We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Short term gilt yields

I’m trying to understand how the forward short term base rate is reflected in gilt yields. My starting point is > Latest yield curve data > OIS daily data current month > fwds, short end / fwd curve. It shows six months forward at 4.24%, 12 months forward 4.37%, 18 months forward 4.31%, and 24 months forward 4.20%. So, roughly, the base rate is expected to rise half a per cent in the next six months and then stay reasonably stable until this time 2028.

Gilt yields for those appropriate six month periods are (from )

- 3.83% for T26A maturing in October 2026

- 4.33% for both TS27 maturing March 2027 and TG27 maturing July 2027

- 4.33% for TG27 maturing July 2027 and 4.35% for TR27 maturing December 2027

- 4.43 for TE28 maturing March 2028 and 4.42 for TS28 maturing June 2028.

This seems to show that for short duration (excluding ultra-ish short T26A) gilt yields track base rate forecasts quite closely. Is that correct?

Comments

-

More or less, yes. The forward curve aims to isolate each slice of time, whereas the gilt YTM covers the entire period from today until maturity.

I don't know about your comment on the two short term rates generally tracking closely. Gilt yields can be persistently above or below SONIA forecasts, and the two forward curves would therefore diverge.

1 -

You would expect the overnight index swap rates and short term gilt rates to be consistent with what base rate currently is and is expected to be over a short time frame.

Remember the banks themselves bank with the Bank of England. So if you save with say Nat West they pool your savings with those of other savers and bank that saved money overnight with the Bank of England. The Bank of England then pays interest at base rate to Nat West on that overnight money (reserves). That's how monetary policy works to set interest rates.

If say treasury bonds (essentially short term gilts) were offering a lower rate than base rate was or was expected to be, then Nat West wouldn't buy them because they could just hold the money as reserves at the Bank of England instead and get paid bank base rate. And if the government offered a higher rate on an issue of treasury bonds than base rate was or was expected to be, then they would be sabotaging their own monetary policy, as Nat West would buy those treasury bonds rather than leave the money overnight with the Bank of England.

The knock on affect is that overnight index swaps also reflect short term base rate.

I came, I saw, I melted2 -

So if I hold SIPP funds in a STMMF that I will not need this financial year and I want to punt on the base rate being held or only rising 0.25%, I would buy TS27. I realise this also depends on the timing of base rate changes; the sooner it happens, the sooner the MMF equalises the difference.

Many thanks, SnowMan, for explaining how an announcement on interest rates is put into practice.

0 -

The broad idea that base rate and short term treasury bonds are going to be pretty consistently priced is fine, but you have the mechanics a bit wrong. Banks don't (and can't!) pool together deposits placed with them and deposit them with the Bank of England to create reserves. Banks can't create or destroy reserves at all; only the BoE can do that.

It is true in a sense that the BoE is the bank for the regular banks. For customers of regular banks, the deposits they hold with the banks are assets; for the banks, the same deposits are liabilities. Similarly, the reserves regular banks hold with the BoE are assets for them, and liabilities for the BoE. However, customers can take their deposits out of banks, or add to them. Banks can't take their reserves out of the BoE, or add to them; the only thing they can do with reserves is transfer them to other banks (a key way for banks to settle payments with one another), which does not change the total amount of reserves in existence.

The total amount of reserves can only change as a result of actions by the BoE (often working in tandem with the Treasury). The relevant actions are:

- public spending

- taxation

- issuing/selling gilts/treasuries

- redeeming/buying back gilts/treasuries

Actions (1) and (4) increase the total amount of reserves; actions (2) and (3) reduce it.

These 4 basic actions are the building blocks, but are often presented in a confusing way, when people talk about conventional and unconventional (QE and QT) monetary policy. It's confusing because some examples of the BoE buying gilts (action 4) are called QE, but others are not, but really there's no difference between them. And only some examples of the BoE selling gilts (action 3) are called QT. It's also confusing because the BoE have actually unnecessarily sold gilts which they're going to buy back again very soon under QE.

But if we ignore the way it's usually talked about , and concentrate on the 4 building blocks, it's relatively simple. If, as is normal, public spending is higher than taxation, i.e (1) > (2), then this can be funded either by expanding reserves, or by issuing more gilts than are redeemed, i.e. (3) > (4), or by a mixture of the two.

1 -

Some interesting commentary on the correlation between SONIA and short gilt yields here (timestamped): youtu.be/-hjHuksSkE0?t=1552

Illustrates the point I was making earlier about there sometimes being a disconnect.

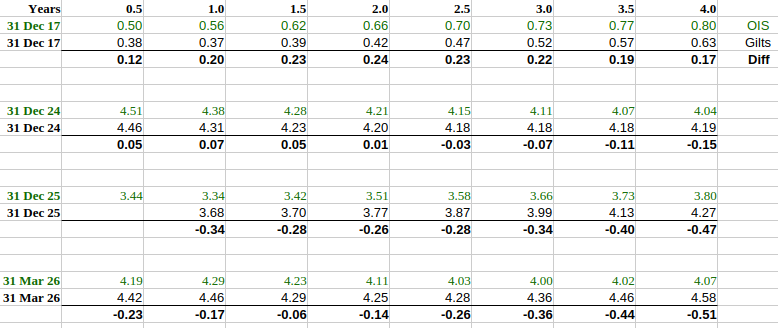

Looking over a few different historic dates also shows the variation:

0

0 -

I didn't word or explain what reserves are at all well, given that reserves in the first place come from government spending less taxation (with adjustment for gilts) that have worked their way into savings (net of loans). But I wasn't suggesting and didn't say that the banks in aggregate pooled savings to create reserves.

With quantitative easing the Bank of England did of course create reserves by creating electronic money to purchase those gilts, and so increasing private sector bank balances. Hence the connection between account balances and reserves.

If I switch my savings to bank A from bank B then bank A's balance at the Bank of England (reserves) goes up and bank B's balance at the Bank of England (reserves) goes down by the same amount. But from bank A's perspective it has higher reserves (an asset) at the Bank of England as a result of my transaction together with a matching liability to pay me back my deposit. Bank A gets paid bank base rate interest on that extra reserve amount. In turn the bank has to pay me interest at whatever rate the account pays.

My point was that as banks have reserves at the Bank of England (which in an oversimplified and clumsy one sentence description could be very loosely described as their combined customer savings net of loans) they have the choice as to whether to use some of those reserves to buy gilts or leave them as reserves and get paid bank base rate.

I came, I saw, I melted0 -

Thanks for the Pensioncraft video link, masonic . It is interesting that short duration gilt YTMs were, in mid-February, returning less than SONIA whereas now they are higher than SONIA – the shift is nearly 1%. That reflects an expectation that base rates will increase, aligning with the MPC’s “probably soon but not yet”. It is also why, in an environment where base rate increases are baked into gilt yields but not into STMMFs, short duration gilts are more attractive (the starting point for this thread; I made the switch into TS27 first thing yesterday morning), while, in an environment where there is an expectation of base rate cuts – baked into gilt yields but not into STMMFs – money market funds are more attractive.

0 -

A late reply, due to issues accessing the website …

Perhaps my last post was a bit of an over-reaction to your exact wording! You've added some helpful explanations here.

There is some kind of a market link between the base rate paid on reserves and the yields on short-term gilts, but I'd say it's a bit incomplete. The base rate is decided unilaterally by the BoE, so there is no market involved there. We are looking for market forces linking the relative, not the absolute, yields of base rate and short-term gilts. When the BoE issues new gilts, it needs to find a willing buyer; and when it chooses to buy gilts back before they mature, it needs to find a willing seller; so there are market links there. The market is expressing view about how the BoE will choose to set base rate in the future. However, when the BoE redeems gilts at maturity, the holder has no choice in the matter; and if the BoE chooses not to buy or sell any gilts, then there is no global choice of swapping reserves for gilts or vice versa (i.e. banks can swap with one another, but that requires 2 banks who wish to make opposite trades). So the market links feel a bit incomplete to me.

But that doesn't mean prices/yields are likely to be inconsistent! We are taught to look for markets in everything. But another way of looking at it is that the BoE is expressing its interest rate policy both when setting base rate (for overnight rates) and when buying or selling short-term gilts/treasuries (for slightly longer term rates). The BoE generally wants to tell a consistent story about interest rates, so it probably will do so, whether or not market forces constrain it to do so.

Comparing yields is always a valid starting point, but there may be other factors affecting banks' preferences for reserves vs gilts/treasuries. The latter, but not the former, can be used in repo operations, which is a possible reason banks might prefer to hold them. Possibly reserves are more convenient as a way to fund any outflows of deposits to other banks, which would go the other way. So operational factors such as these might have a marginal effect on yields.

That said, I would assume that, if banks would prefer more reserves or more gilts/treasuries, as the case may be, then while the BoE is not forced to accommodate such preferences, it probably would do so, since its role is to facilitate the smooth operation of the whole banking system. That is most likely the general motivation behind the policy decisions to implement QE and later QT.

0 -

I'm not sure I agree with that. If base rates will rise, then SONIA / the return on STMMFs / the return on plain cash deposits will also rise. The yield on short-term gilts may start out higher, but it's locked in (for the duration of the gilts), so it won't rise. Which could allow the floating-rate instruments to catch up. The gilts would do better if rates rise less / more slowly than expected. The floating-rate instruments would do better if rates rise more / faster than expected. You are of course free to express a view about how far / fast rates will rise! What is the middle case? In general, I'd expect a premium for locking into a fixed rate, though a small premium when it's a very short-term fix.

(And similar arguments apply when rates are expected to fall.)

0 -

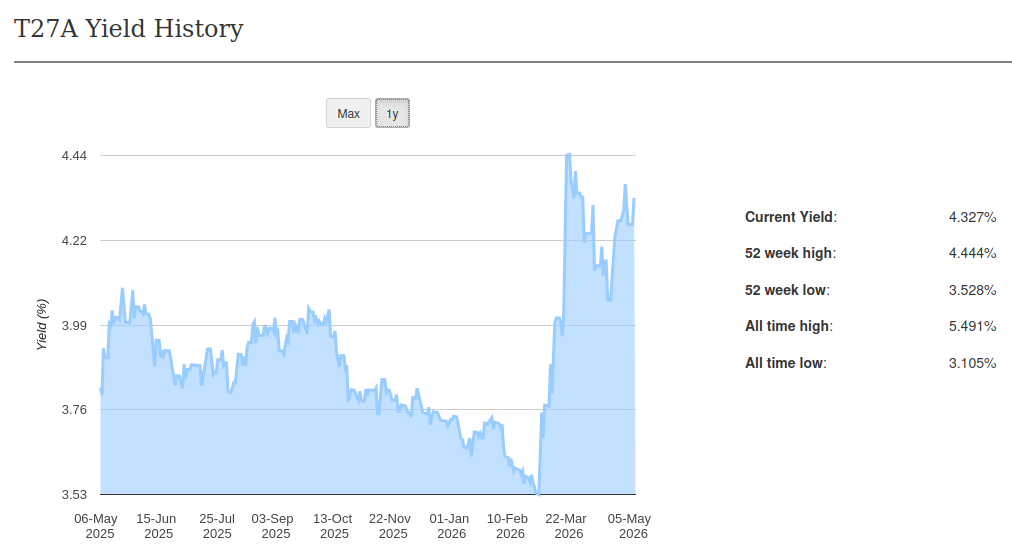

When the economic climate is fairly smooth, no doubt that is how things work. However, there are times when markets overreact, or are irrational. Not so long ago there was media speculation about the base rate rising 1% over the course of this year, apparently fuelled by movements in gilt yields. If you look at the historic YTM chart for T27A you do see this:

Before March, this was tracking the expected interest rate policy pretty well. But the 4.44% spike lacked any credibility as a prediction for base rate, even at the time. The subsequent ~4.1% easing started to look more reasonable, but now we're back up above 4.3%. We'll only know with the benefit of hindsight, but I think looking back this will be an overreaction. The MPC likely realises the futility of raising rates to combat an external supply-side inflationary shock, especially one involving an essential resource. Under those circumstances, such fall in gilt prices can be explained as an additional risk premium.

On the topic of markets being irrational, this was seen during the zero interest rate era, when gilt yields were fairly decoupled from base rate for extended periods.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards