We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Short term gilt yields

Comments

-

So, to be clear: you are agreeing with my proposition that the situation when short-term gilts are more favourable than STMMFs is not when base rates are expected to rise, but when the rise will be less or slower than gilt prices/YTMs are implying. And you argue that the latter does currently hold.

You may well be right. I think this is mainly relevant for cash-like allocations "trapped" in SIPPs or S&S ISAs, since one can already get about 4.3% on variable-rate savings accounts or cash ISAs, before any base rate rise.

The MPC is certainly aware that raising UK base rate can't counter an external inflationary shock, but that doesn't mean they won't raise base rate anyway, as they have done before. A spike in the price of an essential import makes the UK as a whole poorer, and the question is how that pain is to be distributed. The MPC does not want too tight a labour market in this situation, because they don't want workers to be in a position to demand sufficient wage increases to insulate themselves from the price shock. The MPC would call this avoiding second-order inflationary effects, I'd call it class warfare.* However, the price shock may cause an economic slowdown by itself, without any action from the MPC, so how much they will decide to raise base rate is difficult to say.

(*It's not political discussion if I just mention the existence of class warfare, and don't express support for any side, right? 😉)

0 -

"So, to be clear: you are agreeing with my proposition that the situation when short-term gilts are more favourable than STMMFs is not when base rates are expected to rise, but when the rise will be less or slower than gilt prices/YTMs are implying. And you argue that the latter does currently hold."

I agree with the principle that one should expect some risk premium for taking on duration risk, even at the shorter end of the curve. But my observation is that gilts are not always priced to deliver that. The risk premium for short duration is going to be small unless there is a more systemic asset class risk premium (some would use the word use the term "moron risk premium"). But future interest rate policy will also have a significant effect as nobody is going to lock into a 1 year gilt paying 4% if they believe money markets will be delivering a 4.5%+ return over the same period. So it is quite easy for such a small risk premium to be overwhelmed by other factors, which could result in a larger premium or a discount. Currently we appear to be in the larger premium phase, having recently transitioned from a discount period, albeit a brief one.

"The MPC is certainly aware that raising UK base rate can't counter an external inflationary shock, but that doesn't mean they won't raise base rate anyway, as they have done before. A spike in the price of an essential import makes the UK as a whole poorer, and the question is how that pain is to be distributed. The MPC does not want too tight a labour market in this situation, because they don't want workers to be in a position to demand sufficient wage increases to insulate themselves from the price shock. The MPC would call this avoiding second-order inflationary effects, I'd call it class warfare.* However, the price shock may cause an economic slowdown by itself, without any action from the MPC, so how much they will decide to raise base rate is difficult to say."

To be clear, I expect there to be some action from the MPC too, just not the short term +1% priced in to markets recently (and almost that much currently). At a guess, I'd think one 0.25% rise is very likely in one of the next two meetings, and then perhaps one more rise before the end of the year - maybe in autumn. But that does rather depend on how things play out with the orange toddler and his latest pet war.

1 -

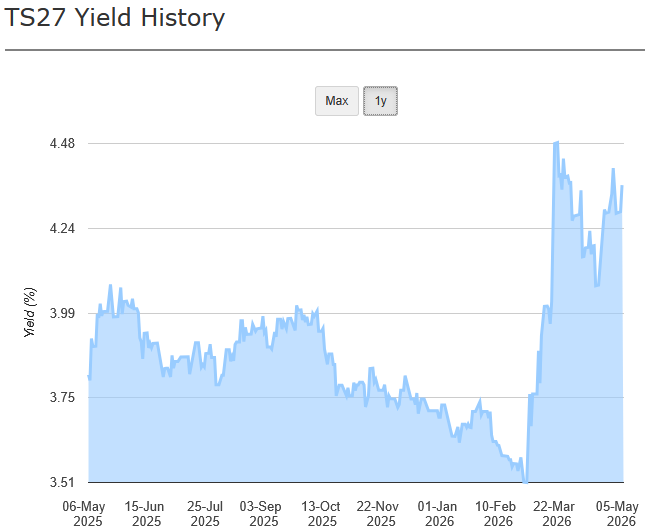

I agree that in theory the gilt yield at the short end should reflect the weighted average of the base rate until maturity (with a small risk premium) but an increase of nearly 1% compared to SONIA would, in a rational market, suggest a more immediate and steep rise in the base rate than seems likely. If the markets expect say three 0.25% base rate increases in M3, M6 and M9 from a 3.75% starting point, the effect on a one year gilt should be an increased yield of 0.375% (average of 3.75%, 4%, 4.25% and 4.5% = 4.125%, less 3.75%). But we saw a greater shift: the yield on TS27, maturing 7 March 2027, rose from 3.51% to 4.48% before falling back a little. That is the overreaction/irrationality mentioned by masonic.

Also, and on my point of gilt yields pricing in base rate expectations while STMMFs have to wait until they occur, then even if the gilt price adjusted more rationally, I could potentially exploit that by switching from STMMF into a short term gilt until one of two of the base rate increases materialised and then, for the latter part of the year, reverting to the STMMF.

0

0 -

I agree with the principle that one should expect some risk premium for taking on duration risk, even at the shorter end of the curve. But my observation is that gilts are not always priced to deliver that. The risk premium for short duration is going to be small unless there is a more systemic asset class risk premium (some would use the word use the term "moron risk premium"). But future interest rate policy will also have a significant effect as nobody is going to lock into a 1 year gilt paying 4% if they believe money markets will be delivering a 4.5%+ return over the same period. So it is quite easy for such a small risk premium to be overwhelmed by other factors, which could result in a larger premium or a discount. Currently we appear to be in the larger premium phase, having recently transitioned from a discount period, albeit a brief one.

Yes, to be clear: if base rate is currently 3.75%, and the expected average base rate over the next 12 months is 4.25%, then one would be looking for a 1-year gilt to pay a small premium over 4.25%, not a small premium over 3.75%. If it's priced "rationally", which it may not be.

Also, and on my point of gilt yields pricing in base rate expectations while STMMFs have to wait until they occur, then even if the gilt price adjusted more rationally, I could potentially exploit that by switching from STMMF into a short term gilt until one of two of the base rate increases materialised and then, for the latter part of the year, reverting to the STMMF.

Well, if the price remains "rational" at the time you're about to make the switch back from gilt to STMMF, the gilt would by then have a slightly lower price / higher YTM, which would prevent you from profiting by switching back. Of course, that may or may not happen, and you can continue to look out for opportunities to switch based on future mis-pricing.

(I wouldn't be trying this myself, since my cash is not "trapped" inside investment accounts, and is earning interest at very similar rates to the current YTM of TS27, and will almost certainly earn more if and when base rate rises.)

0 -

If my interest earned is below the tax allowance and savings rates are better than bond/gilt rates (I am not sure whether I have understood it correctly), apart from being able to access my money, would there be any other reasons to choose bonds/gilts as the return seem to lower than savings ?

0 -

Low coupon gilts with most of the return in the form of CGT free capital gain are most attractive to people who would otherwise be paying HRT (or ART) on their savings income. If you pay 0% tax on your savings income then gilts are less attractive. I suppose if you are skirting the threshold where you start to pay 20% tax you might like a low coupon to keep you under the threshold when a 4 or 5% interest rate might push you over but that seems a bit marginal. ISAs would make more sense but maybe you are maxing out the ISA subscriptions.

1 -

"Yes, to be clear: if base rate is currently 3.75%, and the expected average base rate over the next 12 months is 4.25%, then one would be looking for a 1-year gilt to pay a small premium over 4.25%, not a small premium over 3.75%. If it's priced "rationally", which it may not be."

Indeed, and the most likely path to get there would be four 0.25% rises spread somewhat evenly over the 12 months, ending up at 4.75%. Or it could come from two 0.25% rises early on, such as the next two MPC meetings. But the latter would contradict the current narrative of the committee.

T27A gives a "prediction" of base rate averaging about 4.25% over 9 months, which would likely require the base rate to be 4.5% by late 2026.

When looking at these numbers in combination with the rest of the yield curve, and of ILG yields, it seems much more likely that a more general risk-based repricing of gilts has taken place.

1 -

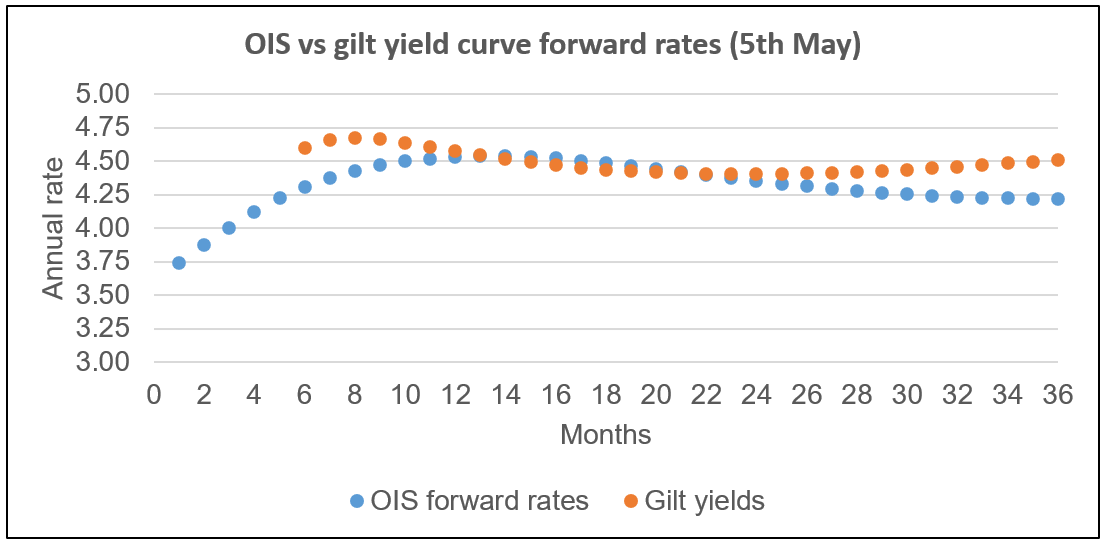

At the moment (5th May last datapoint) the OIS (overnight index swap) forward instantaneous rate at 6 months (i.e. at that point in time) is 4.31%pa and the forward 6 month gilt yield from the yield curve is 4.60%pa so there is a non trivial 0.29%pa differential between rates at the moment.

Not sure I can understand the technical reason for that size of difference.

At 12 months the forward instantaneous rate is 4.53% (OIS) vs 4.58% (gilts). So much closer.

The OIS forward figure at 1 month is 3.74% which is not surprising as the next monetary committee meeting isn't until 18th June (over a month away) so you'd expect it to be close to current base rate of 3.75%.

The OIS forward figure at 2 months is 3.87%pa which suggests to me a roughly 50/50 chance of a 0.25% base rate increase is priced in for 18th June (or more accurately it was at the end of 5th May).

I came, I saw, I melted6 -

Interesting that the short end of the OIS instantaneous curve is in an almost triangular formation at the moment and crosses 4% in 4 months, 4.25% in 6 months, and almost gets to 4.5% in 10 months, before falling back to between 4-4.25%.

2 -

This is the comparison of OIS vs gilt forward instantaneous (i.e point in time in both cases) rates (at 5th May)

I came, I saw, I melted2

I came, I saw, I melted2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards