We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Failure to reply to CCA request - 1st credit

Comments

-

to get all of the account details removed from the Credit Reference Agency you are probably going to have to go to however they bought the debt from, tell them there was no consent to share (proving it with you letters) and ask them to remove the data as well. Westcost will only be able to remove anything they put on themselves.

James0 -

Westcost will only be able to remove anything they put on themselves.

Not always true as far as I know. It appears to depend upon whether the debt has been assigned, and if so who has inherited legal responsibility for the information recorded on the Credit Reference Files.

From: Information Commissioner: Technical Guidance Note - Filing defaults with credit reference agenciesThe ‘sale’ or assignment of debts on defaulted accounts

52 When the rights to a debt are sold to a third party, the lender has to make sure the records with the credit reference agency are accurate, up to date and adequate. If they want information about the debts to continue on the credit reference file they will need to come to an agreement with the purchaser about who is to be responsible for this.

53 If the purchaser agrees to take control of the record, the customer should be informed that the debt has been sold or assigned and to whom. The credit reference agency file should be changed to show the name of the purchaser and that the rights to the debt have been sold or assigned.

The purchaser should then make sure the record is kept up to date including changes to the amount still owed. The purchase should not affect how long the record is kept. It should be removed six years after the default.Free/impartial debt advice: National Debtline | StepChange Debt Charity | Find your local CAB

IVA & fee charging DMP companies: Profits from misery, motivated ONLY by greed0 -

thanks. nickx well i guess we will see what happens, but like i said fingers crossed and I'll let you all know what happens! thanks for everyones amazing help this forum and site is the most helpful ever!Nice Letter, quoting all the right legal facts.

I agree that I don't think they will refund anything, but no harm in requesting it. Afterall, always best to ask for more than you are actually happy to settle with.

It may well make them leave you alone though.0 -

right guys, not a sausage from wescot and the time limites have passed.

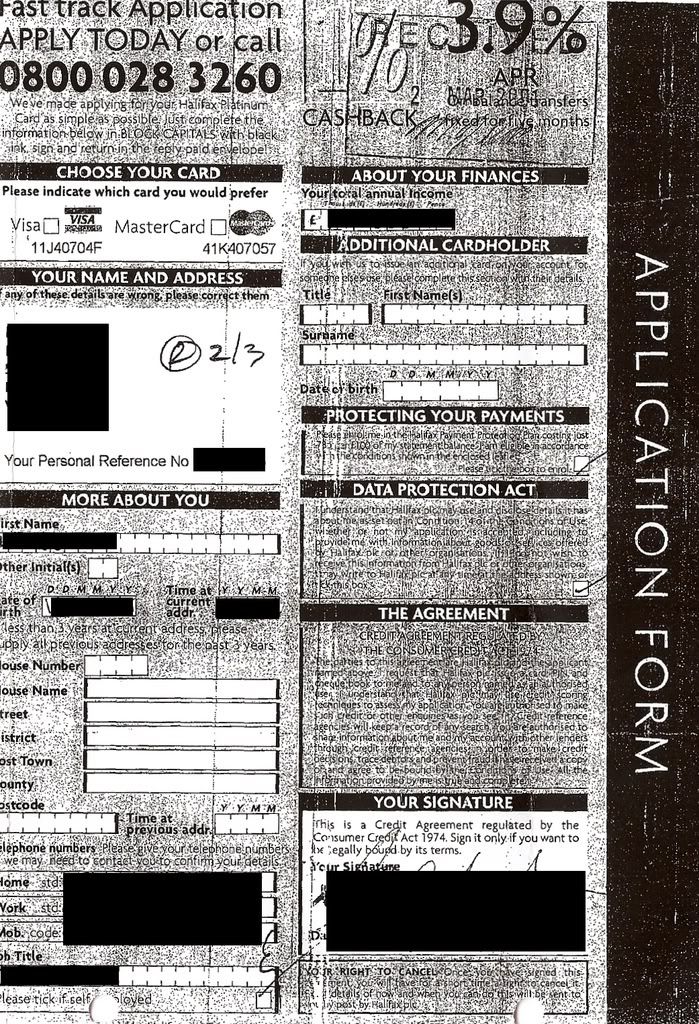

however 1st credit sent me a snotty letter and also enclosed an application form saying it was a CCA. Althought it is signed by me and it was recived by me after the 12+2+30 days can they enforce it (that is if it is a CCA)

I want to upload a picture i have scanned of it but i dont know how......0 -

i have uploaded to :

http://i278.photobucket.com/albums/kk84/momo19751975/1stcfedit.jpg

\right guys, not a sausage from wescot and the time limites have passed.

however 1st credit sent me a snotty letter and also enclosed an application form saying it was a CCA. Althought it is signed by me and it was recived by me after the 12+2+30 days can they enforce it (that is if it is a CCA)

I want to upload a picture i have scanned of it but i dont know how......0 -

any comments anyone?0

-

I agree with the comments on your CAG thread.

The copy agreement you have been sent doesn't comply with the requirements regarding "legibility" under the Consumer Credit (Cancellation Notices and Copies of Documents) Regulations 1983.2 Legibility of notices and copy documents and wording of prescribed Forms

(1) The lettering in every notice in a Form prescribed by these Regulations and in every copy of an executed agreement, security instrument or other document referred to in the Act and delivered or sent to a debtor, hirer or surety under any provision of the Act shall, apart from any signature, be easily legible and of a colour which is readily distinguishable from the [background medium upon which the information is displayed].

Even if it were "legible" it appears that it is missing the prescribed terms required by the Consumer Credit (Agreements) Regulations 1983, which means that in theory the agreement would unenforceable even by the court under s127(3) of the Consumer Credit Act 1974.

The letter suggested by pt2537 looks like your best bet.") Free/impartial debt advice: National Debtline | StepChange Debt Charity | Find your local CAB

Free/impartial debt advice: National Debtline | StepChange Debt Charity | Find your local CAB

IVA & fee charging DMP companies: Profits from misery, motivated ONLY by greed0 -

You most certainly know your stuff on this topic, I am very impressed.

James0 -

You most certainly know your stuff on this topic, I am very impressed.

Not really. I've just done a bit of reading around by looking at the stuff posted by the people who are really clued up on this.;)Free/impartial debt advice: National Debtline | StepChange Debt Charity | Find your local CAB

IVA & fee charging DMP companies: Profits from misery, motivated ONLY by greed0 -

Well well well....... 1st credit they are cheeky so and so's

After i had a letter form the kingdon guy at 1st credit, they must have not had my reply yet, or maybe they have cause this morning i received this letter:

"INSTALLMENT DEFAULT NOTICE"

" Our records indicate that you have broken the agreed installment arrangement. in these circumstances the full balance £XXXX.XX is now due and payable.

Please contact this office immediately to discuss voiding legal action

If you believe that you have maintained your installment arrangement please contact this office to provide full details of the payments you have made"

What next? do i remind them they have not sent em a valid CCA???0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards