We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

ISA & Winter Fuel

bonalymacd

Posts: 2 Newbie

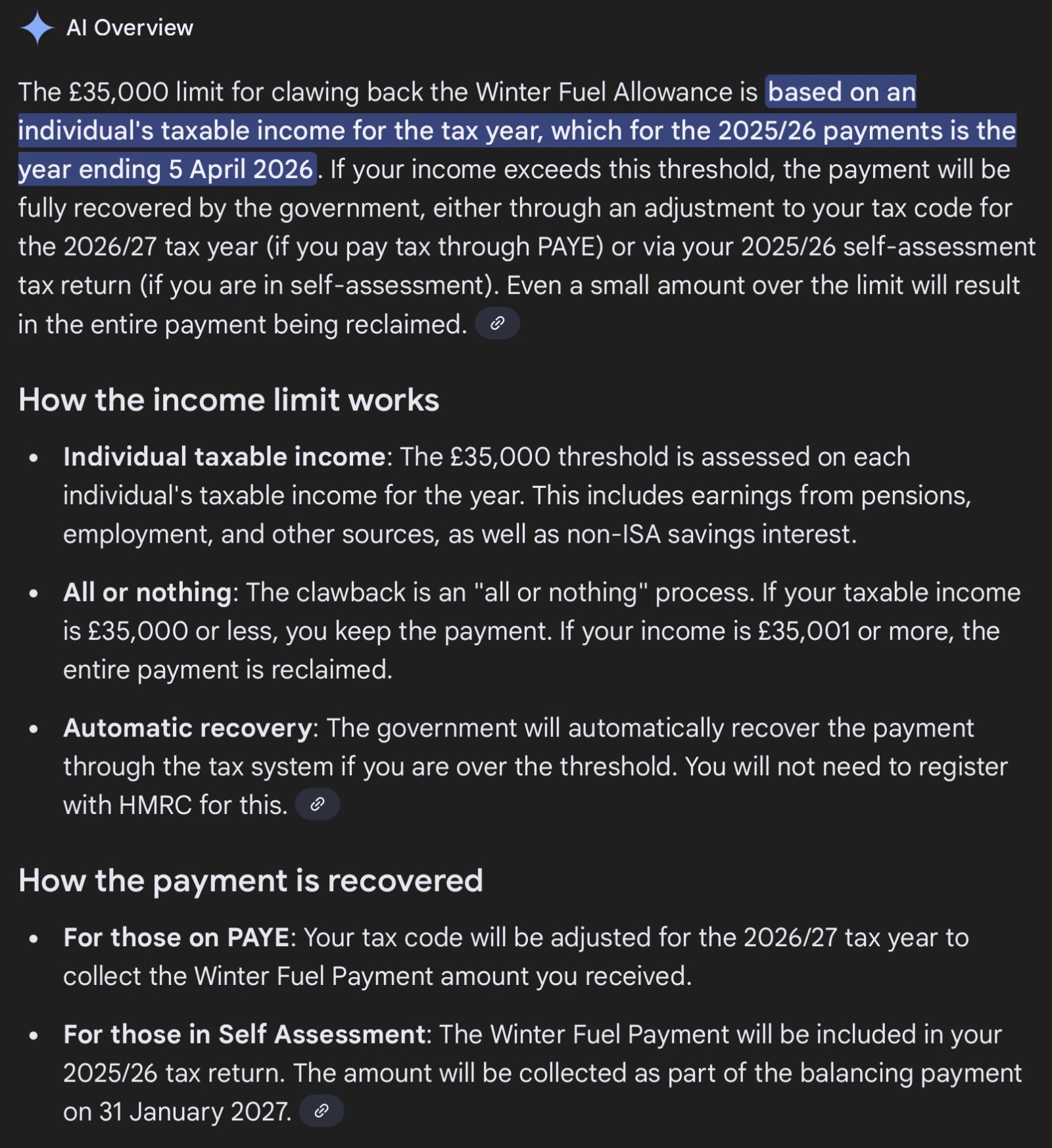

I am perilously near the 35,000 limit for clawing back the Winter Fuel allowance through my tax code, and it is touch and go whether I breach the £35,000 figure. My wife is not particularly near it.

We both have a decent holding in Cash Isa's. I was considering withdrawing some of my ISA and transferring it to hers, where it would obviously be treated as a new investment within her £20,000 limit for this year. Neither of us have used any of our 2025-26 £20,000 limit, and probably will not this year as interest rates are currently better elsewhere, and we do not earn enough to pay income tax on that interest.

Ignoring what may or may not happen in the budget, does anyone see any issues with this course of action?

We both have a decent holding in Cash Isa's. I was considering withdrawing some of my ISA and transferring it to hers, where it would obviously be treated as a new investment within her £20,000 limit for this year. Neither of us have used any of our 2025-26 £20,000 limit, and probably will not this year as interest rates are currently better elsewhere, and we do not earn enough to pay income tax on that interest.

Ignoring what may or may not happen in the budget, does anyone see any issues with this course of action?

0

Comments

-

Isn't it based on taxable income? If so, income earned in an Isa would be excluded so doing what you suggest wouldn't make any difference.bonalymacd said:I am perilously near the 35,000 limit for clawing back the Winter Fuel allowance through my tax code, and it is touch and go whether I breach the £35,000 figure. My wife is not particularly near it.

We both have a decent holding in Cash Isa's. I was considering withdrawing some of my ISA and transferring it to hers, where it would obviously be treated as a new investment within her £20,000 limit for this year. Neither of us have used any of our 2025-26 £20,000 limit, and probably will not this year as interest rates are currently better elsewhere, and we do not earn enough to pay income tax on that interest.

Ignoring what may or may not happen in the budget, does anyone see any issues with this course of action?

1 -

How would that help with regard to having to pay back the Winter Fuel Payment 🤔bonalymacd said:I am perilously near the 35,000 limit for clawing back the Winter Fuel allowance through my tax code, and it is touch and go whether I breach the £35,000 figure. My wife is not particularly near it.

We both have a decent holding in Cash Isa's. I was considering withdrawing some of my ISA and transferring it to hers, where it would obviously be treated as a new investment within her £20,000 limit for this year. Neither of us have used any of our 2025-26 £20,000 limit, and probably will not this year as interest rates are currently better elsewhere, and we do not earn enough to pay income tax on that interest.

Ignoring what may or may not happen in the budget, does anyone see any issues with this course of action?

1 -

Can't see the point. Interest from Cash ISAs is not taxable so won't count toward the £35k anyway. Might be worth using some of your ISA allowance. Interest from non-ISA accounts would presumably be "taxable" even if you don't pay any tax on it.0

-

If you were going to take any action, it would be moving money that is in taxable savings accounts in your name to taxable savings accounts in your wife's name. Taxable interest (Easy Access Savings, Regular Savers etc) counts towards the £35,000, interest earned by ISAs is disregarded.1

-

But you do have to be careful about how you do it, particularly if you would be closing accounts as that could move when interest is paid forwards into the current tax year.Kim_13 said:If you were going to take any action, it would be moving money that is in taxable savings accounts in your name to taxable savings accounts in your wife's name. Taxable interest (Easy Access Savings, Regular Savers etc) counts towards the £35,000, interest earned by ISAs is disregarded.

And moving money from an account that is due to next pay interest on say 30/04/2026 isn't going to help either.1 -

As above, is your £35k income or savings?bonalymacd said:I am perilously near the 35,000 limit for clawing back the Winter Fuel allowance through my tax code, and it is touch and go whether I breach the £35,000 figure. My wife is not particularly near it.

We both have a decent holding in Cash Isa's. I was considering withdrawing some of my ISA and transferring it to hers, where it would obviously be treated as a new investment within her £20,000 limit for this year. Neither of us have used any of our 2025-26 £20,000 limit, and probably will not this year as interest rates are currently better elsewhere, and we do not earn enough to pay income tax on that interest.

Ignoring what may or may not happen in the budget, does anyone see any issues with this course of action?

The following article might help you. Is the new Winter Fuel Payment £35,000 threshold for an individual or a household? STEVE WEBB replies | This is Money2 -

Of course, any account that is being withdrawn from should be left open with at least the minimum balance to avoid interest being paid any earlier than it has to be.Dazed_and_C0nfused said:

But you do have to be careful about how you do it, particularly if you would be closing accounts as that could move when interest is paid forwards into the current tax year.Kim_13 said:If you were going to take any action, it would be moving money that is in taxable savings accounts in your name to taxable savings accounts in your wife's name. Taxable interest (Easy Access Savings, Regular Savers etc) counts towards the £35,000, interest earned by ISAs is disregarded.

And moving money from an account that is due to next pay interest on say 30/04/2026 isn't going to help either.

With an ISA allowance remaining, the easiest thing to do would be to use it so that your savings stay in your name. Although the rate is lower now, it will remain tax free year after year and help you to stay under the £35,000 in future tax years. I suspect it will be frozen and like the tax bands, more people will be fiscal dragged into it. The ISA allowance is very likely to be lower in 26/27, especially for cash.0 -

bonalymacd said:I am perilously near the 35,000 limit for clawing back the Winter Fuel allowance through my tax code, and it is touch and go whether I breach the £35,000 figure. My wife is not particularly near it.

We both have a decent holding in Cash Isa's. I was considering withdrawing some of my ISA and transferring it to hers, where it would obviously be treated as a new investment within her £20,000 limit for this year. Neither of us have used any of our 2025-26 £20,000 limit, and probably will not this year as interest rates are currently better elsewhere, and we do not earn enough to pay income tax on that interest.

Ignoring what may or may not happen in the budget, does anyone see any issues with this course of action?

If it's the £100 each you are talking about you should have said you didn't want your payment.bonalymacd said:I am perilously near the 35,000 limit for clawing back the Winter Fuel allowance through my tax code, and it is touch and go whether I breach the £35,000 figure. My wife is not particularly near it.

We both have a decent holding in Cash Isa's. I was considering withdrawing some of my ISA and transferring it to hers, where it would obviously be treated as a new investment within her £20,000 limit for this year. Neither of us have used any of our 2025-26 £20,000 limit, and probably will not this year as interest rates are currently better elsewhere, and we do not earn enough to pay income tax on that interest.

Ignoring what may or may not happen in the budget, does anyone see any issues with this course of action?

Then your wive would possibly receive £2000 -

Thanks for all the feedback. I Know ISA interest isn't taxable, but the Winter fuel limit is based on income. But wasn't aware that ISA interest income was specifically excluded.0

-

It is based on a particular bit of the calculation of tax liability as eplained here.bonalymacd said:Thanks for all the feedback. I Know ISA interest isn't taxable, but the Winter fuel limit is based on income. But wasn't aware that ISA interest income was specifically excluded.

https://www.taxadvisermagazine.com/article/202526-winter-fuel-payments-and-pension-age-winter-heating-payments-ps35000-income-limit0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards