We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Being nosey... How many Regular Saver accounts do you have?

Comments

-

Non! because saving money is a mugs gametopyam said:Starting to find this is addictive!

I have five now..

How many does everybody else on here have?0 -

Are you aware that there are a couple of Monmouth 7% reg savers available ?Middle_of_the_Road said:

Make that 20......just applied for the Monmouthshire 6% 😂Middle_of_the_Road said:

Have 19 at this time. Not worked out monthly funding total or amount deposited. I could have applied for more, but trying not to open accounts with any more providers, as feel it could become too burdensome.Bobblehat said:I wonder if there are any closet RS enthusiasts browsing this forum that are too shy to contribute?

Unfortunately, I'm not expert enough with the forum's search facility to know how to search for them, but I'd never add in their past admissions anyway without their say so, as they can easily do it themselves here if they wished to play")

The whole savings mindset I find, can become an obsession, and distract one from enjoying other important aspects of life that I feel are pleasureable.0 -

Err ... you may have stumbled into the wrong forum!GringoGoesToVagas said:

Non! because saving money is a mugs gametopyam said:Starting to find this is addictive!

I have five now..

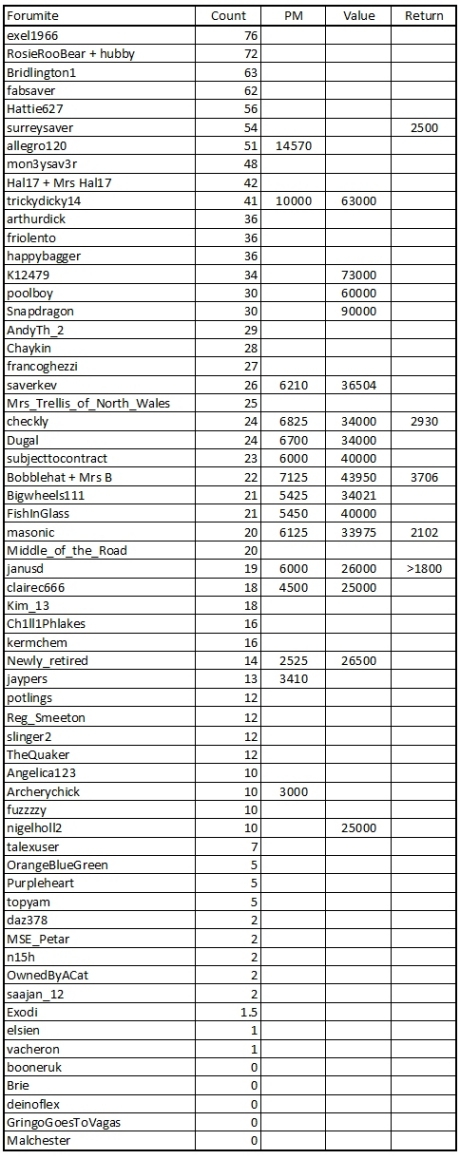

How many does everybody else on here have?Compiler of the RS League Table.

https://forums.moneysavingexpert.com/discussion/6670416/how-many-regular-savers-do-you-have-the-league-table/p15 -

There were, now NLA. Existing customers only too… did those who opened them without having been members on the specified date ever have Mon BS close the accounts?subjecttocontract said:

Are you aware that there are a couple of Monmouth 7% reg savers available ?Middle_of_the_Road said:

Make that 20......just applied for the Monmouthshire 6% 😂Middle_of_the_Road said:

Have 19 at this time. Not worked out monthly funding total or amount deposited. I could have applied for more, but trying not to open accounts with any more providers, as feel it could become too burdensome.Bobblehat said:I wonder if there are any closet RS enthusiasts browsing this forum that are too shy to contribute?

Unfortunately, I'm not expert enough with the forum's search facility to know how to search for them, but I'd never add in their past admissions anyway without their say so, as they can easily do it themselves here if they wished to play

The whole savings mindset I find, can become an obsession, and distract one from enjoying other important aspects of life that I feel are pleasureable.0 -

Did see mention of them, but never looked into them that closely as my only easy access funds were in a CMC ISA at a good rate at the time.subjecttocontract said:

Are you aware that there are a couple of Monmouth 7% reg savers available ?Middle_of_the_Road said:

Make that 20......just applied for the Monmouthshire 6% 😂Middle_of_the_Road said:

Have 19 at this time. Not worked out monthly funding total or amount deposited. I could have applied for more, but trying not to open accounts with any more providers, as feel it could become too burdensome.Bobblehat said:I wonder if there are any closet RS enthusiasts browsing this forum that are too shy to contribute?

Unfortunately, I'm not expert enough with the forum's search facility to know how to search for them, but I'd never add in their past admissions anyway without their say so, as they can easily do it themselves here if they wished to play

The whole savings mindset I find, can become an obsession, and distract one from enjoying other important aspects of life that I feel are pleasureable.0 -

What I think you are missing is that you should not be investing all your cash. The advice is generally to keep around 6 months’ income as cash/cash equivalent for emergencies. So even those maxing their stocks and shares ISAs should hold some cash.Exodi said:Usually 1 or 2.

While I'm a big advocate of Regular Savers, there are several things that hinder my ability to go crazy like other forumites.

Firstly is opportunity cost. If I have surplus cash and I don't need the money in the short-medium term, I'd likely be better off investing the money instead. My current (tax-free) XIRR on investments is around double the rate you can get from Regular Savers.

It's also worth remembering that all Regular Savers are taxable. A higher rate tax payer for example, could exceed their PSA with no previous savings, by just contributing the maximum to ~4 RS accounts over a year. This would effectively turn a 7% First Direct Regular Saver into 4.2%. While still not bad, it's certainly not as exciting as it might first appear.

I appreciate that everyone's situation is different, but it's hard to imagine people with double digit numbers of Regular Saver accounts are not paying tax on the interest, unless they're just making minimum contributions (to which you'd wonder what the point was). For some, if they have some of their ISA allowance available to them, they might be better off putting the money in there than another Regular Saver.

Of course there's also those that have more money than they know what to do with. Those that have maxed out theirs and their partners ISA allowances in April, don't want (or it is impractical, e.g. due to stage in life) to invest and accept they will pay tax on interest.Regular Savers generally offer the best return for that cash, outperforming the average return on Premium Bonds even after tax. To maximise your return on the 6 months of income held as cash would likely require a double digit number of Regular Savers (whilst avoiding those like First Direct which don’t allow penalty free access) spread out across the year.1 -

There are plenty of regular savers which allow unlimited withdrawals or closure without penalty, so are a useful home for your emergency funds.LZC said:

What I think you are missing is that you should not be investing all your cash. The advice is generally to keep around 6 months’ income as cash/cash equivalent for emergencies. So even those maxing their stocks and shares ISAs should hold some cash.Exodi said:Usually 1 or 2.

While I'm a big advocate of Regular Savers, there are several things that hinder my ability to go crazy like other forumites.

Firstly is opportunity cost. If I have surplus cash and I don't need the money in the short-medium term, I'd likely be better off investing the money instead. My current (tax-free) XIRR on investments is around double the rate you can get from Regular Savers.

It's also worth remembering that all Regular Savers are taxable. A higher rate tax payer for example, could exceed their PSA with no previous savings, by just contributing the maximum to ~4 RS accounts over a year. This would effectively turn a 7% First Direct Regular Saver into 4.2%. While still not bad, it's certainly not as exciting as it might first appear.

I appreciate that everyone's situation is different, but it's hard to imagine people with double digit numbers of Regular Saver accounts are not paying tax on the interest, unless they're just making minimum contributions (to which you'd wonder what the point was). For some, if they have some of their ISA allowance available to them, they might be better off putting the money in there than another Regular Saver.

Of course there's also those that have more money than they know what to do with. Those that have maxed out theirs and their partners ISA allowances in April, don't want (or it is impractical, e.g. due to stage in life) to invest and accept they will pay tax on interest.Regular Savers generally offer the best return for that cash, outperforming the average return on Premium Bonds even after tax. To maximise your return on the 6 months of income held as cash would likely require a double digit number of Regular Savers (whilst avoiding those like First Direct which don’t allow penalty free access) spread out across the year.1 -

Sorry, I'm late to the party. Currently sitting on 16 in total (from 12 providers), though some end in the next month.Bobblehat said:I wonder if there are any closet RS enthusiasts browsing this forum that are too shy to contribute?

Unfortunately, I'm not expert enough with the forum's search facility to know how to search for them, but I'd never add in their past admissions anyway without their say so, as they can easily do it themselves here if they wished to play

Had been trying to keep the number of providers I use on the low side, but as I've got into investing and used my ISA allowance in a S&S ISA, regular savers have become my main savings method. This time last year it was 9 from 6 providers so definitely is starting to become a bit of a hobby.1 -

Some more additions ...

Compiler of the RS League Table.

https://forums.moneysavingexpert.com/discussion/6670416/how-many-regular-savers-do-you-have-the-league-table/p11 -

@ThePirates I wasn't aware that RSs have the maturity option that allows the funds to be transferred to another RS account with the same provider e.g., Principality - unless I've misread that. Or do you mean something else?ThePirates said:@n15h I'd go Principality before Provincial

Higher rate and when you choose maturity options that allow you to have duplicate accounts you are quids in!

I'm on 4 Principally accounts now even thought the 'rules' suggest you can only have 1.

Thousands of candles can be lit from a single candle, and the life of the candle will not be shortened. Happiness never decreases by being shared - Buddha0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards