We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

US Markets Risk

Comments

-

It seems to me that one of the OPs key requirements is that the approach should be enjoyable and fun. Investing in 2 or 3 trackers might achieve the same or a better results, but it's not going to meet those requirements.

1 -

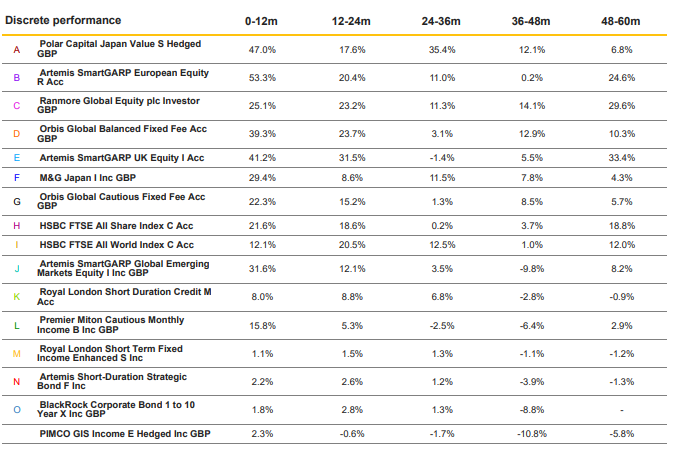

It's not correct to say that I only derisk once the target has been acheieved, risk is an important consideration throughout. The funds I chose this year are all well regarded funds, many of which I continue to hold, albeit it in lesser amounts now that I have reached my target. Time in the market is relative to the return but it is also relative to risk. I posted the funds previously elsewhere, here they are again.

1

1 -

I don't think we have a traditional approach here, but from the mind the gap reports, what most people seem to do is to change, perhaps in the hope of chasing better performance than leaving investments alone. So what you're doing is far from uncommon. Some of those changes will no doubt work out great, just, taken as a whole (across everyone), they don't.

For me, time frames of last five days, or even since start of the year, is definitely in the realms of trading, rather than investing, so for everything except for a fun portfolio I wouldn't take notice. But as mentioned above, this is perhaps effectively your fun portfolio.

0 -

I try to make it enjoyable but I have tremendous respect for money, it's difficult to earn and easy to lose so needs to be handled respectfully. I would never intentionally let the fun side overtake my risk aversion side, although that could happen inadvertently. I like to think I would do exactly the same things, in the same way, if my economic survival depneding on my success.

One of the differences between us is that I am more willing to respond to risk and threats and am not constrained by the stigma of "the rules" hanging over my head. I had held the US Index for several years but last year questioned the wisdom of continuing that hold, in light of what I percieved to be significant markets disruption, threats and opportunities elsewhere. I think that if you follow events and stay abreast of the economics landscape and form these views without acting on them, you probably shouldn't follow them in the first place or simply not invest, I mean, what's the point.

0 -

"I think that if you follow events and stay abreast of the economics landscape and form these views without acting on them, you probably shouldn't follow them in the first place or simply not invest, I mean, what's the point"

I'd counter that following events and staying abreast of the economic landscape while mostly sitting on my hands has allowed me to learn I am rubbish at picking next year's winners or predicting future returns without the associated harm to my wealth. Lessons that can only be learned by the current generation of investors if we return to more challenging investment conditions such as those seen after the dotcom boom.

It's true that I could make it more exciting by having a "fun portfolio" where I can speculate, but I don't need that to keep me interested. I see such an exercise as futile and would much rather focus on a coherent strategy that does not require chopping and changing. Understanding the economic landscape is vital in selecting appropriate long term building blocks to meet an objective.

4 -

The point about the passive approach is that, at least historically, 'good enough' results have generally been achieved by investing in the index (for UK investors, an international mix provided better outcomes than investing solely in the UK). Since investing in the index was not even an option until the 70s in the US and the 80s(?) in the UK, in reality investors would have picked a mix of the available investment trusts/mutual funds and individual stocks and hoped for the best. Given that investing costs were so much higher in the past (e.g., the first mutual funds I invested in had a 5% entry cost) this made switching an expensive business (IIRC, in the 70s and 80s, my father's stockbroker/FA visited once per year).

In other words, in the long-term holding a world equity index plus fixed income to taste (and age, risk tolerance etc.) has, over the years delivered better results than holding savings (e.g., easy access). So, investing, even with no knowledge or interest in world events and perceived risks, has generally provided the best means of building a decent retirement pot.

Responding to perceived risks by changing investments will have one of three outcomes compared to holding the index in that the new investments will do

- better

- the same, or

- worse

My contention is that beforehand it is impossible to predict which of these three outcomes will be realised, but over different periods the individual investor, unless particularly skilled, lucky, or blessed with a time machine, will probably see each of them with a longer term average of close to 'the same'.

A useful study beyond the 'Mind the gap' one would look at the outcomes for individual investors compared to the relevant index - I've a (very) vague recollection that such a thing exists (for US investors), but don't have time to look for it right now.

1 -

We have several different informed opinions in play. One refers to potential under performance by meddling with out performing funds, whilst another talks in terms of passives providing returns that are good enough. The difference between the returns on those two types of holdings could potentially be massive, which is why I think setting a target for the desired portfolio returns, is important, regardless of the type of fund chosen.

0 -

Agreed - question 1 should always be how much return do I need to in order to achieve my goals (over the entire lifetime of the target). That then informs how much risk is needed to be taken.

1 -

And given the target of 12-15%, the conversation appears to be what is the best way to beat the market.

0 -

"Usually", not always, it depends on the year and the state of the markets. But certainly this year (ending April). It's certain however that index trackers are never going to do that, by their very nature.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards