We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Housing benefit nominal income from deferred pension

I reached pension age earlier this year.

I have some small private pension funds which I haven’t as yet decided what to do with - so I’ve deferred them.

As a recipient of housing benefit I have told my local authority (Hackney) about these deferred funds (around £15,000 in total value).

My understanding is that they should calculate the nominal income from these funds as the amount I would receive if I converted them into an annuity.

Instead of doing this they have said that my nominal income is the whole value of the funds (£15000) drawn down over one year - ie my nominal income is £15,000 a year & reduced my housing benefit accordingly.

Needless to say I have repeatedly objected citing DWP advice plus examples from common practice.

They have nonetheless stuck with their guns & insisted that their approach is in line with the 2006 housing benefit act.

I’m sure that they’re argument is absurd but I’m having difficulty finding anyone authoritative to support me.

Any ideas?

Am I just wrong ?

Obviously, I’m pushing to take this to a tribunal- but I can’t understand why they don’t accept that their approach is obviously illogical - in fact is it even legal?

Comments

-

You will need to check the regulations cited to determine how the pension should be treated:

I'm not familiar with the above regulations, but maybe this falls under 86(7)?

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.Our green credentials: 12kW Samsung ASHP for heating, 7.2kWp Solar (South facing), Tesla Powerwall 3 (13.5kWh), Net exporter1 -

DWP advice and guidance doesn't apply to housing and council tax benefits that are not administered by the dwp

2026 wins - Parker Pen, American Sweets bundle, dish magic bundle

0 -

I haven't read though the Regs for those over pension age they are below.

The Housing Benefit (Persons who have attained the qualifying age for state pension credit) Regulations 2006

https://www.legislation.gov.uk/uksi/2006/214/contentsEDIT did a bit of reading

4) This paragraph applies where a person [F8who has attained the qualifying age for state pension credit]—

(a)is entitled to money purchase benefits under an occupational pension scheme or a personal pension scheme;

(b)fails to purchase an annuity with the funds available in that scheme; and

(c)either—

(i)defers in whole or in part the payment of any income which would have been payable to him by his pension fund holder, or

(ii)fails to take any necessary action to secure that the whole of any income which would be payable to him by his pension fund holder upon his applying for it, is so paid, or

(iii)income withdrawal is not available to him under that scheme.

(4A) Where paragraph (4) applies, the amount of any income foregone shall be treated as possessed by that person, but only from the date on which it could be expected to be acquired were an application for it to be made.]

(5) The amount of any income foregone in a case [F9where paragraph (4)(c)(i) or (ii)] applies shall be the [F10rate of the annuity which may have been purchased with the fund] and shall be determined by the relevant authority which shall take account of information provided by the pension fund holder in accordance with regulation 67(6) (evidence and information).

(6) The amount of any income foregone in a case [F11where paragraph (4)(c)(iii)] applies shall be the income that the claimant could have received without purchasing an annuity had the funds held under the relevant scheme F12... been held under a personal pension scheme or occupational pension scheme where income withdrawal was available and shall be determined in the manner specified in paragraph (5).

Based on that I agree with the OP, it should be based on the amount an annuity would generate.

Let's Be Careful Out There1 -

Interesting question, but I think that the council may be correct here. Particularly with a pot as small as £15k. (Is that correct or did you mean £150k?)

Notional Income from a deferred private pension when over State Pension age is the income that private pension would provide if taken as income.

If there are options of how you could draw down the pot - as opposed to if the terms of the pension say that you have to convert to an annuity - then the councils approach may be reasonable.

To put it another way if the pensions terms would allow you draw it down over 12 months at £1,250 a month then I can't see any reason why the council can't treat the notional income as being that much each month.

It's going to depend on the actual terms of the pension and how those terms would let you take the money.

0 -

I don't think taking the whole value of a pension pot is logical. Before the pension freedoms were introduced in 2015 there was only one way to access the money in a defined contribution pension pot and that was to buy an annuity. Of course the pension freedoms legislation now give the pension holder many different ways to access that money but the priciple of a pension pot is still the same as before, to provide an income in retirement.

My reading of the legislation is the same as @HillStreetBlues in that the notional income used should be what annuity the pension pot could purchase.

As a side note I was surprised what annuity £15,000 could actually purchase.

Single life flat pension with no guarantees £96 p/m.

Single life, RPI increase with no guarantees £71 p/m.

1 -

@kaMelo do you mean shocked rather than surprised 😦?

0 -

Lol, no. They were much better than I expected.

1 -

Thinking more about the answer I gave above.

Whilst it could be reasonable for the council to treat the whole £15k as being taken in 1 year - provided that the pension terms allow it to be drawn down like that - then what happens after that year is up and the pension is still deferred?

Would the council then say "You still have £15k deferred pension which you could draw over the next 12 months, so we are going to treat it the same again for the next 12 months."?

Obviously that would seem to be unreasonable in most peoples view.

However the legislation may well allow the council to do so. Legislation does not always seem reasonable, particularly some of the benefits legislations.In the end though as the council are being adamant that they are correct in this case then the only way that the OP will get any movement towards confirmation or rebuttal of the councils stance is to go to the tribunal for a legal decision.

We can give opinions, but that is all they are.

The council will only budge if a tribunal tells them that they are incorrect in their interpretation of the law.PS. A bit of an aside but with small pension pots legislation can even override a pension schemes rules.

For instance there is the "Small pot lump sum" - If you have a pension pot worth £10,000 or less, you can cash it in fully. You can take up to three such payments from personal pensions.

There is also the related "Trivial commutation lump sum" - If you have multiple small pots and the value of all of your pension posts is less than £30k you can often take it all at once.

(Of course with either of those you are taking a lump sum and not an ongoing income, so the lump sum would/should be treated as capatial for HB and not as income).1 -

As a side note I was surprised what annuity £15,000 could actually purchase.

Single life flat pension with no guarantees £96 p/m.

Single life, RPI increase with no guarantees £71 p/m.

Those are suprisingly high to me too. (See the edit below).

£15000 / 96 = 156.25 months or just a week over 13 years.

So if you take that at age 66 and live to above 79 technically you'll be winning.Don't forget that those figures are before tax, so the taxman will be taking a chunk of that £96, probably just below the full 25%.

If you have a full State pension it now takes up all but £34 of the single persons annual tax allowance, giving you a tax code of just '3L', (I got my code notification last week).£96 x 0.75 = £72.

£15000 / 72 = 208.33 months or just over 17 years and 4 months, and so it will take you roughly until over 83 before you have received £15,000 worth of (after tax) payments from the annuity.Of course the annuity providers are gambling that you snuff it early.

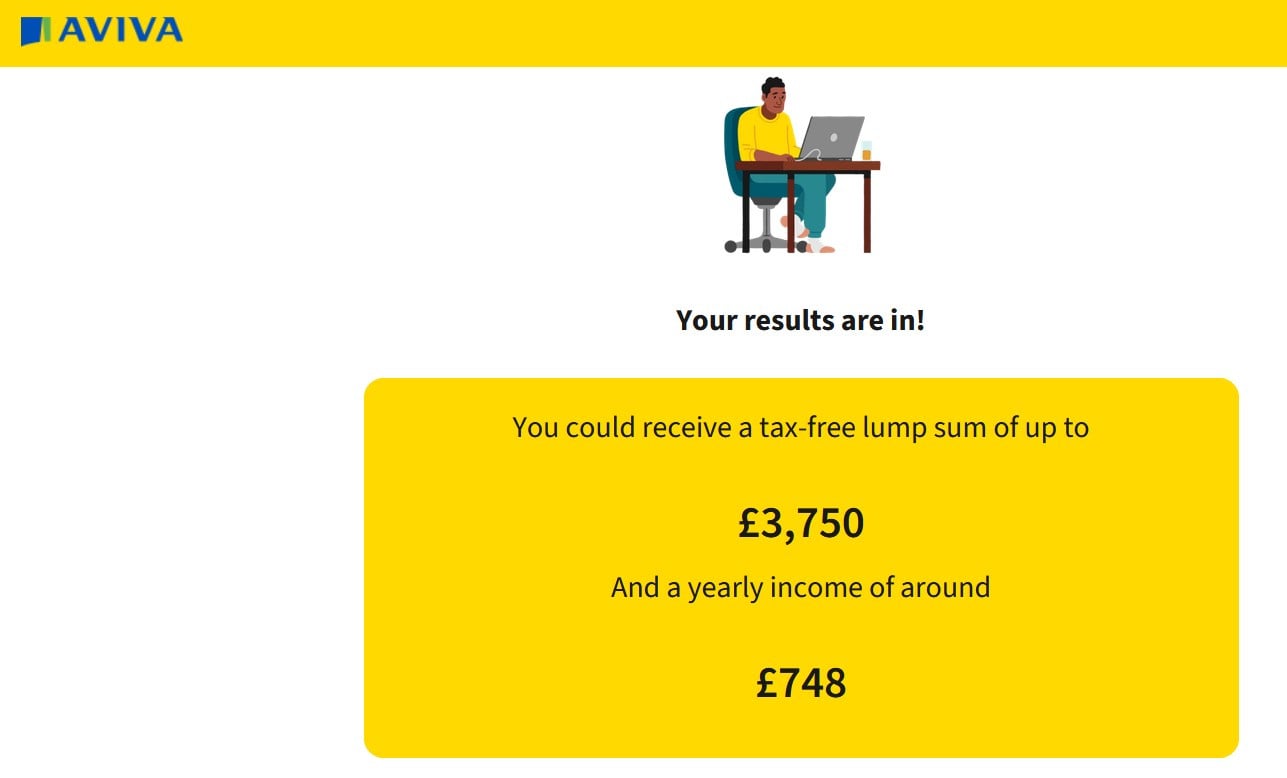

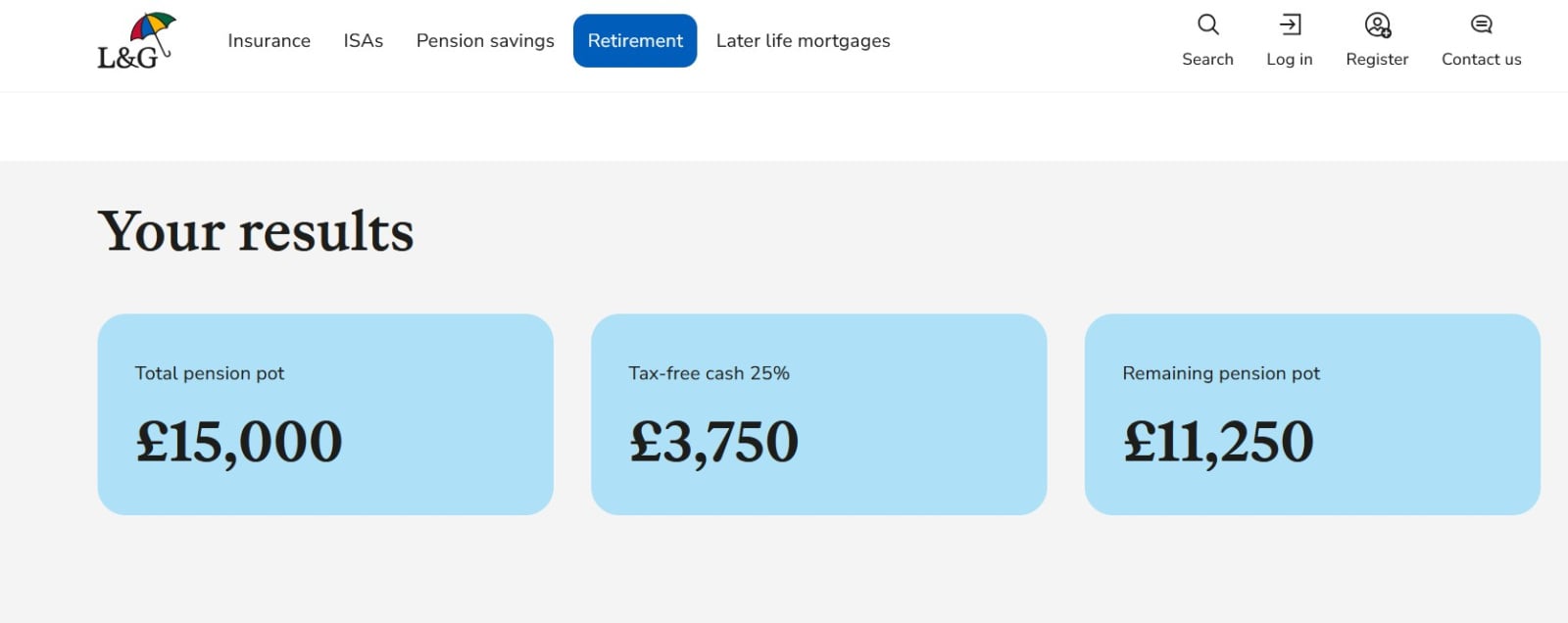

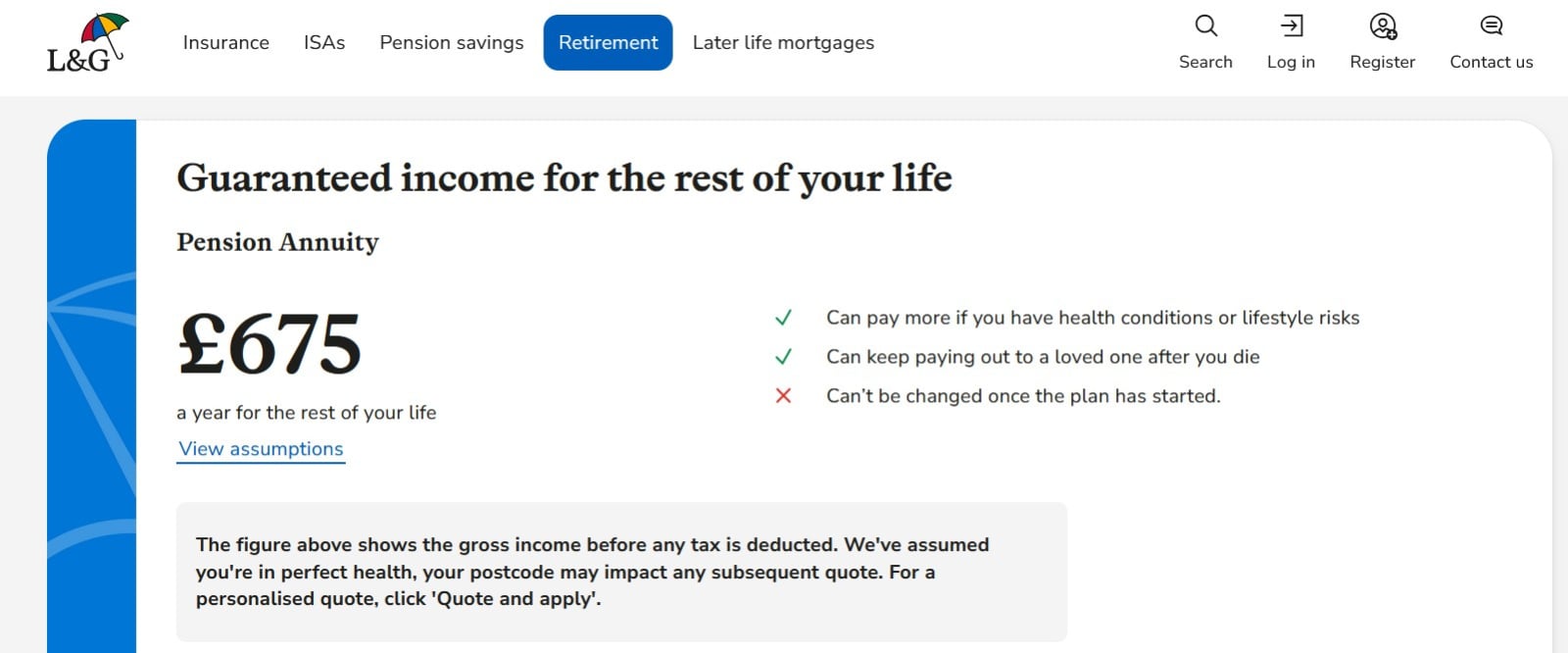

EDIT- As a sanity check (and because I don't fully trust AI answers on Google) I put £15k into the Aviva and Legal and General Annuity calculators, the results are below. And show that you need to shop around.

Although it would be nice to see what the quotes would be without the 25% lump sum the calculators don't give that option. (you can roughly extrapolate though by dividing the given income by 3 then multiplying by 4).

Taking the highest qoted income of the two, Aviva:

£748 a year is £62 a month (before tax).£15000 - £3750 = £11250

£11250 / 748 = 15 years and 2 weeks.

0

0 -

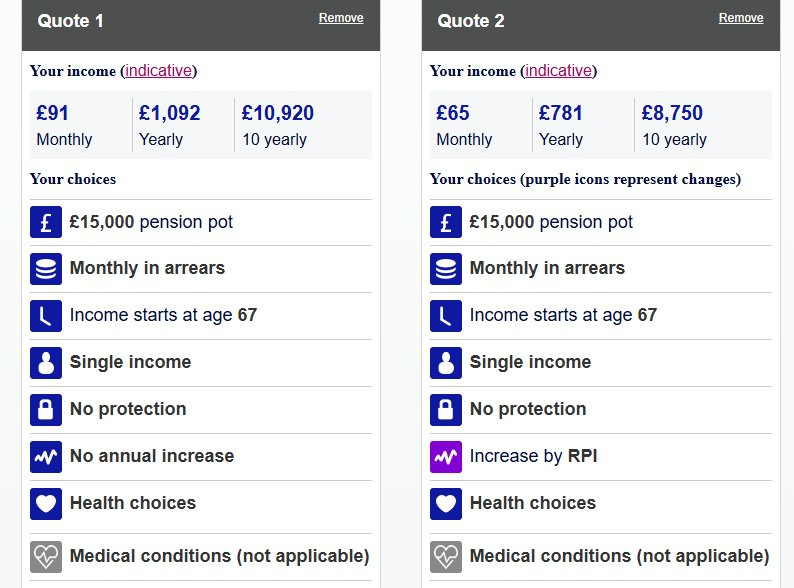

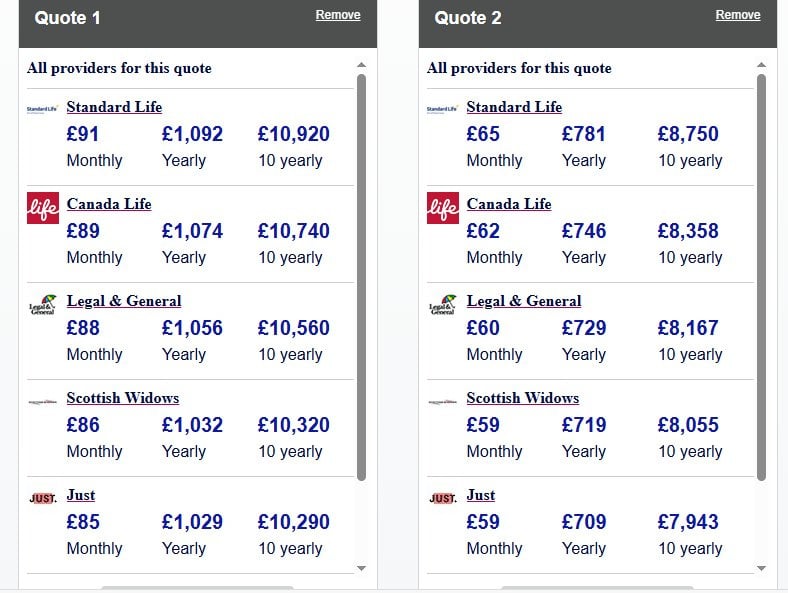

I used the annuity comparison tool on MoneyHelper, these are today's quotes (which are worse than yesterdays) which shown it definitely pays to shop around.

I used basic factors but changing one of those factors above could increase/decrease the monthly payments depending upon your choices, it really is an individual quote. Both quotes above were supplied by Standard Life.

Annuities are no different to any collective insurance scheme or Government tax and spend regime in that some of those who pay in will 'lose' and some will 'win'. Those who die early without a guarantee period will lose, those who become octogenarians and above will undoubtedly win.

Regarding the 25% tax free amount, it is not included in the annuity quote. If someone chose not to take the tax free lump sum and purchased an annuity with their entire pension pot they don't get any credits for that in the monthly payments. Anyone taking a TFLS need to deduct that from their pot before getting an annuity quote.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards