We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Shawbrook 7 years fixed rate, would you go for that?

Shawbrook bank website is offering a quite rare (or let's say unusual) 7 years fixed rate Bond at 4.21% interest (and an Isa version at 4.14% with deposit allowed in the first 90 days that it is useful even for those who have already maxed out this year allowance and they must wait for April). Would you put £1000 on that ? Do you value certainty or, given the very long period, would you put the same money on a stock and share fund ?

Comments

-

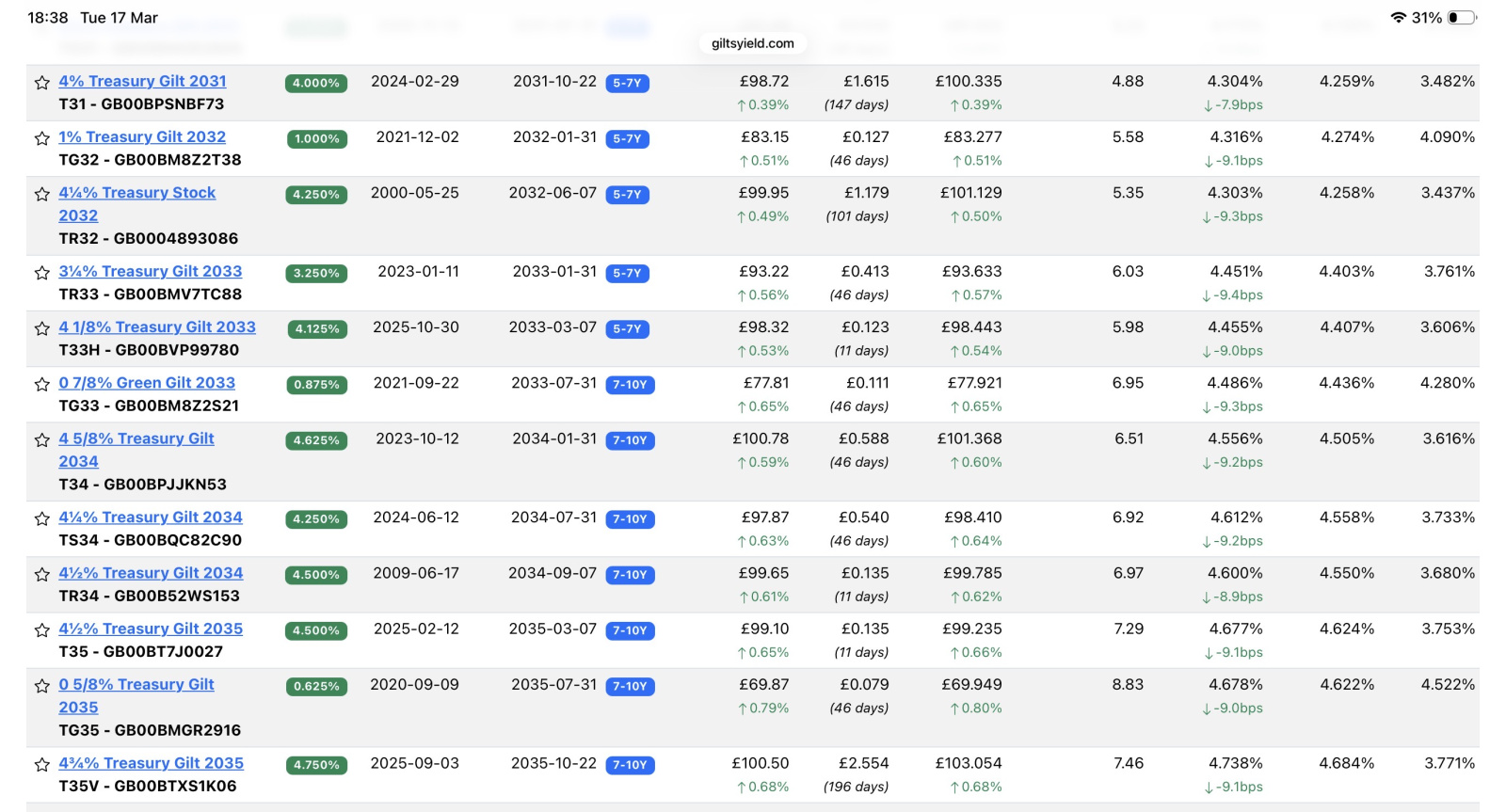

No. Could get a gilt at 4.486% which is low coupon therefore largely tax free for the same duration.

4 -

For an inaccessible 7 year savings bond I'd want at least 5%. If you want a known return for seven years I'd buy a 2033 gilt rather than this: 4.45% and you can sell it anytime. TG33's a low coupon gilt so most of the return would be tax free when it matures but not much good for ongoing income.

6

6 -

Can't see the column headings but I think you're saying it costs £77 but you'd get £100 in 2033.

This gain would be tax free?

And the c1% annual coupon would count as income?

Thanks

0 -

The ISA would be more attractive because apart from the tax issue, Shawbrook allow new contributions throughout the fixed term ( unusually). So if in some years time interest rates had dropped a lot, that would be a nice advantage. So probably at least worth a punt to put a £1000 in just to get it open.

Always good though to check the T's & C's to make sure this still applies.

0 -

Yes, if you spend £7781, you will get £10000 tax free in 2033.

7/8% so about £68 yearly is treated as income and taxable if you're over limits.

In theory you can sell it but.. if interest rates go up to 10% it will lose a lot in value so may need to keep till maturity date. And vice versa, it may go up in price if they drop to 1% :D

0 -

In this case appears that the limit to deposit money is the first 90 days, while the last 5 years Bond allowed deposit throughout the entire term.

0 -

Demonstrating that it's a gamble on inflation as much as interest rates.

There is a point where the gamble is worthwhile, but for me it would need to be much higher than circa 4%!

It's actually the gamble in the opposite direction I would be more inclined to take currently, fixing a mortgage for that long. In fact I did just that in 2021 for this length of time, at around 2%.

0 -

Looks like T&Cs might have changed a bit. Sounds to me like you can only fund it in the first 90 days. And they also allow you to open multiple ISAs with them in a tax year, whereas previously you couldn't.

1 -

Website link below. Capital gains on gilts and other “qualifying” sterling bonds are tax free but on the flip side losses aren’t allowable against taxable capital gains.

https://giltsyield.com/bond/

0 -

But no more a gamble on inflation than a 7 yr fixed savings account (less, actually, because the return is higher).

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards