We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Unenforceability & Template Letters II

Comments

-

Hi Nid,

As you know I've sent off 3 account dispute letters to 3 creditors and cancelled my dd to cccs. CCCS have since sent me an email and a text stating the dd has been returned unpaid and to ring them immediately.

Should I call them and tell them why I've cancelled it or just ignore them?

Yea, just let them know that the debts are unenforceable and you're not paying until such time they send compliant paperwork.also - I had what I thought was a £3.5k default balance with b'card/goldfish but when I got my equifax credit file, this debt wasn't showing? I've read the cag thread re the problems with goldfish/barclays and I'm hoping it may have been written off.

How old is it? If over 6 years (or at previous address) then it may just not be linked - also, worth confirming with Experian as well - but it doesn;t matter if they default you cos you'll get others (if not already)....

see below too....Is it possible that the debt is still owing but just not showing on my file with equifax?

Yes, not all creditors/dca's update the CRA's until they default you - or if you dispute the account they can temporarily remove the entry....Should I still send them the default letter or just leave things?

Leave things until they next write to you

2010 - year of the troll

2010 - year of the troll

Niddy - Over & Out :wave:

0 -

Hello again NID. I have another question which I'm sure you have already answered somewhere in this thread but I've been trawling through and can't find anything. Basically we now realise that a certain proportion of our debt is definitely enforceable and have taken the 1st steps towards sorting our huge mess out by setting up a meeting with a cccs counsellor (made contact with one through the forum). Anyway, what we really want to know is this: where do cccs counsellors stand on the issue of unenforecability? Should we tell the counsellor that we are going down this road for some of our pre 2007 debts or keep quiet about it? Or, once we embark on a DMP, should we be encompassing all of our debt? It's all a bit like a foreign language & we don't speak the lingo yet - but I'm so glad you do!

Many many thanks yet again, Pressers

Hiya

best to be honest with the counsellor so tell them you've sent CCA's and these came back ok, these did not. Lay your cards on the table - at the end of the day if the lender did in the future find the agreement then CCCS would need to amend the amounts payable to include them.

They are not anti unenforceability, nor are they pro unenforceability..... they will advise on your debt situation, not the enforceability of debts. 2010 - year of the troll

Niddy - Over & Out :wave:

0 -

Hi NID,

I today received a reply from barclays re my loan with them. They have sent the agreement with the prescribed terms intact, this looks like the agreement they sent me. However it does not have my or their signature on it even though their are spaces for them to go. Surely if they had the agreement (which I don't remember signing or sending back) they would send it with my signature on it. Also they have my old address on it, I had moved 5 months before the application.

Any advise?

Cheers

Hiya

Ok, so it sounds (from your post) that they have provided a recon - especially if it has the wrong address! So you're saying the address on the agreement was not your address until +5 months after you took the account?

Either way, send this off to them: 3. CCA Query 2010 - year of the troll

Niddy - Over & Out :wave:

0 -

I originally put this in a new thread but was advised that this is the best place to post and that there was a very kind person called NID who might be able to help

")

LOL - NID? Wonder who that is :whistle::whistle:

If you're a DCA then bugga off :rotfl:

I've responded to your own thread here: Unenforcable HSBC Credit Card. Advice Please but if you can stick to this thread as I spend most my time here.....

---I have had a credit card from HSBC since 2002.

I followed the advice on the Unenforcability Templates thread and sent all of the appropriate letters to HSBC. This is where I currently stand:

HSBC are usually quite good, can you confirm whether you have linked pages (terms) - i.e. they can send the CCA with additional pages, if so then it may not be unenforceable. However, lets assume for ease, they never.- Requested credit agreement.

- Sent reminder after 14 days

- Received "credit agreement" - Had my signature on it but none of the prescribed terms (interest rate etc).

- Sent "does not contain prescribed terms" letter and tell them that they have defaulted.

What you've done so far is correct :T- I cancel my direct debit

Good - just make sure you do not bank with HSBC or they will utilise RoSo (set off) and will dip into your bank account!- Reply from HSBC saying that they will not write off the debt as they claim that the credit agreement is valid

Of course they do They always do!- Received default notice

Ok, standard - is this the only one you have? If so, was it worth it for one default, you'll get no credit for a few years (default remains for 6 years!).... if you have others, have you CCA'd them too?- HSBC then take a monthly payment from my HSBC current account!

Perfectly normal and acceptable within the banking industry, it is called Right of Set off (RoSo) - see here: http://www.financial-ombudsman.org.uk/publications/ombudsman-news/40/40_setoff.htm- I phone and request a reversal, they say I have to put it in writing.

Save your stamp - they will not do it nor are they legally obliged to do it, forget this but move banks asap!This is where I currently stand. I am considering going to one of the unenforcability lawyers advertised on the internet as I don't know where to go and I don't want bailiffs on my doorstep.

Don't pay - you will get nowhere by paying! Regards to bailiffs, they will not turn up on your doorstep - you actually have more rights than they do! See here for details of what they can/can't do and how to respond to their letters/threats etc: Dealing with Bailiffs HarassmentWhere can I go from here?

See here: Unenforceability & Template Letters IIDid HSBC take the payment from my account illegally?

Nope - see here: http://www.financial-ombudsman.org.uk/publications/ombudsman-news/40/40_setoff.htmAm I in a grey area?

Nope - its black & white to me - the debt is unenforceable until such time HSBC provide a compliant agreement and associated terms of the account as one document (or linked).... therefore get a new bank account sorted asap!Are there any decent lawyers if I am unable to deal with this myself?

Do it yourself, link to my thread above.

Don't worry, you've done everything correctly so far.... 2010 - year of the troll

Niddy - Over & Out :wave:

0 -

Sir, you are simply brilliant

They did send a photocopy of the Terms and Conditions at time of signing with the "credit agreement". Does this count as the "aditional pages" (which I did not sign)?0 -

Sir, you are simply brilliant

They did send a photocopy of the Terms and Conditions at time of signing with the "credit agreement". Does this count as the "aditional pages" (which I did not sign)?

Seems so, although your signature should be on the prescribed terms page itself, if not then you can argue but no guarantee of unenforceability..... 2010 - year of the troll

Niddy - Over & Out :wave:

0 -

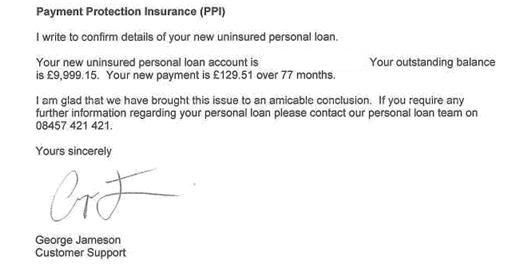

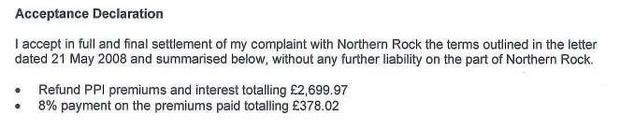

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock1.jpg

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock2.jpg

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock3.jpg

These are my so-called new 'agreements' with Northern Rock following a PPI refund.

If i CCA them, what do you think they would send?

I have just started a DMP and Northern Rock have probably just received my proposal, should i wait for their response on that before CCA'ing them, or just do it now?LBM - Jan'10

DMP Start - 01st March 2010 - Debt £31,614

Debts at Highest - £36k Mid Jan 2010

Debt Free Date 22nd December 2015!

DMP - Just do it, don't hesitate.0 -

never-in-doubt wrote: »Hiya

Ok, so it sounds (from your post) that they have provided a recon - especially if it has the wrong address! So you're saying the address on the agreement was not your address until +5 months after you took the account?

Either way, send this off to them: 3. CCA Query

Cheers NID. No it was my address 5 months before the application.0 -

-

nonnynonny wrote: »http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock1.jpg

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock2.jpg

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock3.jpg

These are my so-called new 'agreements' with Northern Rock following a PPI refund.

If i CCA them, what do you think they would send?

I have just started a DMP and Northern Rock have probably just received my proposal, should i wait for their response on that before CCA'ing them, or just do it now?

Hi

Can you please be more specific - what do you mean 'the new agreements' as a result of PPI challenge>? The original documents, should be sent to you - are the above links your original documents or copies assuming the new terms etc?

Please elaborate - quite a lot lol. I don't know wnaything about your past or what has happened to date etc. If you want me to check if the links are enforceable, then just ask - but your post is too confusing to decifer without expansion. 2010 - year of the troll

Niddy - Over & Out :wave:

0

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards