We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

flexible cash ISA: does withdrawn money count towards allowance?

Comments

-

This news has been a revelation for me. I have almost £20,000 of this year's new money languishing in Monument at 3.74% AER but didn't move it to a preferred one because it didn't accept transfers in!

I think I will go with Plum to get the 4.66% then transfer out in a year's time, as long as it's not one of those platforms where your money is held somewhere for a period (however brief) that is a grey area for FSCS protection.

0 -

Plum uses Modulr FS to collect the money going into your ISA. Modulr is an e-money institution, so you don't get FSCS protection while they hold it, just the e-money "Safeguarding". I used Plum last year, took the risk, and the money landed within seconds into my ISA.

1 -

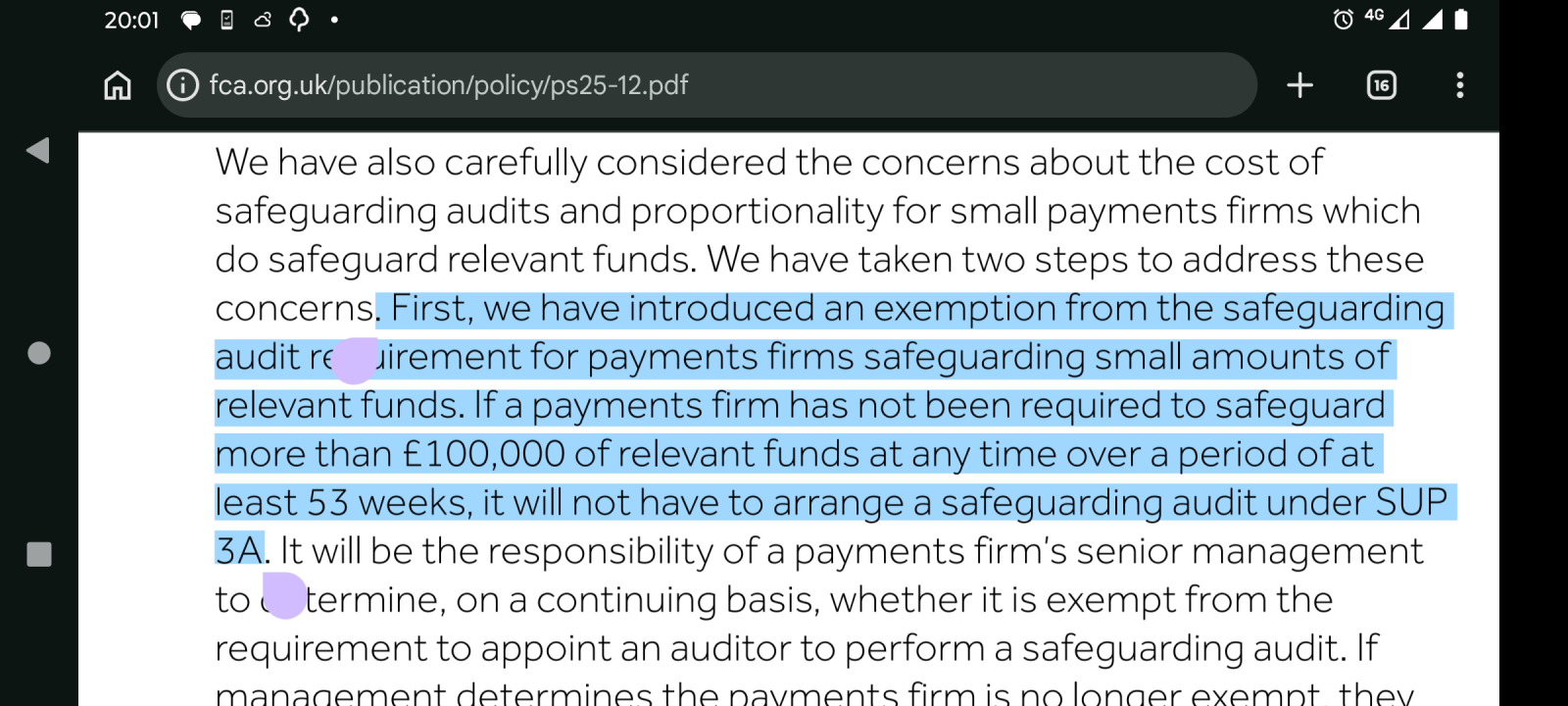

I've looked into this via and when I read the highlighted bit below, I thought it couldn't apply to Modulr FS as they must be processing millions of pounds per week, if not per day. Then I pondered your report of money moving within seconds and am now wondering if their systems don't actually allow a six-figure sum to accumulate, because maybe input is restricted until the near-instant output has occurred. This would fulfill the requirement that less than £100,000 is held at any one time, so could this be a ploy to put keep them in a more lenient regime?

0

0 -

Probably not a deliberate ploy. They are a payment processor, so they should not be holding on to money for any longer than absolutely necessary. That said, it seems likely that at times they'd be processing very large transactions that would prevent them from claiming the audit exemption.

I'd feel safer if they didn't keep hold of my money for a second longer than necessary vs having it linger in their holding account and them being subject to an annual audit.

1 -

Wait - why does earning interest mean this no longer works? I had 16k in T212 flexible ISA - all this year's contribution. I withdrew it today and left the interest in the account. It now shows as zero ISA allowance used for this year. Then I deposited the 16k funds into a flexible Prosper's ISA. Is there something I need to be aware of re the interest remaining in the T212 ISA?

0 -

No, leaving the interest behind is a necessary condition of self-transfer from a fully subscribed flexible ISA. Said interest can be left there or transferred to some other ISA using the formal process. It does not count as current year subscriptions.

2 -

What you did is fine because you left the interest in the old ISA. My point is that you can't manually withdraw the interest and put it in a new ISA without it counting towards your ISA allowance. You need to do formal ISA transfer to move it.

#24 Save 12k in 20261

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards