We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Equity market crash ?

Comments

-

This feels like the early days of a self-fulfilling prophecy1

-

Presumably shortly followed by the biggest gains in 'absolute value'.

Context is everything, and from my recollection, the falls in April had not even eroded gains from the preceding year.2 -

No doubt this subject (of whether it should or shouldn't be allowed) as been discussed many times and/or isn't allowed to be discussed - I'm not sure. Either way, politics is a major driver of investments. Perhaps a discussion ought to be allowed in that context?subjecttocontract said:World Politics will play a big part in stock market performance and there is a long list of things that could happen. But we aren't allowed to discuss politics on this forum so we'll all have to wait until something happens.0 -

Political debate is not allowed because it often leads to partisan squabbling and derails threads, leading to work for the forum team. This is first and foremost a money saving forum, so any non-moneysaving posts (including my one) are potentially at risk of being removed. Though there is a separate board for discussing forum policies and rules: https://forums.moneysavingexpert.com/categories/forum-policy-rules-discussionmichael1234 said:

No doubt this subject (of whether it should or shouldn't be allowed) as been discussed many times and/or isn't allowed to be discussed - I'm not sure. Either way, politics is a major driver of investments. Perhaps a discussion ought to be allowed in that context?subjecttocontract said:World Politics will play a big part in stock market performance and there is a long list of things that could happen. But we aren't allowed to discuss politics on this forum so we'll all have to wait until something happens.

4 -

Doesn't that depend on which definition of a crash you are using? No doubt you'll point me to THE definition but regardless, I suspect the OP meant a crash bigger than last April.

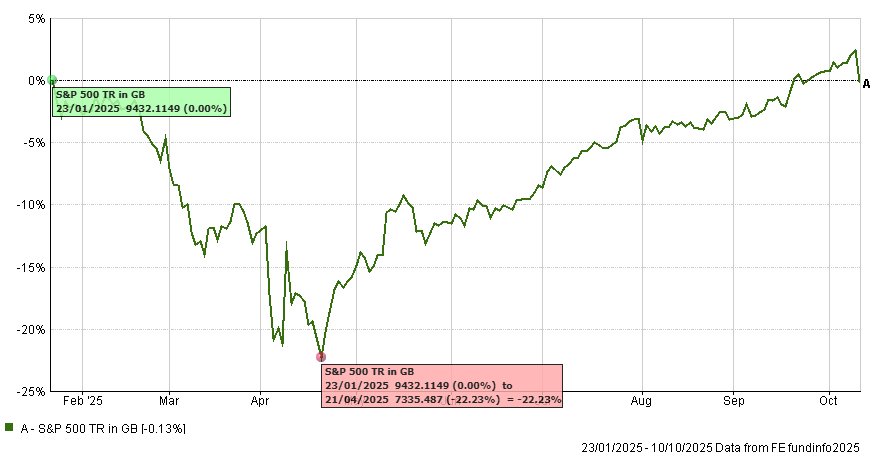

S&P500 fell by 22.23% earlier in the year for those invested in Sterling.

23/01/2025 was the peak, and 21/04/2025 was the trough, and after Friday's fall, it is lower than in January.

There have been times over the years when UK investors were shielded from the S&P crashing because of currency movements going the other way.

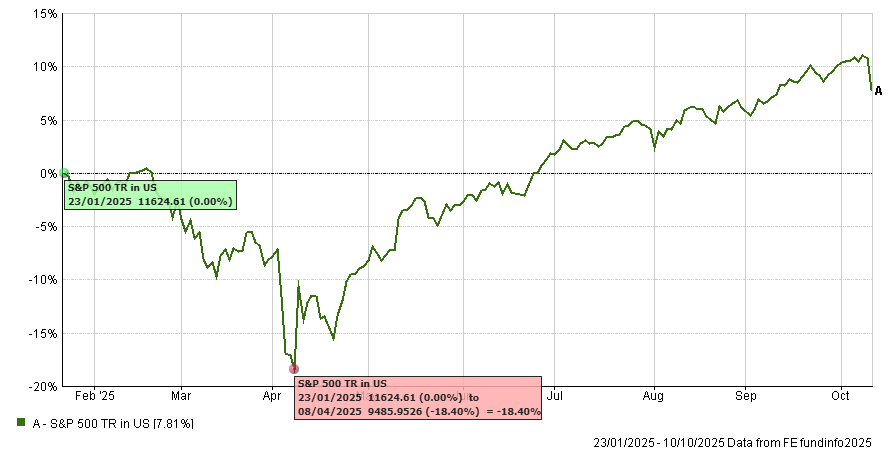

Here is the same chart for those using dollars (i.e. Americans and those that currency hedge to dollars):

Note that the peak and trough for dollars was different to Sterling as well as the recovery point

So, whilst in dollar terms it didn't crash (18.4% just short of the often used 20% reference point), for Sterling investors it did crash at 22.23%

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.7 -

Hence the use of the quotation marks and the allusion to cousins. I used "4% rule" as a name for such SWR models as Trinity or Bengen are not as widely known.dunstonh said:Like we all know equity markets always crash every so oftenAbout 1 in 4 years has a crash and the last one was earlier this year.Your investing strategy should take account of crashes that will certainly occur. In Drawdown that's why we have the "4% rule" and it's cousins and tools like annuities.As this is a UK site, the US 4% SWR won't apply. UK is closer to 3.5% in your 60s and 3.0% in your 50s.And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

However trying to predict the effect of events that have not yet occurred is more guesswork than politics.subjecttocontract said:World Politics will play a big part in stock market performance and there is a long list of things that could happen. But we aren't allowed to discuss politics on this forum so we'll all have to wait until something happens.1 -

I agree and have for many years been planning 1/35th drawdown from 55 around 2.86%.dunstonh said:

As this is a UK site, the US 4% SWR won't apply. UK is closer to 3.5% in your 60s and 3.0% in your 50s.

However with inflation linked annuity rates at around 4.25% from 55 then it seems rational to take profits from the equities and switch into long dated inflation linked bonds to synchronise with annuity prices until 55 to get around 50% more income without needing to worry about when markets might next crash. It's quite a mindset change after being 100% equities during the years bonds were so overvalued. For the past few days I've been trying to think of any good reason to still hold any equities in my pensions.

5 -

Once you've met your goals, definitely. No need to take any more risk than needed.Alexland said:

I agree and have for many years been planning 1/35th drawdown from 55 around 2.86%.dunstonh said:

As this is a UK site, the US 4% SWR won't apply. UK is closer to 3.5% in your 60s and 3.0% in your 50s.

However with inflation linked annuity rates at around 4.25% from 55 then it seems rational to take profits from the equities and switch into long dated inflation linked bonds to synchronise with annuity prices until 55 to get around 50% more income without needing to worry about when markets might next crash. It's quite a mindset change after being 100% equities during the years bonds were so overvalued. For the past few days I've been trying to think of any good reason to still hold any equities in my pensions.3 -

So you can make more and more money and have a really BIG pension pot. ( even if you do not really need oneAlexland said:

I agree and have for many years been planning 1/35th drawdown from 55 around 2.86%.dunstonh said:

As this is a UK site, the US 4% SWR won't apply. UK is closer to 3.5% in your 60s and 3.0% in your 50s.

However with inflation linked annuity rates at around 4.25% from 55 then it seems rational to take profits from the equities and switch into long dated inflation linked bonds to synchronise with annuity prices until 55 to get around 50% more income without needing to worry about when markets might next crash. It's quite a mindset change after being 100% equities during the years bonds were so overvalued. For the past few days I've been trying to think of any good reason to still hold any equities in my pensions.") )

)

More seriously, my view is more about maintaining diversification.

If I look at the big picture of our household finances, including value of home, pension, S&S ISAs, cash savings, state pension, DB pension etc I can make an approx guess that the % of equity is just less than 20%.

In the long run that might just help to keep us ahead of inflation.

Whether that is a sensible way to look at, I am not really sure !1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards