We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Annuity 5% increase per year or RPI

Comments

-

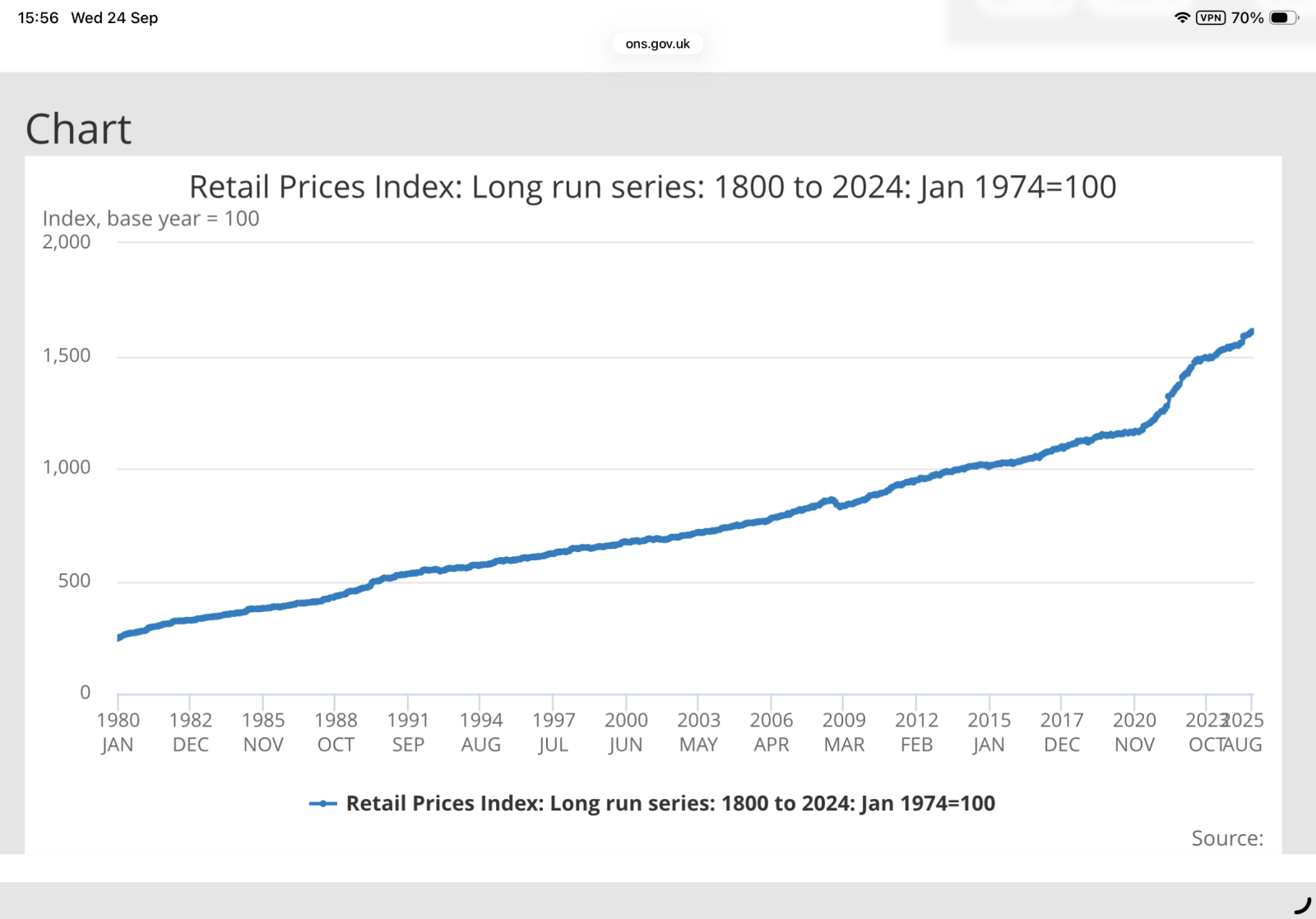

10% or 20% average inflation over an entire retirement would wreck plans for millions. Lots of DBs and annuities with fixed or capped increases would lose much of their value.

Historically it's never been that high as a long term average rate in the UK, although it got close to 10% through the 70s and 80s. ( Trailing 20 year average annual inflation was over 9% from 1980 to 1993). Prudent to at least consider the possibility of a repeat.

The years below were the peak annual rates. Retire in 1970 at the beginning of that period, and by 1990 a 5% fixed increase pension or annuity would be worth almost 60% less than at the start.1982 8.6 1981 11.88 1980 17.97 1979 13.42 1978 8.26 1977 15.84 1976 16.56 1975 24.21 1974 16.04 1973 9.2 1972 7.07 1971 9.44 1970 6.37 4 -

I get it. I have some very complex models projecting every eventually of a DB scheme from the ages of 55 to 65, plus varying lump sums.FIREDreamer said:

He is assuming future RPI from the same starting point for an RPI annuity ! Why not do a quote assuming 10%, 20% or 30% then? 🤷♂️Cobbler_tone said:

I understand that but I'm assuming they wouldn't be the starting numbers. If they are you would take the 4%FIREDreamer said:

Those are RPI annuities that start at the same value (obviously) and he is making those assumptions about future RPI increases post annuity purchase.Cobbler_tone said:

P.S. that table above reminds me of one of mine on the respective ages of taking a DB pension. Seems strange to have the same starting annuity for 2.5%, 3% and 4%?

You will always net out 'worse off' at some point, but how do you value some happier years up front? Potentially priceless.

I don't get the top line, if I am reading it right. Maybe it just isn't described clearly:

It suggests you can have a level annuity for life of £16,349.

Or you can have a lifetime annuity of £9,794 with 5% annual increases. I also understand adding 2.5%-4% per year but must have missed what the £11,584 is. I (wrongly) assumed they were the quotes for the annuity from the £16,349 for 2.5%-4% increases.

My mindset has always been, if I would have been better off after 20 years I'll take the jam now. I figure that if I will be 'technically' worse off that far in the future it won't make a tangible difference to my life. Like most things, 'it depends' is usually the answer based on everyone's personal circumstances. e.g. we recently inherited a significant amount which we (rightfully) never factored into our retirement planning.

If you are relying on your annuity and state pension pooled together to get by, then RPI protection makes sense. Always a balanced decision based on security, affordability and appetite to risk.1 -

The £11,584 is the annuity Available with RPI increases.Cobbler_tone said:

I get it. I have some very complex models projecting every eventually of a DB scheme from the ages of 55 to 65, plus varying lump sums.FIREDreamer said:

He is assuming future RPI from the same starting point for an RPI annuity ! Why not do a quote assuming 10%, 20% or 30% then? 🤷♂️Cobbler_tone said:

I understand that but I'm assuming they wouldn't be the starting numbers. If they are you would take the 4%FIREDreamer said:

Those are RPI annuities that start at the same value (obviously) and he is making those assumptions about future RPI increases post annuity purchase.Cobbler_tone said:

P.S. that table above reminds me of one of mine on the respective ages of taking a DB pension. Seems strange to have the same starting annuity for 2.5%, 3% and 4%?

You will always net out 'worse off' at some point, but how do you value some happier years up front? Potentially priceless.

I don't get the top line, if I am reading it right. Maybe it just isn't described clearly:

It suggests you can have a level annuity for life of £16,349.

Or you can have a lifetime annuity of £9,794 with 5% annual increases. I also understand adding 2.5%-4% per year but must have missed what the £11,584 is. I (wrongly) assumed they were the quotes for the annuity from the £16,349 for 2.5%-4% increases.

My mindset has always been, if I would have been better off after 20 years I'll take the jam now. I figure that if I will be 'technically' worse off that far in the future it won't make a tangible difference to my life. Like most things, 'it depends' is usually the answer based on everyone's personal circumstances. e.g. we recently inherited a significant amount which we (rightfully) never factored into our retirement planning.

If you are relying on your annuity and state pension pooled together to get by, then RPI protection makes sense. Always a balanced decision based on security, affordability and appetite to risk.

0 -

I've been playing for hours on the Money Helper annuity tool, very helpful and interesting.

I espically liked the comparison of the payments achieved between using 3,4,5% & RPI.

In my case, the RPI sat in between the 4 & 5% fixed quotes.

One main reason I'm again looking at annuities or PLAs is to maintain living standards/buying power whatever inflation does, so I'm feeling more happy to just cover inflation eventualities and hopefully switch off personal emotions that are yet to be experienced as time goes by.

I'm currently feeling doing 2 annuities, one RPI & one 3 or 4% fixed to achieve a balancing in my head.

I'm now playing with the guarantee period (years) and the value protection (%) to see what I feel on this aspect of it.

I understand any value protection payment is put back in to my estate so in the IHT zone.

I'm just wondering how a guarantee period works after death, I'm wondering if them years of output can be passed to children or friends and possibly not falling under the IHT zone and said people just paying their marginal income tax.

****

I did a quick googling about annuity payments after death, it needs more investigation and how will stuff change from April 2027, but the option of putting children or friends as beneficial people appears easy enough as spouse will not require these funds is the plan.

Link below for supplementary information.

****

https://techzone.aberdeenadviser.com/public/pensions/Tech-guide-pensions-IHT?hl=en-GB#:~:text=For lifetime annuities, if the,and the 'two year rule'

0 -

af1963 said:

The years below were the peak annual rates. Retire in 1970 at the beginning of that period, and by 1990 a 5% fixed increase pension or annuity would be worth almost 60% less than at the start.1982 8.6 1981 11.88 1980 17.97 1979 13.42 1978 8.26 1977 15.84 1976 16.56 1975 24.21 1974 16.04 1973 9.2 1972 7.07 1971 9.44 1970 6.37 Yes, and if you lived and worked through those years and then retired in the early 1980s then you wanted an RPI-linked annuity. But if the table were continued then you realise that RPI was then below 5% for the next 15 years.An RPI-linked annuity (or CPI or CPIH) buys certainty though.

0 -

Gotcha. Obviously no right/wrong answer and so much context needed, including age and other provisions.

In my position I'd go drawdown or flat, or fixed term annuity. I personally wouldn't even consider the 5% option.

If it was your only income (with the state pension) then RPI protection may be the way to go.0 -

I prefer the HL calculator but they both do the same thing.RogerPensionGuy said:I've been playing for hours on the Money Helper annuity tool, very helpful and interesting.0 -

A great data shot here above, tks af1963.af1963 said:10% or 20% average inflation over an entire retirement would wreck plans for millions. Lots of DBs and annuities with fixed or capped increases would lose much of their value.

Historically it's never been that high as a long term average rate in the UK, although it got close to 10% through the 70s and 80s. ( Trailing 20 year average annual inflation was over 9% from 1980 to 1993). Prudent to at least consider the possibility of a repeat.

The years below were the peak annual rates. Retire in 1970 at the beginning of that period, and by 1990 a 5% fixed increase pension or annuity would be worth almost 60% less than at the start.1982 8.6 1981 11.88 1980 17.97 1979 13.42 1978 8.26 1977 15.84 1976 16.56 1975 24.21 1974 16.04 1973 9.2 1972 7.07 1971 9.44 1970 6.37

This is a great example of sequence of sequences risk, just imagine any people that were the wrong side of them numbers and had locked in and it formed a large % of all their income.

Altho annuities hopefully provide more lifestyle stability and less emotions that trying to ride/navigate the stockmarkets, this example above easily shows there is ample opportunity to select annuities that may produce a bumpy ride.

Many of us on here have worked many decades to secure reasonable pensions, annuities are typically a one shot product(not some term annuities I know) but this thread is very helpful in my head as I go towards buying an annuity or 2.

Many thanks to all contributing posters.1 -

The added complication with RPI is the RPI could be averaging 8% per year but the RPI for the mth of the annuity increase could be , say 4%, meaning the RPI increase could be less than the average RPI for that year.It's just my opinion and not advice.2

-

But that will come out in the wash in the following year’s increases as inflation is cumulative.SouthCoastBoy said:The added complication with RPI is the RPI could be averaging 8% per year but the RPI for the mth of the annuity increase could be , say 4%, meaning the RPI increase could be less than the average RPI for that year.

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards