current balance sheet, excluding pensions, is below. Next week £40K of the cash balance will go to ISA. The credit card liabilities are all 0%, so the cash balance is now just conventional (albeit not very profitable) Stoozing. Previously this costless borrowing (it was all nil-fee, 0% interest credit cards) was used to accelerate pension and ISA investment. Over the coming months all the credit cards will get paid off as the 0% offers come to an end and will not be renewed.Plan for the coming years is:

- Leave employment on unpaid leave (if employer agrees, to give an option on return I don't expect to take but also enhanced death and ill-health pension should anything happen whilst traveling, else resign) around December, and sell house. We will be aged 44 then.

- Spend up to 3 years traveling. Starting with traveling the full length of Americas overland (something a bit like this trip, but doing it independently, and seeing a lot more of the USA and Caribbean). No time-frame, but roughly thinking 18 months. After that, see bits of east Africa, Indonesia, Australia and New Zealand and perhaps South Africa - basically things missed out on previous trips, or things my wife would like to see that I've seen before. I suspect that at some point we will get tired of constant travel and head back before three years is up - the longest I have ever continuously traveled is 13 months and my wife hasn't done any long trips. I have plans around staying in some areas for longer times to recharge, and also using technology to make travel more similar to home life which should mean travel is not as draining as my previous trips, eg, the 13 month trip never had more than 6 nights in the same bed whereas I expect to stay in a few places for several weeks.

- Buy house in rural central or north Wales upon return and have a conventional retirement - pets, voluntary work, fitness, sport, hobbies, etc.

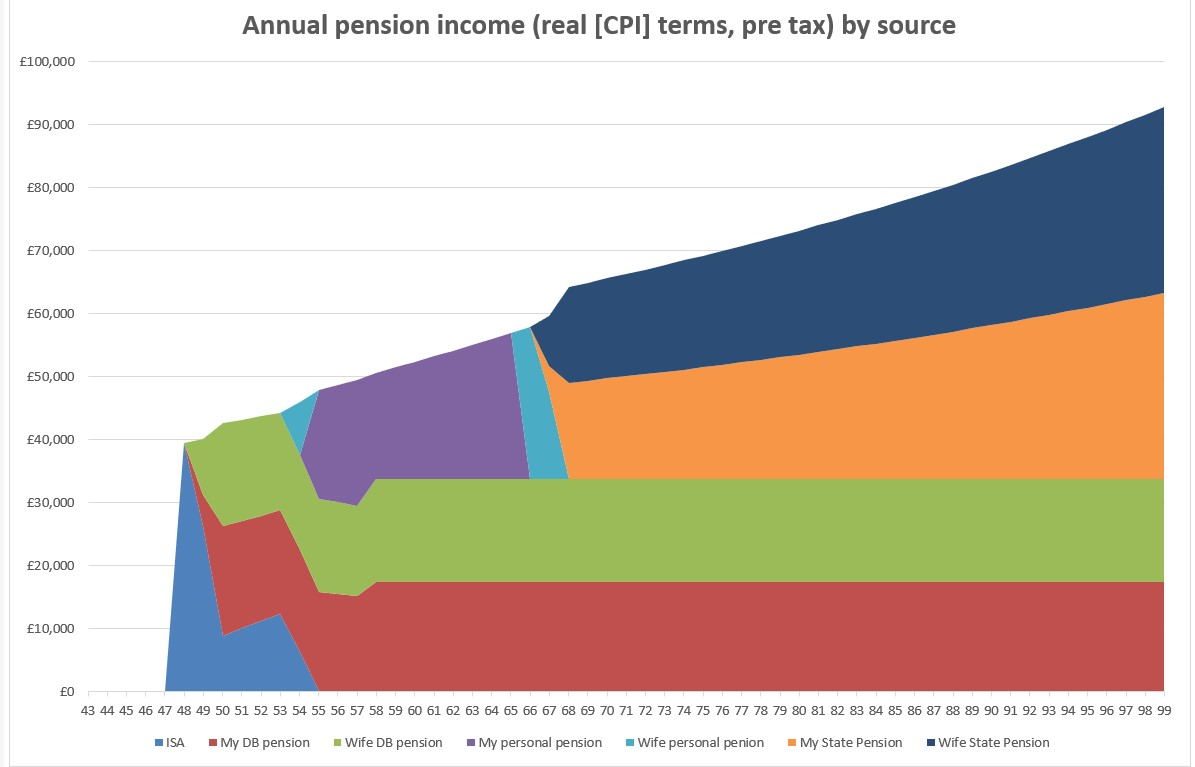

I'll use funds from selling current house for the travel, and augment the remainder of those funds with ISA funds to buy house in Wales upon return from travel. After that, retirement funding will look like this (note that as ages are not aligned with financial year some slight inconsistencies appear, eg, taking pension at age 49. This isn't the case and everything is modeled as coming into payment at the correct age, but showing age on the x-axis is more useful than financial year): Although the income composition changes a lot, the total income is quite consistent. The few small jumps represent changes in taxation (eg from untaxed ISA to taxed pension) - the income requirement prior to age 68 increases smoothly when looking at net income, as it is modeled as increasing in line with average earnings growth (3.8% p/a).Prior to age 50 all funding will coming from ISA. At age 50 we will both commence our DB pensions with protected minimum pension ages, and between 50-55 these pensions augmented with ISA funding will provide our income.From age 55 DC income will be available to augment income up to State Pension age (I assume we will have protected minimum pension age of 55 for these, based on content of current HMT minimum pension age increase consultation). We will initially draw on my wife's DC pension via UFPLS, as she is slightly older than me so will reach age 55 first. However, I have a bigger DC pot, so in subsequent years we will draw from my pot via UFPLS to balance resources (more tax-efficient in case of premature death of either partner to have balanced DC assets and use UFPLS rather than drawdown to avoid having unwrapped assets). Once my pot is largely depleted we will revert to wife's DC pension shortly before State Pension age.Note the growth (in real terms) of State Pension. This is based on Office for Budgetary Responsibility forecasts of the increase of Triple Lock in the long-run (4.2%, 0.36 percentage points above long-term average earnings). The up-rating policy results in very large State Pension amounts in the long-run, so the policy may well change at some future point despite the strength of the pensioner lobby group. Even under CPI uprating of State Pension we would have sufficient income so this policy change risk is of little concern to me.The key assumptions underpinning this are (short-term assumptions for next 3-4 years are taken from 2021 OBR Economic and Fiscal Outlook and Annex B of the 2020 OBR Economic and Fiscal outlook for long-term assumptions):

Although the income composition changes a lot, the total income is quite consistent. The few small jumps represent changes in taxation (eg from untaxed ISA to taxed pension) - the income requirement prior to age 68 increases smoothly when looking at net income, as it is modeled as increasing in line with average earnings growth (3.8% p/a).Prior to age 50 all funding will coming from ISA. At age 50 we will both commence our DB pensions with protected minimum pension ages, and between 50-55 these pensions augmented with ISA funding will provide our income.From age 55 DC income will be available to augment income up to State Pension age (I assume we will have protected minimum pension age of 55 for these, based on content of current HMT minimum pension age increase consultation). We will initially draw on my wife's DC pension via UFPLS, as she is slightly older than me so will reach age 55 first. However, I have a bigger DC pot, so in subsequent years we will draw from my pot via UFPLS to balance resources (more tax-efficient in case of premature death of either partner to have balanced DC assets and use UFPLS rather than drawdown to avoid having unwrapped assets). Once my pot is largely depleted we will revert to wife's DC pension shortly before State Pension age.Note the growth (in real terms) of State Pension. This is based on Office for Budgetary Responsibility forecasts of the increase of Triple Lock in the long-run (4.2%, 0.36 percentage points above long-term average earnings). The up-rating policy results in very large State Pension amounts in the long-run, so the policy may well change at some future point despite the strength of the pensioner lobby group. Even under CPI uprating of State Pension we would have sufficient income so this policy change risk is of little concern to me.The key assumptions underpinning this are (short-term assumptions for next 3-4 years are taken from 2021 OBR Economic and Fiscal Outlook and Annex B of the 2020 OBR Economic and Fiscal outlook for long-term assumptions):- Growth of 1% above CPI (after fees, so growth assumed to cover inflation and fees and give an additional 1% return) for ISA and DC pension

- CPI in line with Office for Budgetary Responsibility (OBR) forecasts, and 2% thereafter

- 0.75% return on cash savings, based on the interest rate of my saving account, and we will also purchase Premium Bonds with funds from house sale prior to travel.

- Cost of purchasing house in Wales (inc Land Transaction Tax and other moving costs) is £500,000 (increases by OBR house price change forecast in future years)

- We spend £60,000 per year traveling (increases in line with OBR earnings forecast in future years). This was tricky to estimate, but based on previous holidays and websites of people who have done similar, I am confident this will be sufficient.

- Our spending requirement is £37,403 p/a after we return from travel (value as at 2021/22, increases in line with OBR earnings forecast in future years up to State Pension age and by CPI thereafter). This is based on the highest annual expenditure on consumption in all years since 2013/14, with that amount revalued by average earnings to present day. The main expenditure changes will be having to ensure my wife gets 17 National Insurance qualifying years (up to £800 per year, I need some too, but only about 9 years, so will purchase these after age 55 when DC pension is available), and much higher council tax (currently £1,888 p/a likely to be a bit over £3,000 p/a). That suggests a target of about £31,000 p/a should be sufficient based on average consumption over last 8 years, so £37,403 should be very comfortable. Note that it is important when retiring very early to think about income relative to earnings, else what may seem like a high income in price terms at retirement will get eroded relative to wider standard of living.

- Income tax thresholds are frozen to 2025/26 and increase by average earnings thereafter. Rates do not change.

- Our State Pension ages will be 68 (currently they are a bit below this, but I expect the increase to age 68 to be brought forward based on comments from govt. following the 2018 Cridland Review of State Pension age)

The modelling results in small amounts of ISA and DC pension being left, as well as 6 months of cash savings at all times. In practice, I expect to use less than allocated as assumptions are conservative, and if so some surplus will probably be used in lieu of State Pension which can then be deferred, effectively turning spare capital into guaranteed pension.I will also exchange some DB pension in return for enhanced survivor benefits (exchange included within figures in charts above), set to ensure whichever of us survives the other sees net income drop to 70% of the net household income as a couple. This is a bit above what equivalisation scales suggest (67%) so should be fine. If either of us die very early, the survivor will be much better off than this, so 70% is a worst-case, albeit most likely, scenario.In practice, our retirement date is now more dependent on COVID and international travel opening up than it is on the financials. If we cannot travel in early 2022 we will delay retirement until about June 2022 to take advantage of Personal Allowances in 2022/23. Once we reach age 55 everything should be very comfortable, but even the pre-55 period isn't very concerning really, not least due to having DB pension from age 50 available which should be fine even without any enhancement from ISA if necessary. We can also vary house funds quite a lot too if required, so plenty of caution in the assumptions along with flexibility in approach should it be needed.23 - Leave employment on unpaid leave (if employer agrees, to give an option on return I don't expect to take but also enhanced death and ill-health pension should anything happen whilst traveling, else resign) around December, and sell house. We will be aged 44 then.

-

love this detailed post. want to go back and have a proper read, as I am thinking I will learn a lot. well done on retiring so early. what field of employment are you and your wife in?1

-

savingmore said:love this detailed post. want to go back and have a proper read, as I am thinking I will learn a lot. well done on retiring so early. what field of employment are you and your wife in?I like planning, arguably I do too much of it but I find it quite fun, it isn't a chore, and knocking all the stuff together in the post above only takes a day each year updating well-established spreadsheets. Going into such detail also helps unearth various things I haven't considered, eg, until this year I hadn't given much thought to survivor benefits, but now that has all been fully researched and a few adjustments to the plan factored in to optimise that area. Thinking through and developing the detailed assumptions is very helpful for ensuring the plan is robust with alternative assumptions should things not develop as intended (as well as being very educational about exactly what is going on in taxation and pension policy).My wife and I are both Civil Servants. My wife had an early career in academia, then moved into the Civil Service where we met a few years later. I've only ever worked in the Civil Service. In anticipation of comments about the generosity of public sector pensions, they are very generous (especially the older schemes), but we have also both saved several hundreds of thousands of pounds into pensions over and above standard contribution rates to increase the Defined Benefit pension and also build up DC pension for flexibility and to smooth out income (DC essentially substitutes for State Pension between age 55-68 in our plan).2

-

Thanks for posting such a detailed post @hugheskevi. Fascinating reading and plenty of useful information I can incorporate into my own planning.1

-

Always good to look back at old posts, so here's an update from me, nearly 7 years on:bownyboy said:Great thread. Here's my answers:

Who is aiming for early retirement (or who has retired early already)?

Looking to retire by 55 (or at least drastically reduce hours work and remove the daily commute)

When did you begin planning and what drove the decision?

Had a stakeholder pension in 2000 but hardly contributed to it. It was October last year that I finally started to put a plan in place, realising I wasn't getting any younger and was probably at peak earning power so should start maxing out pension and investments as quickly as possible.

What is the strategy for getting there?

I'm currently 41, so I have 14 years. I've researched 'The Number' which for us will be £24k a year. Am saving £2k gross a month into personal pension with Aegon (transferred over my stakeholder to them and halved the AMC to 0.5%) Also saving £1k a month into Stocks & Shares ISA with Vanguard Lifestyle 60% acc.

Between me and my partner we already have £109k in S&S ISAs and Personal Pensions. £500k is the first target which should be reached in 8 years with 5% growth and 2.5% inflation.

After that another 6 years of contributions would give us approx £900k. However life happens and I've no idea if I can sustain this level of contributions.

I'm just throwing as much as I can as quickly as I can without impacting quality of life now too much!

How much of a relative decline in income are you prepared to take / did you take?

Quite substantial, probably 70% drop We enjoy the simple things in life and live pretty frugally.

What are your main concerns?

Government interference and changes to pension rules.

Looking to retire this year when my current contract finishes at the beginning of September, I'll be 49 so 6 years earlier than my original estimate.

Our pot which consists of ISAs and SIPPs is currently at £710k and my estimate is that it will be around £780k by September. We reached £500k in 4 years not 8! Thanks to some incredible market returns and also the fact that I decided to go contracting which dramatically increased my income.

Our estimated living expenses steadily increased over the years from £2k a month to £2.5k and then around £3k which is where it is now. We see our expenses being higher initially as we want to do some slow travel (post covid). We had big plans for Central America and South East Asia, but we'll see how that pans out.

My wife has a full state pension of £9,338 due in 11 years and I'm currently at around £7.5k, but I'll continue voluntary NI contributions until I reach 35 years.

Things that helped us along the way:- Combing finances for that 'big picture' view; works for some not for others. For me it allowed us to optimise our savings, tax and ensure we chased lowest fees

- KISS; keep it simple. we use one platform with one SIPP and one ISA each. Both in Vanguard FTSE Global All Cap and Vanguard Total Bond Index split 75/25. We originally started out in Lifestrategy 60, but as we become more confident I decided to take more control and move into a 75/25 split and rebalance once a year

- A spreadsheet (of course!) I created a simple google sheet showing assets, minus liabilities along with 12 months for the year. I then forecast for the year based on some assumptions for growth, contributions and expenses. On the first of each month I update with actuals. Gives us a good focus on where we are aiming for at the end of the year. It also helped with any wobbles due to market drops as I could view all our historical data and see that dips where inevitable and that the trends were always upwards

- Going contracting and setting up a limited company. This gave us more flexibility with how we managed income as well as the bump in income contracting gave

- Getting a 3rd party to sanity check our plan. Originally I was thinking an IFA but decided against that approach for various reasons. Instead we had a chat with a well known personal finance blogger to get a second opinion on our approach which helped my wife feel more confident that we were on the right track (I take care of all the financial planning)

- Running the numbers in https://ficalc.app using variable percentage withdrawal showing 100% success rate using historical data

Feels good to finally be on the other side, if slightly dazed that we've got here!

early retirement wannabe12

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards