We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Natural yield vs. total return

Comments

-

How do you decide when to invest some of your capital growth into more income generating funds?

0 -

I agree with this. If you want income and also capital growth, it is better to choose the best asset for income and the best asset for capital growth, rather than a single asset that serves both objectives sub-optimally. For example, I am overweight UK because a UK equity income index fund provides better income than a global equity index fund; if it didn't, I would not be overweight UK.

0 -

I agree that a good strategy depends on having clear objectives. IMO, within retirement, there are broadly two objectives: the first is to provide 'sufficient' income and the second is to (potentially) provide a legacy. These are competing objectives - increasing the amount of income will decrease the amount of legacy and vice versa.

FWIW, my philosophy has been to

- Build an RPI protected floor of income that meets all core and most adaptive spending. In my case largely using a DB pension and, eventually, the SP, but other sources are available (e.g., RPI annuity, collapsing ILG, or single ILG)

- Take variable withdrawals from the remaining total return portfolio using an amortization based approach (effectively giving a gently rising percentage of portfolio).

I note that the three methods I mentioned of building inflation protected guaranteed income flooring illustrate the competition between income and legacy.

- RPI Annuity. Currently a single life RPI annuity (5 year guarantee) taken at 65yo provides a payout rate of 5.4%, but of course provides no legacy (buying a joint annuity or lengthening the guarantee period, the latter providing a legacy, reduces the payout rate).

- Collapsing ILG ladder. A 35 year (taking a 65yo to 100yo) ILG ladder currently has a payout rate of 3.7%. The amount of legacy will depend on the time of death, higher for earlier death, and changes in yields (higher yields, lower legacy and vice versa).

- Single ILG gilt. It is currently quite difficult to find an ILG with a reasonable coupon and maturity. TR49 would give an inflation protected payout rate of about 1.9% (i.e., pretty terrible) but would deliver a legacy (in 2049) of about 102% in real terms (which could be used to purchase another gilt).

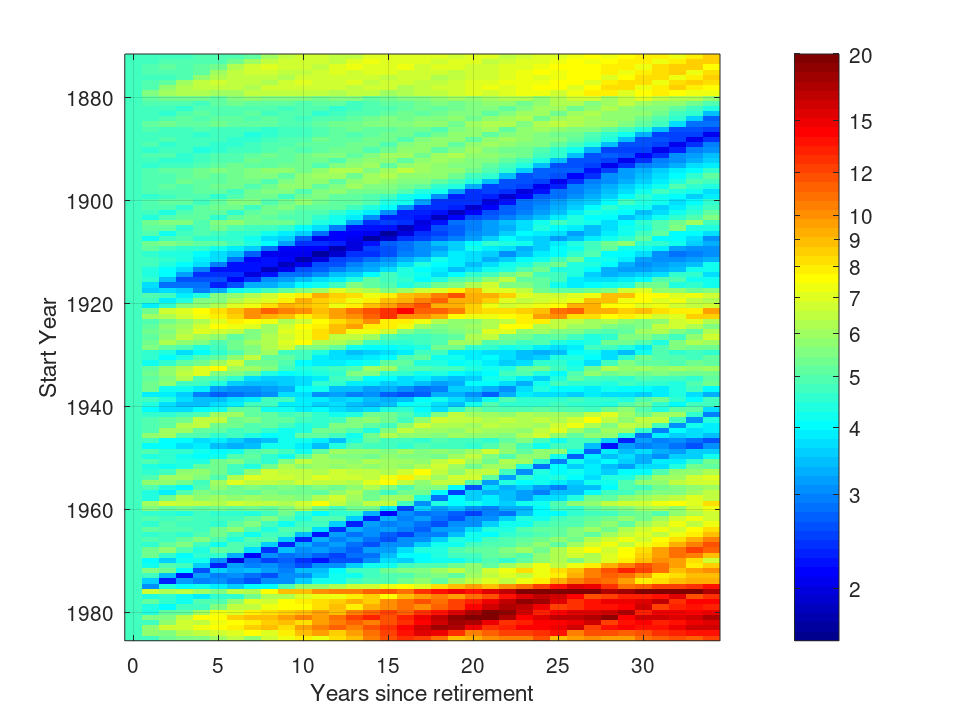

Finally, with a solid income floor, despite what you keep saying, taking percentage of portfolio withdrawals will not be particularly stressful since I know that my plan can cope with likely fluctuations in income. For example, the graph below shows the historical real withdrawal rate (in colour) as a function of start year and time after retirement.

Yes, there were some pretty awful periods in the past (coloured blue in the plot), e.g., a decade up to the end of WWI of income around the 2% mark and a second decade starting from 1975 or so. The retirement starting in 1937 was lousy too. However, retirements starting since just before 1980 have been very good although note that the dataset I'm using currently stops at the end of 2020. In other words, recent experience in the UK has been unusual in an historical context.

To put some specific numbers to this, for a couple with two full SP and a £500k portfolio, the initial income would have been £24k from the portfolio and £24k from the SP, for a total of £48k. Fluctuations would have seen a worst case real portfolio income of about £8.5k for a total income of £32.5k.

For those following a natural yield approach, how would a retirement starting in the 1960s and early 1970s have done (AFAIK, there are some current ITs going back that far)? Can anyone provide actual numerical evidence (not generalities) for comparison? I have modelled natural yield using index data (see earlier post), but only for the UK (i.e., not an international portfolio) so a comparison with the above is unfair (natural yield was a lot worse, but only because it was a UK only portfolio).

* For the graph I've used a portfolio with 30/30/20/20 (US equities/UK equities/UK long bonds/UK bills) as a proxy for an international portfolio and return and cpi data from macrohistory.net. The initial withdrawal was 4.8% of the portfolio.

0 -

My aim is to keep my total ongoing income higher than my normal expenditure, with the excess topping up a cash pot which is mainly used for larger one-off expenses. When I rebalance or reorganise the growth portfolio I would normally leave some money as cash or move it into income generation at the same time. In addition should the cash pot begin to steadily decline over say a year I would rebalance the portfolios to generate extra ongoing income, though this has never actually happened.

The objective is never being forced to sell long term investments for cash for short term reasons. The S&P 500 has crashed by about 50% twice in my investing lifetime. Taking drawdown rather than buying an annuity only became a practical choice for a reasonable number of people with DC pensions (including myself) in around 2012 and for everybody else in 2015. I fear that as experience of living through a real crash is very limited next time many people are going to be very frightened.

0 -

Some questions if I may:

- How many years would your gilt ladder cover without replenishment?

- How often do you buy new gilts?

- How do you manage large one-offs?

0 -

If you mean generally with this approach ('floor and upside' as it has been termed) then, I should first stress that (broadly) there are two components, the floor (guaranteed income probably from multiple sources) and upside (i.e., a risk portfolio).

For a lifetime floor, a collapsing gilt ladder can be constructed to cover a period to 100yo since it will then cover a lifetime in virtually all instances (notwithstanding that I have two acquaintances who are over 100). For short term bridges (say from retirement to SP age), then the period is well defined by the end date. While these ladders are often considered to be fully constructed 'at retirement', and therefore new gilts are not needed, gradual construction can be adopted in the run up to retirement (e.g., Zwecher's book, Retirement Portfolios: Theory, Construction, and Management) and the ladder can be added to in retirement. However, this adds some uncertainty since poor performance from the portfolio (e.g., historically the UK stock market has had negative real returns over a some 20 year periods) and falling yields would reduce the amount of income available.

Personally, we keep an amount in cash savings (which I consider separately from the risk portfolio) sufficient to cover multiple emergency spends (e.g., new boiler, house repairs - even a new roof, etc.), although there is a limit to what this covers. Even in retirement, I've not lost the savings habit, so the cash savings are topped up from income. In the event of an emergency that exceeded the amount in savings, then the portfolio would have to be used. Since that includes fixed income at various maturities (i.e., one year fixed cash and short and long bond funds) even in the event of an equity meltdown there will be some amount available. If the emergency exceeds the amount we have in the portfolio (e.g., house destroyed, but the insurance won't pay out), then we're in trouble (but I suspect that would be true for most people).

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards