We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Annuity 5% increase per year or RPI

Comments

-

Agree with the recent posts on ensuring that you can live comfortably with as much inflation proofing as possible.

DB + SP + RPI*/CPI annuity.

You can then determine your appetite for risk once you've determined your capacity for it.

Yes, many people do spend more early in retirement, but declining health may also mean you need to pay someone else for maintaining the garden, cleaning and potentially personal care.

*RPI will be calculated as CPIH eventually, which has historically been closer to CPI."Real knowledge is to know the extent of one's ignorance" - Confucius1 -

As has been observed by many people on here your personal inflation rate may bear little resemblance to the "official" rate of RPI. Even if you take the sensible step of getting an RPI annuity you could still find yourself short. So just don't put all your eggs in one basket - keep some assets in other pots (savings equities gilts gold comics whatever you think best)saajan_12 said:This isn't about what makes the most money - even with a great forecast, its just that and the reality could be higher or lower. Its about matching your costs so you don't run out of money.

Eg if the crystal balls all say that with 70% certainty, RPI is expected to be less than 5% over your lifetime. So 70% of the time, you're better off with the 5% fixed. But lets your main costs are food, clothes. energy, holidays, which all rise with inflation. Then in 30% of the time, inflation is high and you're short of money. Vs if you stick with an RPI linked annuity, then in 100% of cases you can live comfortably, even though you've given up some profits in 70% of cases.

If you have well more than you need to live comfortably, THAT is what I would consider investing to maximise returns.2 -

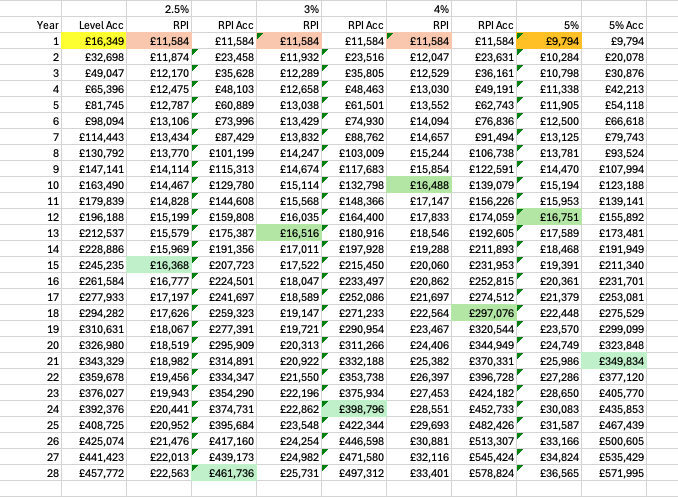

Another illustration - this time including RPI and 3 possible average rates - with no account taken for sequence of returns on the RPI, plus no allowance made for earlier excess income from the options with the larger starting amounts.These quotes are all single life, non guaranteed, age about 61, slightly enhanced.If we get a few years of 10% inflation again the RPI options would quickly start to outperform the others.The green highlighted figure are the break evens compared to a level annuity.Comparing 5% with RPI the only scenario that breaks even in terms of accumulated funds is the 4% RPI.Annually 5% starts lowest - but could catch up 2.5% RPI within 8 years.

update: all starting figures are for a £200k purchase 2

2 -

I'm in a quandary as to whether I will take an annuity. If I do I think I will go for an rpi annuity.It's just my opinion and not advice.0

-

Reduces the stress of retirement so you don’t have to see your funds plummet and worrying if you can continue your income. I am 61 and my RPI annuities are paying 4.5% of my purchase money which I am happy with. I sleep well at night.SouthCoastBoy said:I'm in a quandary as to whether I will take an annuity. If I do I think I will go for an rpi annuity.0 -

Isn't this just a variation on the numerous choices we all make when making pension decisions and investment choices?

Reminds me exactly of the DB debates on early reduction factors, amounts of lump sums etc.

It is all about (relative) risk, peace of mind and the ultimate factor (that we don't normally have the answer for) of how long do we have left! Surely it is about having 'enough'. e.g. IMO if you bought a 5% annuity and a couple of years of 10% inflation saw you desolate, then you probably didn't have 'enough' to start with. It's a bit like saying that if you started with a drawdown pot and it dropped 10% over a period of 20 years that you'd be in big trouble.

My lived experience (from those around me) tells me that you need less money as you get older, certainly late 70's onwards. The irony being that everyone I know just generates more. Unless of course you still intend to be travelling the world and have grand plans. Your aim might be to try to build a war chest on the off chance you need a care home, which I always find a bit sad as a bookend to your life....i.e. you are born, work and save to live and then save to die. I also know that some people have more motivation to provide for their kids (who won't be 'kids') than they do for themselves.

P.S. that table above reminds me of one of mine on the respective ages of taking a DB pension. Seems strange to have the same starting annuity for 2.5%, 3% and 4%?

You will always net out 'worse off' at some point, but how do you value some happier years up front? Potentially priceless.0 -

Those are RPI annuities that start at the same value (obviously) and he is making those assumptions about future RPI increases post annuity purchase.Cobbler_tone said:

P.S. that table above reminds me of one of mine on the respective ages of taking a DB pension. Seems strange to have the same starting annuity for 2.5%, 3% and 4%?

You will always net out 'worse off' at some point, but how do you value some happier years up front? Potentially priceless.1 -

I understand that but I'm assuming they wouldn't be the starting numbers. If they are you would take the 4%FIREDreamer said:

Those are RPI annuities that start at the same value (obviously) and he is making those assumptions about future RPI increases post annuity purchase.Cobbler_tone said:

P.S. that table above reminds me of one of mine on the respective ages of taking a DB pension. Seems strange to have the same starting annuity for 2.5%, 3% and 4%?

You will always net out 'worse off' at some point, but how do you value some happier years up front? Potentially priceless. 0

0 -

Correct you can't specify a percentage when you buy an RPI annuity - although you can get capped RPI.

I've just assumed 3 different average RPI rates - to show when you are ahead and behind.

I think the most likely long termRPI rates is between 2.5% and 3%

You could of course spend more to get a larger starting amount - these were for a £200k purchase/0 -

He is assuming future RPI from the same starting point for an RPI annuity ! Why not do a quote assuming 10%, 20% or 30% then? 🤷♂️Cobbler_tone said:

I understand that but I'm assuming they wouldn't be the starting numbers. If they are you would take the 4%FIREDreamer said:

Those are RPI annuities that start at the same value (obviously) and he is making those assumptions about future RPI increases post annuity purchase.Cobbler_tone said:

P.S. that table above reminds me of one of mine on the respective ages of taking a DB pension. Seems strange to have the same starting annuity for 2.5%, 3% and 4%?

You will always net out 'worse off' at some point, but how do you value some happier years up front? Potentially priceless.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards