We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Early-retirement wannabe

Comments

-

Good point - I have never had that as an explicit benefitI’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

Similar for me.westv said:Now the Government has withdrawn the work from home guidance our company has said we can either do 3, 4 or 5 days in the office and the rest wfh or, in some cases, move to a full time wfh contract (with a reduction in benefits).

I'm not sure what to choose.

Before Covid I went down to London on Monday, stayed in a rented room and then came back home Friday evening. Doing it for 3 days would mean less time away but it would still be a large amount of money to pay out - something I haven't done for almost 18 months. Then again being in the office means interaction with my colleagues.

This would not be something I would want to do past 60 - in 18 months time. In fact, I was considering going at 59.

On the other hand a wfh contract would save me paying out for fares and room rent but I would have much less interaction with other team members. On the other hand it would be more sustainable post 60 and much easier financially to reduce my days worked if wanted.

Pre Covid I used to rent a room and went down Sun/Mon night for 3-4 days working in London. Sometimes 5.

Cost was pretty much fixed - an off peak return ticket to London, plus the room rental.

It's been a huge relief not to have to pay this for the last year plus, but there's a clear message that we will be expected 1-4 days a week in the office. Zero is not an option.

I have 2.5 to 3 years remaining, depending on the whims of SIPP returns etc.

I'll have to stump up a peak ticket and travel in a day (roughly 8.5 hrs travel, plus a full working day, plus any travel to client), or travel the night before and find a cheap hotel. The overall cost (vs pre Covid) is therefore not going to be much different, but without the permanence of a room with my things around. I rather baulk at the thought of renting a room to use 1-2 nights a week.

Sadly my friends and colleagues are either way out of London, or crammed full with young children, so I can't come to some sort of flexible arrangement.

I'd love to stop now, but need another 2.5 years to get to 55 and access my pension...0 -

If they are available on your route, have you tried Advance Purchase tickets? You are restricted to a specific service though. I use them and, for me, they are a lot cheaper than flexible tickets.ex-pat_scot said:westv said:Now the Government has withdrawn the work from home guidance our company has said we can either do 3, 4 or 5 days in the office and the rest wfh or, in some cases, move to a full time wfh contract (with a reduction in benefits).

I'm not sure what to choose.

Before Covid I went down to London on Monday, stayed in a rented room and then came back home Friday evening. Doing it for 3 days would mean less time away but it would still be a large amount of money to pay out - something I haven't done for almost 18 months. Then again being in the office means interaction with my colleagues.

This would not be something I would want to do past 60 - in 18 months time. In fact, I was considering going at 59.

On the other hand a wfh contract would save me paying out for fares and room rent but I would have much less interaction with other team members. On the other hand it would be more sustainable post 60 and much easier financially to reduce my days worked if wanted.

I'll have to stump up a peak ticket and travel in a day (roughly 8.5 hrs travel, plus a full working day, plus any travel to client), or travel the night before and find a cheap hotel. The overall cost (vs pre Covid) is therefore not going to be much different, but without the permanence of a room with my things around. I rather baulk at the thought of renting a room to use 1-2 nights a week.2 -

It's a possibility - my "pre Covid" model was cheap advance offpeak - roughly £45 - £65 return per week, if I caught the late unpopular trains. I used to stay v late in the office, then get the last train to York.westv said:

If they are available on your route, have you tried Advance Purchase tickets? You are restricted to a specific service though. I use them and, for me, they are a lot cheaper than flexible tickets.ex-pat_scot said:westv said:Now the Government has withdrawn the work from home guidance our company has said we can either do 3, 4 or 5 days in the office and the rest wfh or, in some cases, move to a full time wfh contract (with a reduction in benefits).

I'm not sure what to choose.

Before Covid I went down to London on Monday, stayed in a rented room and then came back home Friday evening. Doing it for 3 days would mean less time away but it would still be a large amount of money to pay out - something I haven't done for almost 18 months. Then again being in the office means interaction with my colleagues.

This would not be something I would want to do past 60 - in 18 months time. In fact, I was considering going at 59.

On the other hand a wfh contract would save me paying out for fares and room rent but I would have much less interaction with other team members. On the other hand it would be more sustainable post 60 and much easier financially to reduce my days worked if wanted.

I'll have to stump up a peak ticket and travel in a day (roughly 8.5 hrs travel, plus a full working day, plus any travel to client), or travel the night before and find a cheap hotel. The overall cost (vs pre Covid) is therefore not going to be much different, but without the permanence of a room with my things around. I rather baulk at the thought of renting a room to use 1-2 nights a week.

Now the offices are strictly open for business hours, owing to the need to deep clean.

The Advance ticket prices seem very few in number and very highly priced - £120+ for equivalent journeys - and a peak fare is £150+. I'm sure it will settle down eventually, but it's not looking cheap for the immediate future!

My ideal is almost 100% wfh/wf client. Let's see how that starts to coalesce.0 -

Nothing is impossible. You could use a mortgage to support spending now and pay back using some of your tfls at 55 if your fund is big enough and the only problem is the 55 access window.ex-pat_scot said:

Similar for me.westv said:Now the Government has withdrawn the work from home guidance our company has said we can either do 3, 4 or 5 days in the office and the rest wfh or, in some cases, move to a full time wfh contract (with a reduction in benefits).

I'm not sure what to choose.

Before Covid I went down to London on Monday, stayed in a rented room and then came back home Friday evening. Doing it for 3 days would mean less time away but it would still be a large amount of money to pay out - something I haven't done for almost 18 months. Then again being in the office means interaction with my colleagues.

This would not be something I would want to do past 60 - in 18 months time. In fact, I was considering going at 59.

On the other hand a wfh contract would save me paying out for fares and room rent but I would have much less interaction with other team members. On the other hand it would be more sustainable post 60 and much easier financially to reduce my days worked if wanted.

Pre Covid I used to rent a room and went down Sun/Mon night for 3-4 days working in London. Sometimes 5.

Cost was pretty much fixed - an off peak return ticket to London, plus the room rental.

It's been a huge relief not to have to pay this for the last year plus, but there's a clear message that we will be expected 1-4 days a week in the office. Zero is not an option.

I have 2.5 to 3 years remaining, depending on the whims of SIPP returns etc.

I'll have to stump up a peak ticket and travel in a day (roughly 8.5 hrs travel, plus a full working day, plus any travel to client), or travel the night before and find a cheap hotel. The overall cost (vs pre Covid) is therefore not going to be much different, but without the permanence of a room with my things around. I rather baulk at the thought of renting a room to use 1-2 nights a week.

Sadly my friends and colleagues are either way out of London, or crammed full with young children, so I can't come to some sort of flexible arrangement.

I'd love to stop now, but need another 2.5 years to get to 55 and access my pension...I think....5 -

michaels said:

It's certainly a possibility, although another healthy 2.5 to 3 years of earning would allow the pot to grow considerably.

Nothing is impossible. You could use a mortgage to support spending now and pay back using some of your tfls at 55 if your fund is big enough and the only problem is the 55 access window.ex-pat_scot said:

I'd love to stop now, but need another 2.5 years to get to 55 and access my pension...

I still have a healthy mortgage, so much of the TFLS is rather earmarked for it.1 -

4 months ago in my last update (3rd April 2021, a couple of pages back) I said:

The situation with COVID and North America has not improved as I had hoped. A US-UK air-corridor is still not in place, although the Canada-USA border is due to re-open in September for non-USA nationals. I had always penciled in 31st July as a 'Go / No go' decision date, and have had the rule that I won't anticipate anything that has not yet been announced (if not enacted) given how much anything COVID related changes.hugheskevi said:Plan for the coming years is: Leave employment on unpaid leave (if employer agrees, to give an option on return I don't expect to take but also enhanced death and ill-health pension should anything happen whilst traveling [for an assumed period of 3 years], else resign) around December, and sell house. We will be aged 44 then.So I have re-planned departure, with key dates now being:- Market house in mid/late February 2022 (apparently marketing house after February half-term is best time of year for my type of property)

- Set off traveling in mid May 2022, although this may be delayed depending on house sale.

- Last day of service at work after using leave is planned to be Monday 13th June (ensuring wife and I use Personal Allowance for 2022/23, get a NICs qualifying year, and take advantage of all the Bank Holidays and Privilege Days in April - June period as well as benefiting from being paid for the weekend)

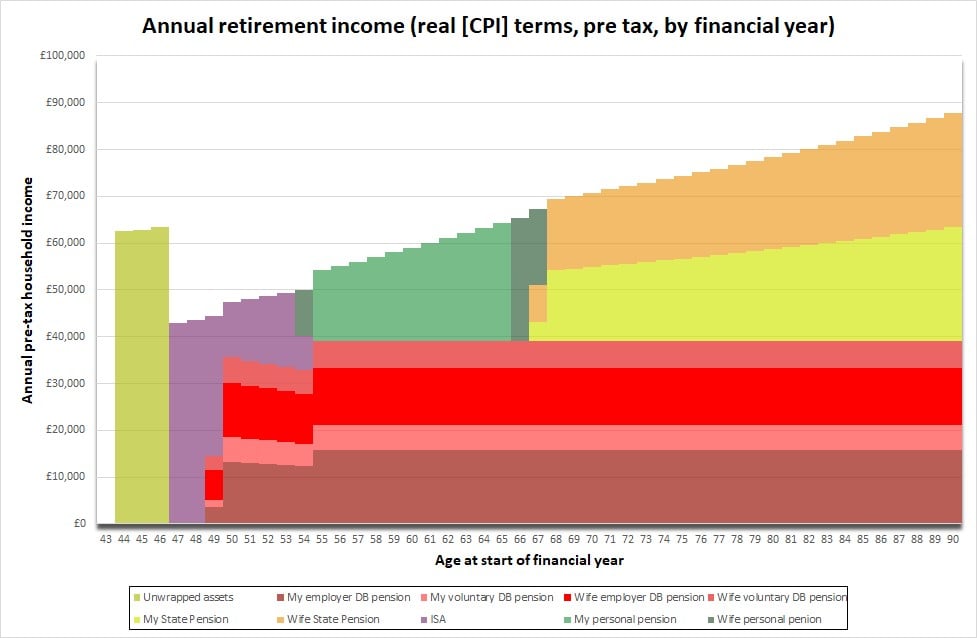

I've also re-planned finances a little, allocating the small extra amount arising from the delay across a variety of categories. So I have made a few tweaks to smooth things out (and improved presentation of the chart), which should deliver an annual net income of £41,400 which increases by forecast earnings growth (3.84%) to age 68 and by a bit more than prices (due to Triple Lock) from age 68. Survivor benefits will be at least 70% of combined income.I'm very relaxed by the delay, as it is always helpful to have extra resources to allocate, and it puts focus on each part of the plan to identify the weakest parts and what can be done to improve them. Although I hope further delays are not required, as there are diminishing returns to this exercise. Also, the revised plan just fits better in terms of when to sell house and leaving date 'efficiency' in terms of getting income tax free salary in 2022/23. The key period of uncertainty is between age 44 to age 57, with key assumptions being:

The key period of uncertainty is between age 44 to age 57, with key assumptions being:- Sale of current house yields around £530,000 after costs of sale

- Annual cost of travel for my wife and I will be a bit over £60,000 p/a and last for 3 years

- ISA returns of 3% p/a after charges (nominal terms)

- Unwrapped cash yields 0.75% (nominal terms)

- Inflation between 50-55 is important, as our DB pensions do not increase in this period. They are CPI-linked to age 50, and will get all inflation increases for the previous 5 years when we reach age 55 (but no backdated payment, just increase to future pension). Hence high inflation in that period would reduce available funds in real terms.

- I can access DC pension from age 55 - either via my existing scheme having a protected minimum pension age of 55, or being able to make a partial transfer before April 2023 of sufficient funds for the period 55-57 to a scheme that has a protected minimum pension age.

Based on the above, the outcome would be funds available for house purchase (including costs and furnishing) after returning from travel of around £525,000. Any surplus or deficit arising from variance in assumptions above will affect this figure, with limited ability to 'borrow' some funding from ISAs intended for funding for future years if desired.The rate of return on DC pension is increasingly becoming less important. The chart above requires a growth rate of 2.5% after fees (nominal) which should be routine with low volatility investments. So the period after 57 is unlikely to pose any issues, given receipt of a decent amount of DB pension plus the flexibility of DC.I've also been short-listing places to visit on the first part of our trip, although a lot of the trip will be researched and planned whilst on the road so I'm only planning north and central America and the Caribbean in advance of leaving. These are just the 'big ticket' things to see, and we will visit other things in areas as we move overland between the things we want to visit. It now looks like starting in Calgary / Edmonton area, visiting the nearby National Parks then heading up into Alaska in the summer months of 2022. 4

4 -

So, you haven't given it much thought then! : )hugheskevi said:4 months ago in my last update (3rd April 2021, a couple of pages back) I said:

The situation with COVID and North America has not improved as I had hoped. A US-UK air-corridor is still not in place, although the Canada-USA border is due to re-open in September for non-USA nationals. I had always penciled in 31st July as a 'Go / No go' decision date, and have had the rule that I won't anticipate anything that has not yet been announced (if not enacted) given how much anything COVID related changes.hugheskevi said:Plan for the coming years is: Leave employment on unpaid leave (if employer agrees, to give an option on return I don't expect to take but also enhanced death and ill-health pension should anything happen whilst traveling [for an assumed period of 3 years], else resign) around December, and sell house. We will be aged 44 then.So I have re-planned departure, with key dates now being:- Market house in mid/late February 2022 (apparently marketing house after February half-term is best time of year for my type of property)

- Set off traveling in mid May 2022, although this may be delayed depending on house sale.

- Last day of service at work after using leave is planned to be Monday 13th June (ensuring wife and I use Personal Allowance for 2022/23, get a NICs qualifying year, and take advantage of all the Bank Holidays and Privilege Days in April - June period as well as benefiting from being paid for the weekend)

I've also re-planned finances a little, allocating the small extra amount arising from the delay across a variety of categories. So I have made a few tweaks to smooth things out (and improved presentation of the chart), which should deliver an annual net income of £41,400 which increases by forecast earnings growth (3.84%) to age 68 and by a bit more than prices (due to Triple Lock) from age 68. Survivor benefits will be at least 70% of combined income.I'm very relaxed by the delay, as it is always helpful to have extra resources to allocate, and it puts of focus on each part of the plan to identify the weakest parts and what can be done to improve them. Although I hope further delays are not required, as there are diminishing returns to this exercise. Also, the revised plan just fits better in terms of when to sell house and leaving date 'efficiency' in terms of getting income tax free salary in 2022/23.The key period of uncertainty is between age 44 to age 57, with key assumptions being:- Sale of current house yields around £530,000 after costs of sale

- Annual cost of travel for my wife and I will be a bit over £60,000 p/a and last for 3 years

- ISA returns of 3% p/a after charges (nominal terms)

- Unwrapped cash yields 0.75% (nominal terms)

- Inflation between 50-55 is important, as our DB pensions do not increase in this period. They are CPI-linked to age 50, and will get all inflation increases for the previous 5 years when we reach age 55 (but no backdated payment, just increase to future pension). Hence high inflation in that period would reduce available funds in real terms.

- I can access DC pension from age 55 - either via my existing scheme having a protected minimum pension age of 55, or being able to make a partial transfer before April 2023 of sufficient funds for the period 55-57 to a scheme that has a protected minimum pension age.

Based on the above, the outcome would be funds available for house purchase (including costs and furnishing) after returning from travel of around £525,000. Any surplus or deficit arising from variance in assumptions above will affect this figure, with limited ability to 'borrow' some funding from ISAs intended for funding for future years if desired.The rate of return on DC pension is increasingly becoming less important. The chart above requires a growth rate of 2.5% after fees (nominal) which should be routine with low volatility investments. So the period after 57 is unlikely to pose any issues, given receipt of a decent amount of DB pension plus the flexibility of DC.I've also been short-listing places to visit on the first part of our trip, although a lot of the trip will be researched and planned whilst on the road so I'm only planning north and central America and the Caribbean in advance of leaving. These are just the 'big ticket' things to see, and we will visit other things in areas as we move overland between the things we want to visit. It now looks like starting in Calgary / Edmonton area, visiting the nearby National Parks then heading up into Alaska in the summer months of 2022.Think first of your goal, then make it happen!7 -

What is your exposure to house price inflation while you are out of the market - have you considered any specific investments to hedge this risk?

(I know we always look at this market and assume it is so high it can only go down/sideways and yet even with a pandemic it has been up over 10% in the last year, probably higher on retirement type properties (assuming these are 'retire to the country' type choice so your 525 would only buy a much smaller house than anticipated if this were to happen again whilst you were travelling)I think....1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards