We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Is the 4% rule still applicable today?

Comments

-

For somebody who doesn't know they might assume the "R" refer to rule rather than rate.Stubod said:I think the problem is some people are assuming that 4%, (or 3.5% in UK or whatever), is a "rule", when it is in fact only a guide to give an indication on what is achievable based on historical data, no more, no less?2 -

The other side of the equation is how much income you need. So reducing fixed costs like mortgages, car loans etc while you are working will take enormous pressure off your need to generate retirement income.Cobbler_tone said:

That is the bottom line really.michaels said:

I think that depends on what proportion of income is baseline day to day spend.Linton said:

The problem I see with approaches which automatically increase or decrease drawdown is how you implement them in reality. If your guardrail suddenly cuts your income by 10% how do you decrease your expenditure accordingly?Gary1984 said:Indeed. This is probably the best argument for using some sort of guardrails approach. Instead of 4% of the initial, target something like 3.5% to 4.5% of the current fund. Start with 4% and increase for inflation each year but if your current withdrawal rate exceeds 4.5% of the current pot then reduce it by 10%. Similarly if your withdrawal rate goes below 3.5% increase it by 10%.

So in the above scenario Alice's rate is 40/670 = 6% so she reduces her withdrawal from 40k to 36k and continues to make similar reductions each year until she's back in range.

Bob (60/710 = 8.5%) should reduce as well but will probably have a few more years of reductions than Alice before he gets back in range unless investments bounce back quickly.

Obviously there's an infinite choice in parameters when setting the guardrails and haircut/boost to incomes but it seems more intuitive than just setting a rate and sticking to it no matter what.

Most of one’s ongoing expenditure is fixed well in advance, eg utilities, council tax, just keeping to the standard of living you are used to. Holidays, particularly expensive ones, may be booked a year previously. Anything you can do quickly seems pretty petty. Go for cheaper wines? Turn the winter heating down by a degree? Cancel your booking for a visit to your favourite restaurant?

Conversely in a market boom why take extra drawdown if you don’t actually need the money?

Your retirement financial management strategy should be based on your needs, you should not expect to change your lifestyle to meet the ongoing requirements of the strategy.

A lot of people on here have a good base of a DB pension. Others will buy a decent annuity.

It is common sense really. If you have £1m in a pot and intend to spend £50k for 25 years and the markets plummet for a few years, you are probably going to start twitching, or realise you probably aren't going to have £50k a year.

If anything (IMO) it bolsters the argument of getting a healthy guaranteed income of buying an annuity.

Conventional wisdom has people investing in both equity and bonds funds with the bond funds supposedly providing some stability, but the last few years have shown how volatile even they can be. If you are going to buy an annuity at retirement maybe you should start early and have an individual Gilts ladder held to maturity. I'm not sure if you can buy "deferred annuities" in the UK, but in the US you can buy such products that guarantee a minimum interest rate and linked to the current market rates. At retirement there are cash out options or you can buy an annuity. They are good replacement for a DB pensions.And so we beat on, boats against the current, borne back ceaselessly into the past.1 -

It's why some people struggle with the idea of a hard drop from £120k gross joint earnings to £40k gross joint pension, which is what we are doing. I know we will be very comfortable. We spend under £2,000 net a month between us and that involves a lot of clothing packages through the post and a significant cava bill.Bostonerimus1 said:

The other side of the equation is how much income you need. So reducing fixed costs like mortgages, car loans etc while you are working will take enormous pressure off your need to generate retirement income.Cobbler_tone said:

That is the bottom line really.michaels said:

I think that depends on what proportion of income is baseline day to day spend.Linton said:

The problem I see with approaches which automatically increase or decrease drawdown is how you implement them in reality. If your guardrail suddenly cuts your income by 10% how do you decrease your expenditure accordingly?Gary1984 said:Indeed. This is probably the best argument for using some sort of guardrails approach. Instead of 4% of the initial, target something like 3.5% to 4.5% of the current fund. Start with 4% and increase for inflation each year but if your current withdrawal rate exceeds 4.5% of the current pot then reduce it by 10%. Similarly if your withdrawal rate goes below 3.5% increase it by 10%.

So in the above scenario Alice's rate is 40/670 = 6% so she reduces her withdrawal from 40k to 36k and continues to make similar reductions each year until she's back in range.

Bob (60/710 = 8.5%) should reduce as well but will probably have a few more years of reductions than Alice before he gets back in range unless investments bounce back quickly.

Obviously there's an infinite choice in parameters when setting the guardrails and haircut/boost to incomes but it seems more intuitive than just setting a rate and sticking to it no matter what.

Most of one’s ongoing expenditure is fixed well in advance, eg utilities, council tax, just keeping to the standard of living you are used to. Holidays, particularly expensive ones, may be booked a year previously. Anything you can do quickly seems pretty petty. Go for cheaper wines? Turn the winter heating down by a degree? Cancel your booking for a visit to your favourite restaurant?

Conversely in a market boom why take extra drawdown if you don’t actually need the money?

Your retirement financial management strategy should be based on your needs, you should not expect to change your lifestyle to meet the ongoing requirements of the strategy.

A lot of people on here have a good base of a DB pension. Others will buy a decent annuity.

It is common sense really. If you have £1m in a pot and intend to spend £50k for 25 years and the markets plummet for a few years, you are probably going to start twitching, or realise you probably aren't going to have £50k a year.

If anything (IMO) it bolsters the argument of getting a healthy guaranteed income of buying an annuity.

Most of what we earn goes on pensions and tax. If you have no mortgage, rent or debts you don't actually need that much, especially when your 'holidays abroad' itch has already been scratched. We just want peace!0 -

The reduction of fixed costs to take pressure off your retirement income is why I advocate paying off your mortgage before you stop working and control IFA and other financial fees which might be 10% or 20% of drawdown given the average fees charged. If you can DIY it’s a big saving in expenses.Cobbler_tone said:

It's why some people struggle with the idea of a hard drop from £120k gross joint earnings to £40k gross joint pension, which is what we are doing. I know we will be very comfortable. We spend under £2,000 net a month between us and that involves a lot of clothing packages through the post and a significant cava bill.Bostonerimus1 said:

The other side of the equation is how much income you need. So reducing fixed costs like mortgages, car loans etc while you are working will take enormous pressure off your need to generate retirement income.Cobbler_tone said:

That is the bottom line really.michaels said:

I think that depends on what proportion of income is baseline day to day spend.Linton said:

The problem I see with approaches which automatically increase or decrease drawdown is how you implement them in reality. If your guardrail suddenly cuts your income by 10% how do you decrease your expenditure accordingly?Gary1984 said:Indeed. This is probably the best argument for using some sort of guardrails approach. Instead of 4% of the initial, target something like 3.5% to 4.5% of the current fund. Start with 4% and increase for inflation each year but if your current withdrawal rate exceeds 4.5% of the current pot then reduce it by 10%. Similarly if your withdrawal rate goes below 3.5% increase it by 10%.

So in the above scenario Alice's rate is 40/670 = 6% so she reduces her withdrawal from 40k to 36k and continues to make similar reductions each year until she's back in range.

Bob (60/710 = 8.5%) should reduce as well but will probably have a few more years of reductions than Alice before he gets back in range unless investments bounce back quickly.

Obviously there's an infinite choice in parameters when setting the guardrails and haircut/boost to incomes but it seems more intuitive than just setting a rate and sticking to it no matter what.

Most of one’s ongoing expenditure is fixed well in advance, eg utilities, council tax, just keeping to the standard of living you are used to. Holidays, particularly expensive ones, may be booked a year previously. Anything you can do quickly seems pretty petty. Go for cheaper wines? Turn the winter heating down by a degree? Cancel your booking for a visit to your favourite restaurant?

Conversely in a market boom why take extra drawdown if you don’t actually need the money?

Your retirement financial management strategy should be based on your needs, you should not expect to change your lifestyle to meet the ongoing requirements of the strategy.

A lot of people on here have a good base of a DB pension. Others will buy a decent annuity.

It is common sense really. If you have £1m in a pot and intend to spend £50k for 25 years and the markets plummet for a few years, you are probably going to start twitching, or realise you probably aren't going to have £50k a year.

If anything (IMO) it bolsters the argument of getting a healthy guaranteed income of buying an annuity.

Most of what we earn goes on pensions and tax. If you have no mortgage, rent or debts you don't actually need that much, especially when your 'holidays abroad' itch has already been scratched. We just want peace!And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

The bolded bit basically requires you to buy an annuity as the only way to guarantee not having to change your lifestyle in response to market conditions. Otherwise you're choosing between some kind of variable income, or a step function, with level income until the day it runs out, then zero.Linton said:

The problem I see with approaches which automatically increase or decrease drawdown is how you implement them in reality. If your guardrail suddenly cuts your income by 10% how do you decrease your expenditure accordingly?Gary1984 said:Indeed. This is probably the best argument for using some sort of guardrails approach. Instead of 4% of the initial, target something like 3.5% to 4.5% of the current fund. Start with 4% and increase for inflation each year but if your current withdrawal rate exceeds 4.5% of the current pot then reduce it by 10%. Similarly if your withdrawal rate goes below 3.5% increase it by 10%.

So in the above scenario Alice's rate is 40/670 = 6% so she reduces her withdrawal from 40k to 36k and continues to make similar reductions each year until she's back in range.

Bob (60/710 = 8.5%) should reduce as well but will probably have a few more years of reductions than Alice before he gets back in range unless investments bounce back quickly.

Obviously there's an infinite choice in parameters when setting the guardrails and haircut/boost to incomes but it seems more intuitive than just setting a rate and sticking to it no matter what.

Most of one’s ongoing expenditure is fixed well in advance, eg utilities, council tax, just keeping to the standard of living you are used to. Holidays, particularly expensive ones, may be booked a year previously. Anything you can do quickly seems pretty petty. Go for cheaper wines? Turn the winter heating down by a degree? Cancel your booking for a visit to your favourite restaurant?

Conversely in a market boom why take extra drawdown if you don’t actually need the money?

Your retirement financial management strategy should be based on your needs, you should not expect to change your lifestyle to meet the ongoing requirements of the strategy.

I will admit though that your analysis of the difficulty of making changes would hold much more true for someone used to living paycheck to paycheck. Most of the regular posters on here are definitely not in that category") 1

1 -

The replacement of DB pensions by DC pensions is the genesis of SWR modeling for retirement in an attempt to see how much someone can "safely" withdraw. Ideally people will live a lifestyle within their means while they are working allowing them to invest and to have that compound so they can fund their retirement comfortably. The FIRE (Financial Independence Retire Early) movement takes that to extremes with frugality and saving and investing maybe 50% of your income. However, that sort of approach requires a fairly high level of income to start with so you can actually afford the basics. Increasingly the fixed costs of daily living consume more and more of many people's wages. So the cost of living stops people from saving for retirement and poor financial skills hampers them even further. I see a bit of a time bomb in the UK as the full impact of the transition to DC pensions explodes - maybe we should go back to forcing people to buy an annuity? Or maybe give people the option of using the 25%tax free lump sum to buy an annuity or put it into drawdown but pay the tax on it. Or go back to employer provided DB pensions and increase NI to bring the UK SP closer to the level of other OECD country retirement benefits.Triumph13 said:

The bolded bit basically requires you to buy an annuity as the only way to guarantee not having to change your lifestyle in response to market conditions. Otherwise you're choosing between some kind of variable income, or a step function, with level income until the day it runs out, then zero.Linton said:

The problem I see with approaches which automatically increase or decrease drawdown is how you implement them in reality. If your guardrail suddenly cuts your income by 10% how do you decrease your expenditure accordingly?Gary1984 said:Indeed. This is probably the best argument for using some sort of guardrails approach. Instead of 4% of the initial, target something like 3.5% to 4.5% of the current fund. Start with 4% and increase for inflation each year but if your current withdrawal rate exceeds 4.5% of the current pot then reduce it by 10%. Similarly if your withdrawal rate goes below 3.5% increase it by 10%.

So in the above scenario Alice's rate is 40/670 = 6% so she reduces her withdrawal from 40k to 36k and continues to make similar reductions each year until she's back in range.

Bob (60/710 = 8.5%) should reduce as well but will probably have a few more years of reductions than Alice before he gets back in range unless investments bounce back quickly.

Obviously there's an infinite choice in parameters when setting the guardrails and haircut/boost to incomes but it seems more intuitive than just setting a rate and sticking to it no matter what.

Most of one’s ongoing expenditure is fixed well in advance, eg utilities, council tax, just keeping to the standard of living you are used to. Holidays, particularly expensive ones, may be booked a year previously. Anything you can do quickly seems pretty petty. Go for cheaper wines? Turn the winter heating down by a degree? Cancel your booking for a visit to your favourite restaurant?

Conversely in a market boom why take extra drawdown if you don’t actually need the money?

Your retirement financial management strategy should be based on your needs, you should not expect to change your lifestyle to meet the ongoing requirements of the strategy.

I will admit though that your analysis of the difficulty of making changes would hold much more true for someone used to living paycheck to paycheck. Most of the regular posters on here are definitely not in that categoryAnd so we beat on, boats against the current, borne back ceaselessly into the past.1 -

Bostonerimus1 said:

Conventional wisdom has people investing in both equity and bonds funds with the bond funds supposedly providing some stability, but the last few years have shown how volatile even they can be. If you are going to buy an annuity at retirement maybe you should start early and have an individual Gilts ladder held to maturity. I'm not sure if you can buy "deferred annuities" in the UK, but in the US you can buy such products that guarantee a minimum interest rate and linked to the current market rates. At retirement there are cash out options or you can buy an annuity. They are good replacement for a DB pensions.

Getting well OT, but...

AFAIK, deferred annuities of the type available in the US (as in pay a premium now and receive x income y years later) are not currently available in the UK.

As you suggest, a simple replacement for a deferred RPI annuity is, in the run up to retirement, to steadily buy inflation linked gilts that mature at or close to the expected retirement date. This does leave one open to interest rate risk. At the expense of more complexity, the interest rate risk can be mitigated by buying ILG (or ILG funds) that have a weighted duration similar to that of the proposed annuity (roughly equal to half the life expectancy at purchase plus the delay time).1 -

There are tradeoffs with portfolio withdrawals between flexibility and portfolio longevity (or robustness). At the extremes:

Constant inflation adjusted withdrawals provide constant real income until the portfolio is exhausted when the income falls to zero. If and when that will happen in future retirements is unknown (but we can look at the past for guidance).

Percentage of portfolio withdrawals (e.g., a constant percentage, or increasing percentages such as VPW and ABW) provide variable income (which might be small) but will not go to zero.

Of course, it is possible to mix these two strategies to give a hybrid solution that will then, for good or bad, mix the properties of both.

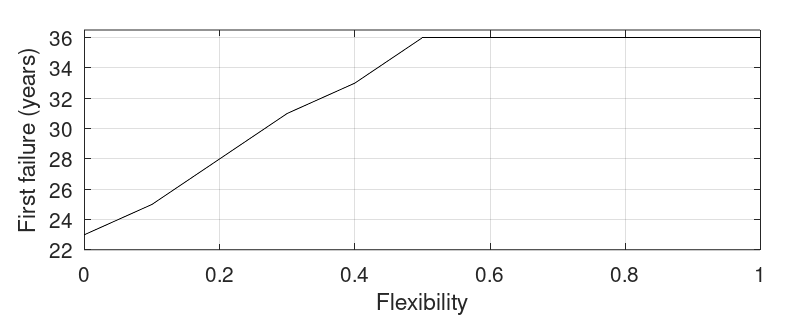

So, here are the results from some historical modelling (see end of post for details).

In the first graph, the first year of failure is plotted as a function of flexibility (flexibility of 0=constant inflation adjusted withdrawals, 1=pure percentage of portfolio, 0.5 represents a 50/50 mix of both)

With constant inflation adjusted withdrawals, the first failure occurred 23 years after retirement – this steadily increases with more flexibility (note: since I have only modelled 35 year retirements, ‘36’ in the above graph means ‘greater than 35’)

In the second graph, I’ve plotted failure rate (i.e., the fraction of historical retirements where the portfolio went to zero before 35 years) as a function of flexibility

With constant inflation adjusted withdrawals, 13% of historical retirements saw the portfolio fall to zero before 35 years had elapsed. Increasing the flexibility decreased the failure rate reaching a value of zero with flexibility of about 0.5.

In the third graph, I’ve plotted the worst case mean real withdrawals over 35 years (expressed as a percentage of the initial portfolio)

In the worst case for constant inflation adjusted withdrawals, the mean was 2.6% (i.e., 4% was delivered for 23 years and 0% for the final 12 years, giving a mean of 4*23.35=2.6). The minimum mean value increased with flexibility reaching a value of about 3.2% (of course, the year to year variability will also increase as flexibility is increased)

Overall, a retiree capable of accepting some flexibility in income will have a more robust plan than one who can't.

Details of modelling:

Returns and inflation from macrohistory.net

30% US stocks, 30% UK stocks, 20% UK bonds, 20% cash

Constant inflation adjusted withdrawals were 4% and percentage of portfolio withdrawals started at 4% and increased by 0.2 percentage points each year (i.e., 4.0%, 4.2%, 4.4%, …).

A 35 year retirement

0 -

A fascinating little analysis OldScientist. Thank you. Is the reason you have upped the variable percentage by 0.2% pa because you are aiming for portfolio depletion? I'm always nervous of such an approach in case one ends up living longer than expected. Fortunately I have inheritance as a key aim so I'm happy with a constant perecntage.

Plenty of off the shelf lifestyling funds are available Bostoneremus1 where assets are progressively moved into suitable gilt funds to try to minimise last minute volatility in the amount of annuity income that can be purchased. They have long been the standard for work DC pensions before the drawdown freedoms came in and are probably worth the marginally higher fees for most people vs trying to manage the locking in of annuity rates themselves. I do agree that, unless annuity rates crash again in another bond bubble, we definitely need to move back to annuities being the default position for the average pensioner. I fear that won't happen until we have an awful lot of people screw up their drawdown.

0 -

This is a graph produced by a historic stress testing tool, using a £1m portfolio in an uncrystallised pension.. Withdrawals are £40K per year net after tax, increasing with historic inflation.

Retiring at age 60.

864 scenarios were modelled starting in 1915 using historic market data.

No state pension assumed.

100% Equities in this case but you can simulate various allocations. 0.3% charges.

According to this software, there is a 99% chance of reaching age 98, and in no case would you run out of money before age 89. 98 was chosen as it's the date when there is less than 10% probability of being alive.

So according to this tool, the 4% rule actually works in 99% of the time for UK retirees if you use 100% equity allocation! In fact it's even more than 4% since I input £40K net spend and there was £6K of tax in year 1, giving 4.6% withdrawal rate. This seems to go against other research findings but there you go.

The software uses UFPLS withdrawals to model the tax payable throughout the plan.

If you add in a full new state pension from age 67, the success rate unsurprisingly goes to 100%.

Red line is the worst case scenario which was 1915. 1969 also failed but you ran out of money at age 94. 2000-2008 is not included as there are not enough years after that for the model to work.

She shaded bands are the likely (30 to 70 percentile), less likely, and rare scenarios.

The bigger thing to note around SWR, is that even in the less likely lower scenario band, you ended up with more money than you started - if using this approach you will highly likely be able to increase your spend over time.

Also interesting to note - reducing the equity allocation below 100% gives worse results, but any equity allocation 50% or more gave 95%+ success rates and 100% to age 81. 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards