We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Cash ISA tactics for the new tax year ?

Comments

-

What's the point? Surely you'd want to do both on 6/4 so that none of your allowance is lost?

Remember the saying: if it looks too good to be true it almost certainly is.0 -

It's future transfers (beyond the initial funding window) that are allowed at their discretion, meaning you need to contact them to ask. The exact wording on the T&Cs is "Transfer requests received after your initial account application may be refused".

New subscriptions from subsequent tax years are allowed so base rate changes don't matter and you don't need to ask permission to do that - the wording from the T&Cs is "Please note that the Bank reserves the right to withdraw this product at any time. If the product is withdrawn, you can continue to put more money into your account until the expiry of the fixed term."

I opened a Shawbrook fixed ISA in January 2025 (funded with a transfer) and then paid more into it via bank transfer (faster payments) in November 2025.

1 -

Confirm the above. Transfers after the initial funding window are at their discretion, and you can be pretty sure that if rates are falling they will not accept later transfers.

However no problem to top up with new money at any time during the fixed term. It is an attractive option to take advantage of if rates are falling. I presume they allow it as they know the maximum you can add is £20K per tax year. For their non ISA fixed rate products, you can also add new money after the initial funding window, but if the product is withdrawn then you only have 28 days to add more and then that is it.

On the other hand Shawbrook have the restriction that you can only add new money to one of their ISAs each year, which is not typical for most providers.

0 -

Chip is flexible, but it would count as new money being deposited into a new Cash ISA.

0 -

I'm not able to follow this discussion back to its origin, but if the Chip ISA is flexible and contains £20k of current year subscriptions, then withdrawing £20k tomorrow and depositing that £20k into Prosper tomorrow would be valid and leave the 2026/27 allowance intact. Which I think was @nottsphil 's point. Otherwise, as he said, withdrawing £20k on the 6th and depositing it on the 6th would achieve exactly the same as 5th → 6th.

1 -

Exactly so, and means you would be needlessly using up your entire allowance for 2026-7.

0 -

As I have been led to believe, only the current year's subscriptions can be withdrawn and placed into a different provider's ISA without losing the allowance. If somebody can confirm this, then it means your advice would result in the loss of a year's allowance.

0 -

That's correct, current year subscriptions can be withdrawn from any flexible ISA and replaced into any other ISA without using additional current year subscriptions. Prior year subscriptions must be replaced in the same ISA or will count as new subscriptions if paid into a different ISA.

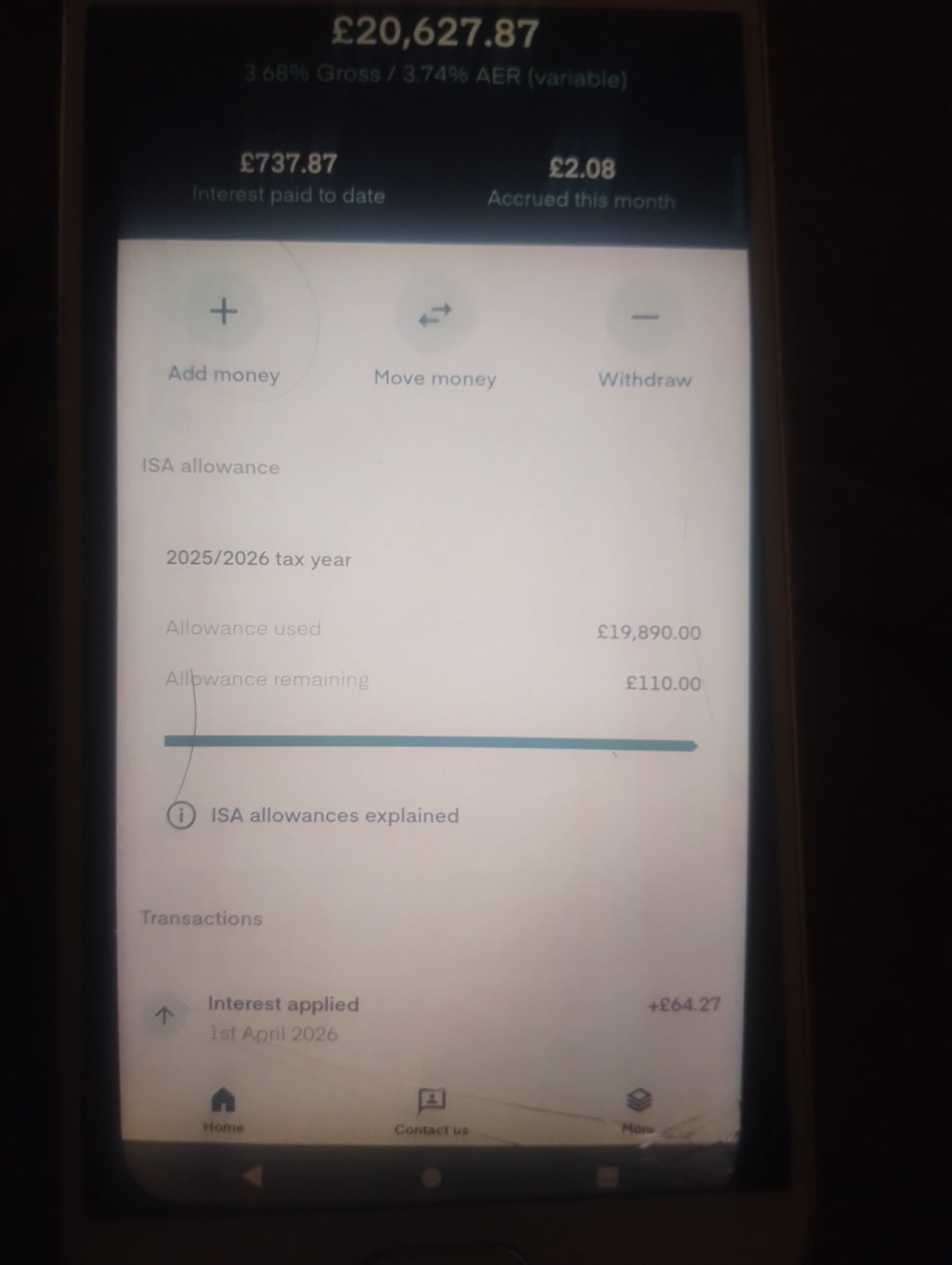

3 -

Maybe a working example would make things crystal clear (unlike this photo of a photo; Monument pointlessly bans screenhots).This is the cash ISA I opened early this tax year and I've made no withdrawals, so my total subscriptions are £19890. I will withdraw this sum into the linked account, then from there into any cash ISA in my name, new or old, flexible or rigid and it'll still retain its tax-free status - but only if I do so this tax year. The £737.87* interest accumulated can also be withdrawn now and used as I like, but its status can only be restored by returning it to this account (though at any time). However I can do this multiple times, so intend using it as a high interest instant access account because it equates to 4⅔% gross as I pay 20% tax on interest (unlike some, I don't have 7+ Cahoot SDSs 🥲).

*less the minimum balance, which I didn't made a note of because I never envisaged the account being this versatile.

0 -

But it would be sitting in an account with a much better interest rate?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards