We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

US Markets Risk

Comments

-

The S&P500 index appears to have achieved it in GBP terms over three of the last five 12 month periods, so never say never. The issue is such performance comes with considerable risk, even if it's been a long time since investors were reminded of that.

Others would remind us that such performance serves as a buffer against the inevitable downturns, such that attempts to trade in and out will generally lead to a worse outcome than time in the market. So a rational investor will determine suitable exposure and stick to that, at least until their personal circumstances change.

Whether you select index or managed funds for your exposure, the downside risks will always be there with a 100% equity fund.

0 -

"depends on the year and the state of the markets" doesn't fit easily with the idea of a target date and return, that must make planning quite hard - aiming for a specific equity performance in as little as a year is almost impossible given the volatility of equities. Most people would use other assets as a buffer so that if equities underperform for a few years they can still meet their targets, but requiring as much as 15% annual for mixed assets probably isn't sustainable in the very long run.

0 -

I start my financial year towards the end of April. The large investment houses issue their quarterly asset management reports at the start of April and I usually take a steer from them. Whilst those reports are US centric, they do provide useful insight into investing world thinking, ex US. From what I see at present, I can see no reason to change from my current allocations. The Japan wave continues to be worth at least 10% whilst EM also continues to warrant 20%/25%. Dev Asia appears to be strengthening with even more BRICS style trade agreements plus Thailand equities now have a unified governement base and have surged, which adds credibility to that regions 10%. So there's 40% just in the East alone, without even having to think about what might happen to the Western markets. Downside risks include TSMC and a weaker USD.

1 -

For those interested two further papers dealing with comparisons of the performance of mutual fund returns with those of buy and hold (both similar methodology to the mind the gap report)

Dichev, Ilia D., 2007. What are Stock Investors Actual Historical Returns? Evidence from

Dollar-weighted Returns (this was the paper I was thinking of and can be found at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=544142 )A UK version which separates out retail and institutional investors can be found at https://www.bayes.citystgeorges.ac.uk/__data/assets/pdf_file/0003/69933/Do-UK-retail-investors-buy-at-the-top-and-sell-at-the-bottom.pdf

Figure 1 in the latter (scroll to the bottom) shows that the difference in returns does vary with time. But overall, the median retail equity investor lost about 1.1% per year over the period studies compared to a buy and hold investor. The authors point out that "this annual performance gap of 1.17% for retail equity investors is a median value, in other words some investors would have experienced a much worse investment performance over this period." What they didn't mention was that some would have done better.

2 -

I had to come back to this one because I think many people probably don't completely understand what the phrase means, "don't try to beat the market".

There are two aspects to this. The first is, which market should we not try to beat, they all have different benchmarks so which one shouldn't we try to better? If you're in the UK market with an index tracker and you move to the US market with a similar type of tracker, you just beat the market! The second aspect is, there are loads of managed funds that regularly beat their benchmark, not every year but often. The question becomes, what's wrong with buying those funds and beating the market?

I think the more complete answer to the quiestion that was asked, is, if you want to beat the market, change the market you're in, which is largely what's being advocated in this thread.

0 -

I don't think the subject can be divided so simply and easily into two buckets, trading or investing, I think there are most probably other divisions or middle grounds, in between those two main headings. Investing or trading alone is too rigid and too simple. The fact that investors hold funds for an average 3.7 years is a testament to that.

1 -

Interesting that the latter paper shows evidence for bond markets being more feasible to market time, mirroring the suggestion made in a recent discussion here. I wonder what the data would look like for the 2020s when bonds went on quite a wild ride. Also interesting that the institutional money was not subject to the same whims and had a better outcome as a result.

The worst outcomes for retail investors are periods immediately following a market downturn, where they are probably pulling money out of markets or delaying investing and missing out on cheap prices, whereas they get their best results when bull markets are in full swing. This certainly seems to follow the pattern we see of overconfidence during the good times and pessimism when the best opportunities present themselves. Whereas institutional money was shown to seize the opportunity of the GFC, albeit not the dotcom crash.

I wonder about the distribution of outcomes around the median. I'd guess there'd be a fairly large bolus hugging the median with a long tail of more extreme outcomes where the investor made lucky or unlucky calls. But looking at short periods in isolation tells us nothing about aggregate performance, which is the more interesting factor.

The other topic mentioned was around the persistence of past performance and using this to predict which funds will perform well in the future. There's a useful meta-analysis at that digs into this and provides plenty of citations to individual studies conducted in various parts of the world.

If you conclude that it's not really feasible for individual funds to perform consistently, but that you, as a private investor can feasibly hop between them in response to your understanding of the prevailing economic weather, it begs the question why a professional fund manager running a global fund with a broad investment mandate could not do similar. But taking the overvaluation of the US as an example, you do have to get your timing right. Those who raised the alarm as early as 2014 would be very disappointed, as would those in 2017, or even 2021. Perhaps now is the right time to be worried, perhaps not. The same can be said for the rotation back into value funds, it may work out, it may not. Market sentiment will drive the outcome, and that cannot be predicted.

2 -

Perhaps because I spend a lot of time updating fund data and researching new funds, I do see evidence that many FM's regularly adjust their holdings to cater to whatever changes they see or anticpate. Some changes are quite large, other FM's freeze their contents which never seem to move. Initially it was the idea that if a FM can make those changes at the company level, why can't I make them at the fund level.

0 -

I thought that, of course changing markets is another slant. FTSE100 up that in 6 months, twice over 12 months.

0 -

Yes, benchmarking comparisons is an important consideration. I'd suggest that for a UK investor, using a cap weighted global index (e.g., FTSE All world index) as a benchmark for an equity portfolio is a reasonable option since few people would be entirely invested domestically nowadays. Comparing localised managed funds with the relevant index is also sensible (e.g., UK equity funds with the FTSE All Share).

The number of managed funds that beat the appropriate benchmark is small but does vary across reporting period and the assets under consideration. For example, according to https://www.spglobal.com/spdji/en/spiva/article/spiva-uk/ to mid-2024, in global equities, 80% of managed funds underperformed the index over a period of 1 year, and over 90% underperformed over periods of 3, 5, and 10 years. In other words, the number of managed funds that persistently outperformed the index was tiny (in fact it was only in corporate bonds where the managed funds did quite well).

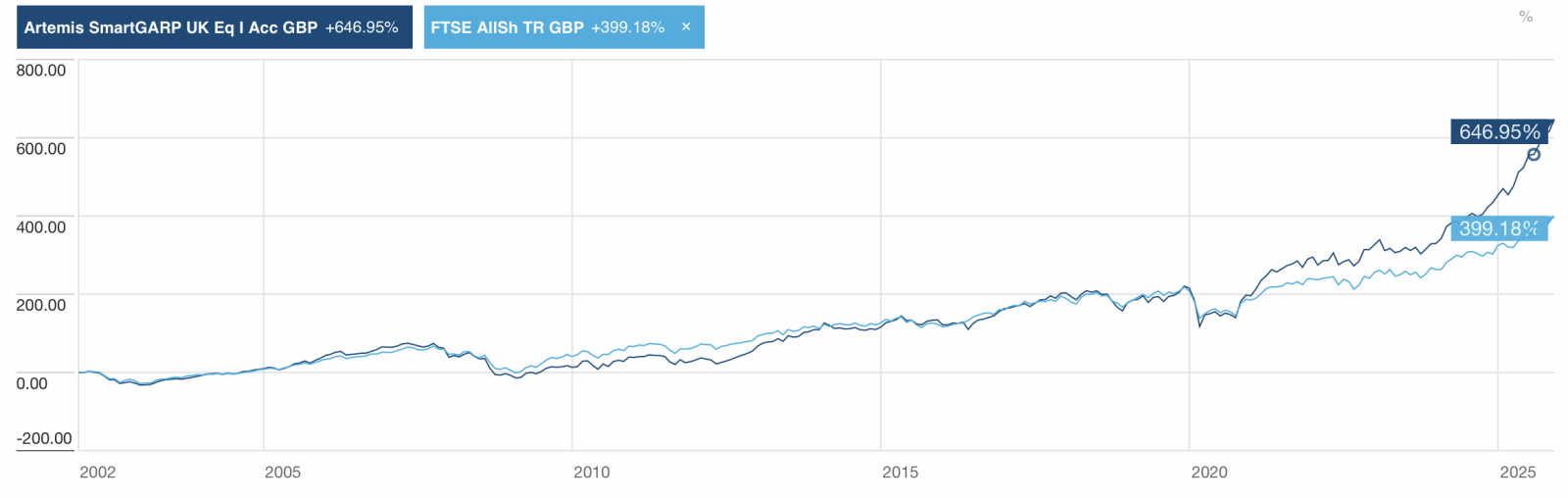

It is interesting to note that one of the funds you hold, Artemis SmartGARP UK equity generally matched the UK All-share index from 2002 (invention of the process?) to 2021 (although it was below after the GFC from 2009 to 2015), but has started to pull away since 2021 thanks to four excellent years (2021, 2022, 2024, and 2025). I have no idea whether that outperformance will continue in 2026. How well an investor will have done with this fund depends on when they started investing.

2

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards