We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Natural yield vs. total return

Comments

-

You seem to be talking about investing in individual shares rather than funds.

Dividend investing with a fund is very different to total return investing in that the dividends paid out by the fund bear no relationship to then current capital value of the fund and are simply the sum of what each individual underlying company has chosen to pay out expressed as £/share. For those companies with a policy of paying a high dividend there is a strong incentive not to cut the dividend as the shareholders dont like it.

The point about the capital value of a share dropping by the value of the dividend on the ex-dividend date can be argued for individual shares. However again for funds the situation is very different. Taking a fund's dividend means that you are only taking money from those underlying companies that are paying a dividend leaving all other holdings unaffected. With total return investing when you sell you are reducing your holdings in all the underlying companies.

Finally with income investing with funds you do not have a problem when an individual company's market value falls as long as it keeps paying its dividend, as is usually the case. A good income fund will invest in a wide range of companies so that even the complete failure of a single company has little effect on the overall income. Of course if all the underlying companies profits fall and they cut all their dividends then you have a problem. But such an event would be so severe that you will be having problems no matter how your equity is invested. However it would be much common for a total return investor to find that his fund has fallen in value because of some external event frightening the markets.

0 -

Companies do not like cutting dividends, but that is not necessarily good. If a company pays out more than it can reasonably afford, maintaining dividends is not good. It is not free money. Bumper dividends followed by a rights issue is certainly not good.

With a fund, just as for a portfolio of individual shares, any dividend that you are paid comes from the capital value of the underlying portfolio. A market weighted tracker holds the same percentage of the free float of all the shares in the index. Selling a percentage of the fund preserves that.

With total return investing, you also do not have a problem with individual companies cutting their dividends. Companies can pay dividends from cash deposits if they think that a downturn is temporary. (They have an incentive to do that when they should not. As you said, they do not like cutting dividends.) You could decide that a downturn is temporary and draw some money from your savings, but you might be better advised to cut your expenditure.

0 -

The other side of the coin is that the dividend payments may be much less than you could safely withdraw with a total return strategy. If you have money left over in a SIPP, you face punitive taxation if you want to pass that money on to the next generation. If you withdraw too much, you face poverty. You cannot avoid making difficult decisions about how much money to take out.

0 -

Comparing the different approaches can be tricky.

Currently, a collapsing inflation gilt ladder covering 35 years (suitable for retirement at 65yo?) has payout rate of 4.3%. This means, that (in the absence of UK debt default), the monthly real income will be reasonably certain over that period.

How long the income from a total return approach using constant inflation adjusted withdrawals (i.e., the so-called 'safe' withdrawal approach) will last is unknown. However, historically, for a UK retiree with a 30/30/20/20 (UK equities/US equities/Uk long bonds/UK cash) had SWRs over 35 years ranging from 3.3% (worst case) to 3.9% in 10% of retirements to 4.9% (median case).

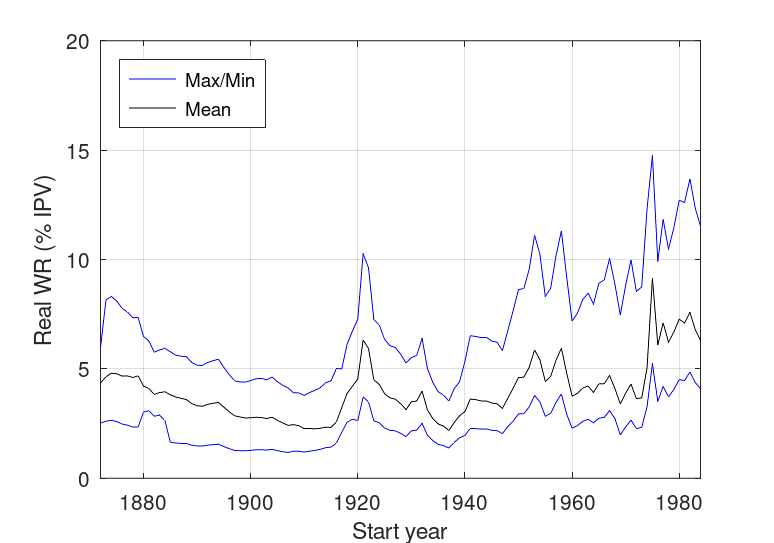

For a natural yield approach, historically the real income varied from year to year. For example, the following graph shows the minimum, mean, and maximum real income as a function of 35-year retirement start year for a 60/20/20 portfolio (UK equities/UK long bonds/UK cash*).

In other words, in common with any variable withdrawal strategy, retirees adopting a natural yield approach should expect variation in real income and have a decent floor of guaranteed income (e.g., from SP, DB pension, ILG ladder, and/or annuity) to reduce the fluctuations. It is noteworthy that the last 40-50 years have been fairly good for UK retirees.

Of course, this was natural yield from UK share index and government bonds. Whether income ITs did better or worse than this over the same period is unknown (AFAIK, the data are just not available).

* returns from macrohistory.net

2 -

With not too much effort or taking crazy risks one can get a steady income of around 6% of initial investment from income equity and well diversified Fixed Interest. That is well above the normally accepted Safe Withdrawal Rate.

For an IHT payer SIPP inheritance taxation is unlikely to be more onerous than if you withdraw the money before death.

For many people it makes sense to withdraw as much SIPP money as possible at Basic Rate and put it in an ISA.

2 -

6% does not come without risks, but may not be above the SWR when you are 80. Drawing an income from risk investments has risks however you do it. If you want a safe income, buy an index linked annuity. Nonetheless, nothing is completely safe.

0 -

"For an IHT payer SIPP inheritance taxation is unlikely to be more onerous than if you withdraw the money before death." You make assumptions about the age you die (over/under 75) and the marginal tax rate you and your beneficiaires pay, but that is another story. I'm just mentioning it here in case others take your comment at face value.

1 -

Is the 6% nominal or real or unknown?

'Safe' withdrawal rates assume inflation protected income (so an initial 3.5% will be adjusted for inflation throughout), but have an unknown lifetime. However, fair comparisons between different methods are often difficult.

To take a 'simple' fixed income natural yield example, in August 2002 you could have bought (price and coupon data from the British Government Securities database at )

- A newly issued index linked gilt with 2% coupon at a nominal price of 94.85

- Nominal gilt with 4.25% coupon at price of 92.26.

For the ILG, £100k would have bought an initial annual coupon income of £2109, which would now be paying out (in nominal terms), £3943.

The nominal gilt would have initially paid out £4606 in coupon income and will continue to do so until maturity (2032*).

From this it would appear that the nominal gilt was a far better bet, but the final capital values are very different. At par, the ILG is currently worth £194k (i.e., in current nominal pounds), while at par the nominal gilt is worth £108k. In other words, the ILG holder has given up income in exchange for final capital.

* I note that there is a further small difference which further muddies the comparison in that the ILG matures in 2035 and the nominal gilt in 2032.

1 -

The 6% is nominal though in practice one would expect equity dividends to broadly increase with inflation, all orther things being equal. Corporate bonds wont increase with inflation though some infrastructure fixed interest is likely to do so, being based on long term inflation adjusted contracts.

In my proposal the 50% growth equity can fill the gap by buying further income funds.

As regards your example of an ILG investor gaining from increasing capital after 30 years, surely the whole point of the exercise is to get maximum sustainable income now rather than in 2032 when most people who retired in 2002 would be dead.

0 -

"Corporate bonds wont increase with inflation…". From the GFC until end 2020 (before rates increased), they rose on average c.4% pa after distributions. With no capital growth the Inc. line would be flat. I do not know if that would always be expected but it seems a useful piece of empirical evidence.

1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards