We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Annuity 5% increase per year or RPI

Comments

-

And the RPI cap is 2.5% for benefits accrued from 6 April 2005, and 5% for benefits accrued between 6 April 1997 and 5 April 2005 inclusive.DRS1 said:

If you are both talking about LPI it is a cap.Andy_L said:

its a statutory minimum, not a capJohnnyboy11 said:According to the below Briefing Note, for most private sector DB schemes in payment, there is a statutory cap on indexation, currently 2.5%:2 -

What's a cap on DB pensions got to do with the OPs question?

3

3 -

My dad retired in 1985 on a company final-salary pension. A few years later (I don't remember exactly when) the company decided to wind-up the pension scheme and use the reserves to buy annuities for the retired members. Dad spent a lot of time arguing that there was enough money in the fund to buy annuities that increased by RPI, but the company / actuaries claimed there was only enough to buy 5% escalating.RPI had been over 5% from 1970 to 1983 without a break, but was then under 5% from 1992 until 2021.My dad had 5% "forced on him", and for nearly 20 years his pension increased by more than inflation.Don't look at what inflation has been over the last few years in deciding what sort of annuity to buy - what you really need is a crystal ball.But, an RPI or CPI linked annuity still buys certainty of always being able to match inflation.

3 -

If an annuity is increased by rpi, what fugure does it take, the month the annuity was bought or the last 12 mth average, or something else? either way you may not capture the true inflation especially if it spiked for 1 mth.It's just my opinion and not advice.0

-

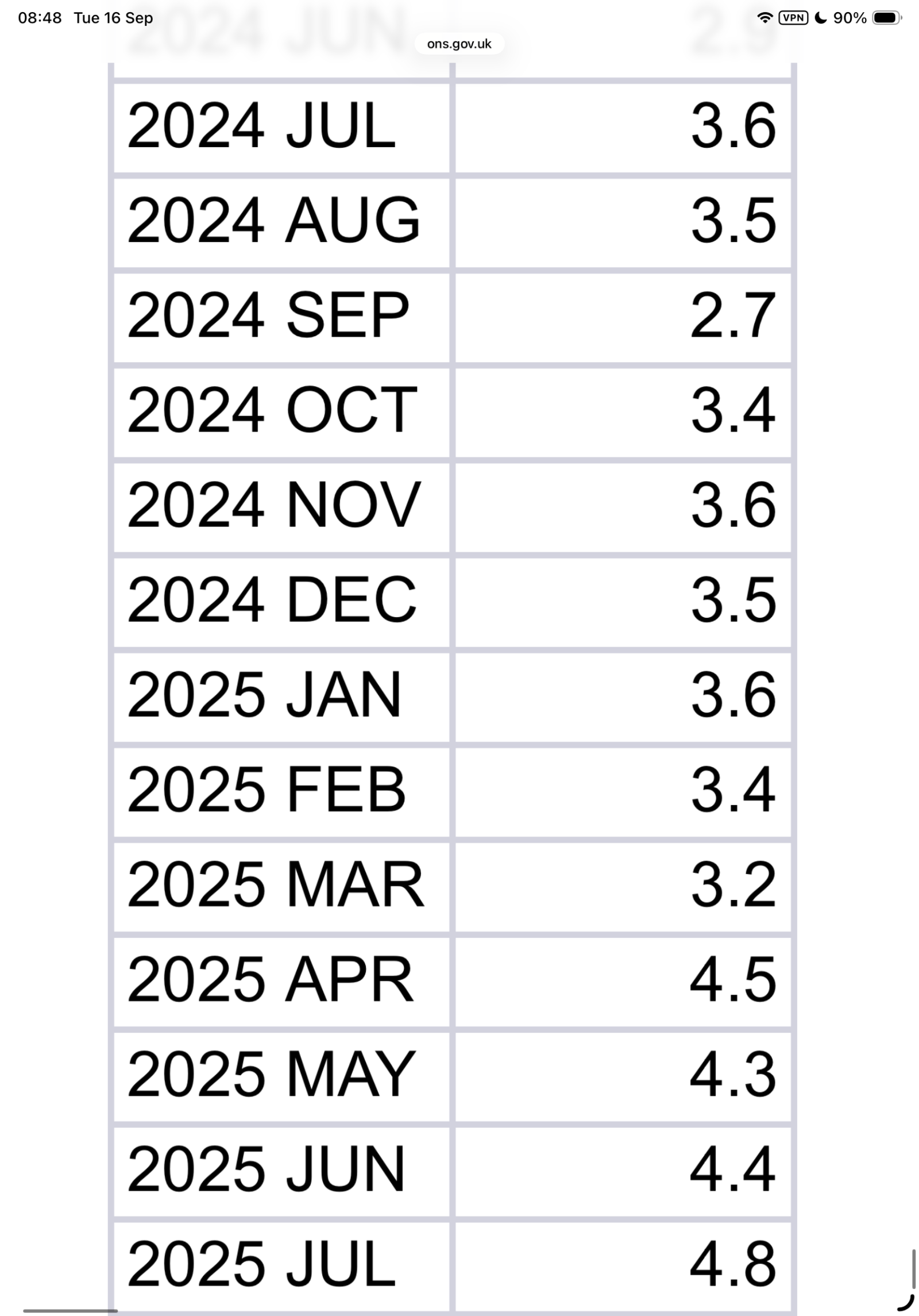

One of my RPI annuities started in Nov 2023.SouthCoastBoy said:If an annuity is increased by rpi, what fugure does it take, the month the annuity was bought or the last 12 mth average, or something else? either way you may not capture the true inflation especially if it spiked for 1 mth.

The first increase effective from Nov 2024 was 3.5% which was the August 2024 rate announced in September 2024.

I guess I find out my November 2025 increase tomorrow, Hopefully it is around the 4.8% announced last month for July 2025. It could be even more.

2 -

its the minimum maximum (or possibly the maximum minimum ;-) )DRS1 said:

If you are both talking about LPI it is a cap.Andy_L said:

its a statutory minimum, not a capJohnnyboy11 said:According to the below Briefing Note, for most private sector DB schemes in payment, there is a statutory cap on indexation, currently 2.5%:

by law they have to provide inflation linked indexation up to a maximum of 2.5% (5% for pension accrued before X date?)

but that level of indexation is the minimum they have to provide. They are free to offer more than that (eg unlimited inflation) ie there is no legislation that bans them from providing more than 2.5%1 -

Assuming the income bought at the start is exactly sufficient for your needs then

RPI annuity

Inflation<=5%. Annuity will provide income sufficient for needs

Inflation>5%. Annuity will provide income sufficient for needs

5% escalation

Inflation<=5%. Annuity income will exceed that required for needs

Inflation>5%. Annuity income will fall below that required for needs

For the RPI annuity the real income is independent of inflation, while for the 5% escalation one outcome is nice to have, but not essential, while the other outcome is bad. Since, none of us know what inflation will do over the next few decades, the level of that risk is unknown.

As per the post of @FIREDreamer, most index linked income will have a date on which it is adjusted (e.g., April for the SP, anniversary for annuities*?) based on the annual inflation of a few months earlier. In other words, there is always a lag (even gilts have a lag of 3 months) which, from the POV of the retiree, is detrimental when inflation is increasing and a boost when inflation is falling.

* I assume (anyone know?) income from fixed escalation annuities are also adjusted annually rather than monthly.

0 -

Annuities usually increase annually on the anniversary of their commencement. I have yet to see one that increases in any other way.OldScientist said:Assuming the income bought at the start is exactly sufficient for your needs then

RPI annuity

Inflation<=5%. Annuity will provide income sufficient for needs

Inflation>5%. Annuity will provide income sufficient for needs

5% escalation

Inflation<=5%. Annuity income will exceed that required for needs

Inflation>5%. Annuity income will fall below that required for needs

For the RPI annuity the real income is independent of inflation, while for the 5% escalation one outcome is nice to have, but not essential, while the other outcome is bad. Since, none of us know what inflation will do over the next few decades, the level of that risk is unknown.

As per the post of @FIREDreamer, most index linked income will have a date on which it is adjusted (e.g., April for the SP, anniversary for annuities*?) based on the annual inflation of a few months earlier. In other words, there is always a lag (even gilts have a lag of 3 months) which, from the POV of the retiree, is detrimental when inflation is increasing and a boost when inflation is falling.

* I assume (anyone know?) income from fixed escalation annuities are also adjusted annually rather than monthly.3 -

If you're asking "which out of 5% or RPI will give me the most money" no-one can possibly know.

If you're asking "which out of 5% or RPI will give me the best protection against inflation" then clearly it's RPI.

1 -

The problem with RPI annuities is they backload your returns. By definition, you'll get the highest nominal payment in the month (year) you die. Yes, they provide longevity insurance, but anecdotal experience is that cash is more fun in your 60s and 70s and tails off in your 80s and beyond. Be careful not to have too little whilst you can enjoy the benefit and end up with too much when it's too late.3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards