We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is the 4% rule still applicable today?

Comments

-

Succinctly said - and such good advice from Bostonerimus1

Spend less than you make

Almost never borrow money (only exception is a mortgage)

Invest as much as you can within pensions and ISAs

Educate your children about money and set them up with JISAs asap.0 -

Another way of looking at fees is that they will reduce (unknown) future returns by x%.Bostonerimus1 said:

But at the start of drawdown a 0.5% fee reduces your spending by 0.5%. So the impact of fees are highest right where sequence of returns risk is highest, of course this assumes fees stay the same. I think it's best to go into retirement with your fixed costs reduced as much as possible, so no mortgage and IFA and fund fees as low as possible. I you can DIY that's an obvious way to give a 16% (0.5%/3.0%) boost to your income.westv said:

I thought it was closer to 0.5% which equates to 0.25% reduction over the length of drawdown.Ibrahim5 said:The average IFA fee is 0.8% so 4% without an IFA is equivalent to 3.2% with an adviser's fingers in your pot. That's assuming an adviser is as good at managing the investments, which in my experience they are nowhere near.

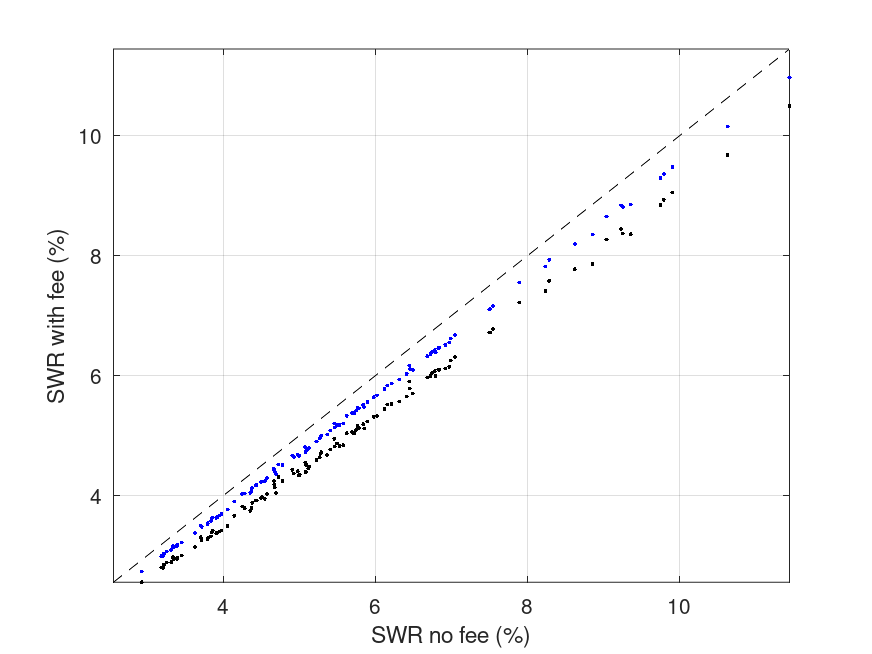

Out of interest, I've plotted the 30-year SWR (Uk retiree with 60/20/20 portfolio) with fees against the SWR without fees for UK historical retirements in the following graph (black dots are for a 1.0% fee, blue dots for a 0.5% fee, and the dashed line is where the SWR with or without fees would be equal)

1) Fairly obviously, higher fees led to a lower SWR in every case!

2) The difference in MSWR tended to be greater for better retirements (i.e., those with higher SWR)

3) Since the difference in SWR was slightly different for cases with similar no fee SWR, then sequence of returns does have a small effect.

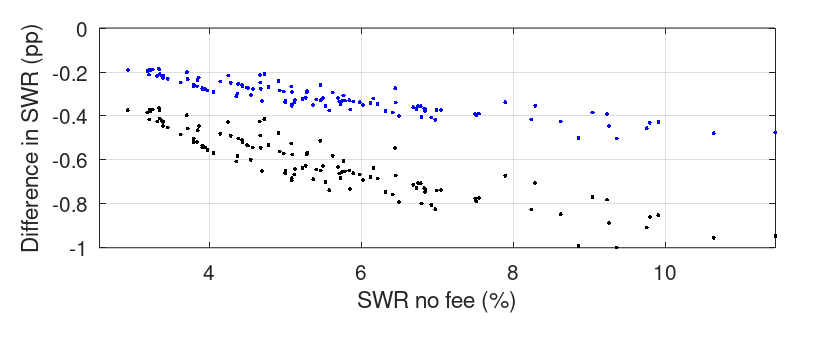

A plot of the difference between the SWR with fee and without fee shows these effects more clearly

For the lowest SWR, the result is similar to that in Kitces work (i.e., multiplying the fee rate by 0.4 gives the effect on SWR), but for the highest values of SWR, the effect on the SWR is closer to the fee rate itself.

Anyway, whatever the precise numerical effect, to a certain extent, minimising fees will lead to more useable income in retirement.

1 -

I have seen 3-3.5% been quoted for UK , and 4% more applicable to the USA , however for ourselves I was thinking of using 4% while still younger and active , then when get state pension (10 years later) reduce that to 2% sayLinton said:

The problem is that if you are very highly invested in equities which crash by say 40% at the start of year 2 you will be withdrawing perhaps 6% of the then pot size. History shows that a 4% initial figure may not be sustainable. A 2-year buffer may help to some extent but has its own problems which have been discussed many times. There have been falls which have lasted longer than 2 years (eg the 2000 .com crash).Mick70 said:Morning

must admit due to time I haven't read the fuill thread but I was going to use the 4% rule for my wife retiring next year .

so say if pot is £350k then in year 1 drawdown £14k and increase accordingly each year with inflation, she will have about 2 years worth of her portfolio as cash , which can be used if the markets ever fell badly

If you are not highly invested in equities your pot may not be able to match long term inflation.

This is why a figure of 3-3.5% is usually quoted here.0 -

This is typical for UK early retirees......for many, it's 5% (or more) front loading up to SP, followed by a corresponding reduction after SP kicks in, though obviously you have to work your own figures in depending on pot size and retirement age etc.......Mick70 said:

I have seen 3-3.5% been quoted for UK , and 4% more applicable to the USA , however for ourselves I was thinking of using 4% while still younger and active , then when get state pension (10 years later) reduce that to 2% sayLinton said:

The problem is that if you are very highly invested in equities which crash by say 40% at the start of year 2 you will be withdrawing perhaps 6% of the then pot size. History shows that a 4% initial figure may not be sustainable. A 2-year buffer may help to some extent but has its own problems which have been discussed many times. There have been falls which have lasted longer than 2 years (eg the 2000 .com crash).Mick70 said:Morning

must admit due to time I haven't read the fuill thread but I was going to use the 4% rule for my wife retiring next year .

so say if pot is £350k then in year 1 drawdown £14k and increase accordingly each year with inflation, she will have about 2 years worth of her portfolio as cash , which can be used if the markets ever fell badly

If you are not highly invested in equities your pot may not be able to match long term inflation.

This is why a figure of 3-3.5% is usually quoted here.0 -

Yes but the comparisons made so far assume that the diy investment portfolio will be the same or equivalent to an IFA's. If you are confident in choosing your portfolio, then fine. However if you get it wrong the costs to future income could be far higher.Bostonerimus1 said:

Yes you go into drawdown to get money to pay of things. I'm just saying that any cost the amortizes to reduce your SWR so significantly should be look at. When you think that your annual IFA etc fees could be 10% or 20% of your retirement expenditures then controlling them is very important when you come to do a budget.westv said:

If you going to look at it that way, then you should always take less in the first few years as there will always be deductions of some sort or another.Bostonerimus1 said:

But at the start of drawdown a 0.5% fee reduces your spending by 0.5%. So the impact of fees are highest right where sequence of returns risk is highest, of course this assumes fees stay the same. I think it's best to go into retirement with your fixed costs reduced as much as possible, so no mortgage and IFA and fund fees as low as possible. I you can DIY that's an obvious way to give a 16% (0.5%/3.0%) boost to your income.westv said:

I thought it was closer to 0.5% which equates to 0.25% reduction over the length of drawdown.Ibrahim5 said:The average IFA fee is 0.8% so 4% without an IFA is equivalent to 3.2% with an adviser's fingers in your pot. That's assuming an adviser is as good at managing the investments, which in my experience they are nowhere near.0 -

It has to be the case that IFAs as a body will on average, before fees, get something close to the market average returns. AFAIK, there are no data on the effectiveness of IFAs in purely investing terms (but perhaps others do have that info). In other words, the comparisons are good enough.Linton said:

Yes but the comparisons made so far assume that the diy investment portfolio will be the same or equivalent to an IFA's. If you are confident in choosing your portfolio, then fine. However if you get it wrong the costs to future income could be far higher.Bostonerimus1 said:

Yes you go into drawdown to get money to pay of things. I'm just saying that any cost the amortizes to reduce your SWR so significantly should be look at. When you think that your annual IFA etc fees could be 10% or 20% of your retirement expenditures then controlling them is very important when you come to do a budget.westv said:

If you going to look at it that way, then you should always take less in the first few years as there will always be deductions of some sort or another.Bostonerimus1 said:

But at the start of drawdown a 0.5% fee reduces your spending by 0.5%. So the impact of fees are highest right where sequence of returns risk is highest, of course this assumes fees stay the same. I think it's best to go into retirement with your fixed costs reduced as much as possible, so no mortgage and IFA and fund fees as low as possible. I you can DIY that's an obvious way to give a 16% (0.5%/3.0%) boost to your income.westv said:

I thought it was closer to 0.5% which equates to 0.25% reduction over the length of drawdown.Ibrahim5 said:The average IFA fee is 0.8% so 4% without an IFA is equivalent to 3.2% with an adviser's fingers in your pot. That's assuming an adviser is as good at managing the investments, which in my experience they are nowhere near.

In terms of DIY investing, the philosophy on these boards (and bogleheads) is that either holding a single multi-asset fund or holding global equity and global bond (hedged) index funds is likely to be good enough. The first, and most important, decision for the DIY investor is then what should the allocation to equities be (with good enough starting points for further discussion being around 80% in accumulation and 60% in retirement*). Personally, I think the biggest problem for DIY investors is psychological, e.g., when panic sets in during a downturn - there were even threads on the bogleheads forum after the GFC suggesting a 'Plan B' of getting out of equities for those who couldn't stomach seeing their portfolios shrink further). For some, an IFA might provide a useful 'cool head' in such times (otherwise, these boards might be useful!)

*Personally, I think the 'risk' concept (i.e., volatility) is not a useful one in retirement since one aim is to secure core income (e.g., through gilt ladders or annuities).2 -

I'm sure OldScientist won't mind me pointing out that these are all the old arguments between IFA and DIY. My DIY lifetime average annual return in my equity and bond investments is almost 10% with a very simple portfolio and management ie just a bit of rebalancing. My experience is just for one set of market conditions and I cannot judge how much of my return is down to luck but I believe that there is little to be gained in investment returns from an IFA or Wealth Manager for a competent amateur.OldScientist said:

It has to be the case that IFAs as a body will on average, before fees, get something close to the market average returns. AFAIK, there are no data on the effectiveness of IFAs in purely investing terms (but perhaps others do have that info). In other words, the comparisons are good enough.Linton said:

Yes but the comparisons made so far assume that the diy investment portfolio will be the same or equivalent to an IFA's. If you are confident in choosing your portfolio, then fine. However if you get it wrong the costs to future income could be far higher.Bostonerimus1 said:

Yes you go into drawdown to get money to pay of things. I'm just saying that any cost the amortizes to reduce your SWR so significantly should be look at. When you think that your annual IFA etc fees could be 10% or 20% of your retirement expenditures then controlling them is very important when you come to do a budget.westv said:

If you going to look at it that way, then you should always take less in the first few years as there will always be deductions of some sort or another.Bostonerimus1 said:

But at the start of drawdown a 0.5% fee reduces your spending by 0.5%. So the impact of fees are highest right where sequence of returns risk is highest, of course this assumes fees stay the same. I think it's best to go into retirement with your fixed costs reduced as much as possible, so no mortgage and IFA and fund fees as low as possible. I you can DIY that's an obvious way to give a 16% (0.5%/3.0%) boost to your income.westv said:

I thought it was closer to 0.5% which equates to 0.25% reduction over the length of drawdown.Ibrahim5 said:The average IFA fee is 0.8% so 4% without an IFA is equivalent to 3.2% with an adviser's fingers in your pot. That's assuming an adviser is as good at managing the investments, which in my experience they are nowhere near.

In terms of DIY investing, the philosophy on these boards (and bogleheads) is that either holding a single multi-asset fund or holding global equity and global bond (hedged) index funds is likely to be good enough. The first, and most important, decision for the DIY investor is then what should the allocation to equities be (with good enough starting points for further discussion being around 80% in accumulation and 60% in retirement*). Personally, I think the biggest problem for DIY investors is psychological, e.g., when panic sets in during a downturn - there were even threads on the bogleheads forum after the GFC suggesting a 'Plan B' of getting out of equities for those who couldn't stomach seeing their portfolios shrink further). For some, an IFA might provide a useful 'cool head' in such times (otherwise, these boards might be useful!)

*Personally, I think the 'risk' concept (i.e., volatility) is not a useful one in retirement since one aim is to secure core income (e.g., through gilt ladders or annuities).And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

Once I woke up. and stopped using the default funds, I have kept things simple, basically trackers with extra UK to hedge against big currency fluctuations and a couple of more adventurous funds. I took more risks because I have so much in DB funds. I don’t think an IFA would have improved that once their charges are taken into account.Bostonerimus1 said:

I'm sure OldScientist won't mind me pointing out that these are all the old arguments between IFA and DIY. My DIY lifetime average annual return in my equity and bond investments is almost 10% with a very simple portfolio and management ie just a bit of rebalancing. My experience is just for one set of market conditions and I cannot judge how much of my return is down to luck but I believe that there is little to be gained in investment returns from an IFA or Wealth Manager for a competent amateur.OldScientist said:

It has to be the case that IFAs as a body will on average, before fees, get something close to the market average returns. AFAIK, there are no data on the effectiveness of IFAs in purely investing terms (but perhaps others do have that info). In other words, the comparisons are good enough.Linton said:

Yes but the comparisons made so far assume that the diy investment portfolio will be the same or equivalent to an IFA's. If you are confident in choosing your portfolio, then fine. However if you get it wrong the costs to future income could be far higher.Bostonerimus1 said:

Yes you go into drawdown to get money to pay of things. I'm just saying that any cost the amortizes to reduce your SWR so significantly should be look at. When you think that your annual IFA etc fees could be 10% or 20% of your retirement expenditures then controlling them is very important when you come to do a budget.westv said:

If you going to look at it that way, then you should always take less in the first few years as there will always be deductions of some sort or another.Bostonerimus1 said:

But at the start of drawdown a 0.5% fee reduces your spending by 0.5%. So the impact of fees are highest right where sequence of returns risk is highest, of course this assumes fees stay the same. I think it's best to go into retirement with your fixed costs reduced as much as possible, so no mortgage and IFA and fund fees as low as possible. I you can DIY that's an obvious way to give a 16% (0.5%/3.0%) boost to your income.westv said:

I thought it was closer to 0.5% which equates to 0.25% reduction over the length of drawdown.Ibrahim5 said:The average IFA fee is 0.8% so 4% without an IFA is equivalent to 3.2% with an adviser's fingers in your pot. That's assuming an adviser is as good at managing the investments, which in my experience they are nowhere near.

In terms of DIY investing, the philosophy on these boards (and bogleheads) is that either holding a single multi-asset fund or holding global equity and global bond (hedged) index funds is likely to be good enough. The first, and most important, decision for the DIY investor is then what should the allocation to equities be (with good enough starting points for further discussion being around 80% in accumulation and 60% in retirement*). Personally, I think the biggest problem for DIY investors is psychological, e.g., when panic sets in during a downturn - there were even threads on the bogleheads forum after the GFC suggesting a 'Plan B' of getting out of equities for those who couldn't stomach seeing their portfolios shrink further). For some, an IFA might provide a useful 'cool head' in such times (otherwise, these boards might be useful!)

*Personally, I think the 'risk' concept (i.e., volatility) is not a useful one in retirement since one aim is to secure core income (e.g., through gilt ladders or annuities).

However, I use the James Shack videos on YouTube. If I had more than £1m and IHT was something that worried me, and/or I had filled my ISA and premium bond allowances I would definitely look for someone like him.0 -

I think that James Shack has talked about "factor investing" as a way to marginally improve your SWR / reduce your fail rate on your withdrawals, but I'm not totally convinced about this because I suspect that the scenarios that are helped by having a bigger share in small cap value type stocks, are a very long time ago and it's not clear if that effect will be valid in future. Either way I don't think it makes a big difference unless you have millions.Moonwolf said:

Once I woke up. and stopped using the default funds, I have kept things simple, basically trackers with extra UK to hedge against big currency fluctuations and a couple of more adventurous funds. I took more risks because I have so much in DB funds. I don’t think an IFA would have improved that once their charges are taken into account.Bostonerimus1 said:

I'm sure OldScientist won't mind me pointing out that these are all the old arguments between IFA and DIY. My DIY lifetime average annual return in my equity and bond investments is almost 10% with a very simple portfolio and management ie just a bit of rebalancing. My experience is just for one set of market conditions and I cannot judge how much of my return is down to luck but I believe that there is little to be gained in investment returns from an IFA or Wealth Manager for a competent amateur.OldScientist said:

It has to be the case that IFAs as a body will on average, before fees, get something close to the market average returns. AFAIK, there are no data on the effectiveness of IFAs in purely investing terms (but perhaps others do have that info). In other words, the comparisons are good enough.Linton said:

Yes but the comparisons made so far assume that the diy investment portfolio will be the same or equivalent to an IFA's. If you are confident in choosing your portfolio, then fine. However if you get it wrong the costs to future income could be far higher.Bostonerimus1 said:

Yes you go into drawdown to get money to pay of things. I'm just saying that any cost the amortizes to reduce your SWR so significantly should be look at. When you think that your annual IFA etc fees could be 10% or 20% of your retirement expenditures then controlling them is very important when you come to do a budget.westv said:

If you going to look at it that way, then you should always take less in the first few years as there will always be deductions of some sort or another.Bostonerimus1 said:

But at the start of drawdown a 0.5% fee reduces your spending by 0.5%. So the impact of fees are highest right where sequence of returns risk is highest, of course this assumes fees stay the same. I think it's best to go into retirement with your fixed costs reduced as much as possible, so no mortgage and IFA and fund fees as low as possible. I you can DIY that's an obvious way to give a 16% (0.5%/3.0%) boost to your income.westv said:

I thought it was closer to 0.5% which equates to 0.25% reduction over the length of drawdown.Ibrahim5 said:The average IFA fee is 0.8% so 4% without an IFA is equivalent to 3.2% with an adviser's fingers in your pot. That's assuming an adviser is as good at managing the investments, which in my experience they are nowhere near.

In terms of DIY investing, the philosophy on these boards (and bogleheads) is that either holding a single multi-asset fund or holding global equity and global bond (hedged) index funds is likely to be good enough. The first, and most important, decision for the DIY investor is then what should the allocation to equities be (with good enough starting points for further discussion being around 80% in accumulation and 60% in retirement*). Personally, I think the biggest problem for DIY investors is psychological, e.g., when panic sets in during a downturn - there were even threads on the bogleheads forum after the GFC suggesting a 'Plan B' of getting out of equities for those who couldn't stomach seeing their portfolios shrink further). For some, an IFA might provide a useful 'cool head' in such times (otherwise, these boards might be useful!)

*Personally, I think the 'risk' concept (i.e., volatility) is not a useful one in retirement since one aim is to secure core income (e.g., through gilt ladders or annuities).

However, I use the James Shack videos on YouTube. If I had more than £1m and IHT was something that worried me, and/or I had filled my ISA and premium bond allowances I would definitely look for someone like him.

Also - the funds that are often quoted for this don't seem to be easily available to DIY investors.0 -

That assumes that the primary objective of a retirement portfolio where the outcome really matters is to maximise long term return. I would contend that a better objective is suffficient return at appropriate risk. In particular the current and future risk of losing sleep and possibly panicking in a market fall. The levels of sufficient return and appropriate risk are both highly dependent on a good understanding of the customer.OldScientist said:

It has to be the case that IFAs as a body will on average, before fees, get something close to the market average returns. AFAIK, there are no data on the effectiveness of IFAs in purely investing terms (but perhaps others do have that info). In other words, the comparisons are good enough.Linton said:

Yes but the comparisons made so far assume that the diy investment portfolio will be the same or equivalent to an IFA's. If you are confident in choosing your portfolio, then fine. However if you get it wrong the costs to future income could be far higher.Bostonerimus1 said:

Yes you go into drawdown to get money to pay of things. I'm just saying that any cost the amortizes to reduce your SWR so significantly should be look at. When you think that your annual IFA etc fees could be 10% or 20% of your retirement expenditures then controlling them is very important when you come to do a budget.westv said:

If you going to look at it that way, then you should always take less in the first few years as there will always be deductions of some sort or another.Bostonerimus1 said:

But at the start of drawdown a 0.5% fee reduces your spending by 0.5%. So the impact of fees are highest right where sequence of returns risk is highest, of course this assumes fees stay the same. I think it's best to go into retirement with your fixed costs reduced as much as possible, so no mortgage and IFA and fund fees as low as possible. I you can DIY that's an obvious way to give a 16% (0.5%/3.0%) boost to your income.westv said:

I thought it was closer to 0.5% which equates to 0.25% reduction over the length of drawdown.Ibrahim5 said:The average IFA fee is 0.8% so 4% without an IFA is equivalent to 3.2% with an adviser's fingers in your pot. That's assuming an adviser is as good at managing the investments, which in my experience they are nowhere near.

In terms of DIY investing, the philosophy on these boards (and bogleheads) is that either holding a single multi-asset fund or holding global equity and global bond (hedged) index funds is likely to be good enough. The first, and most important, decision for the DIY investor is then what should the allocation to equities be (with good enough starting points for further discussion being around 80% in accumulation and 60% in retirement*). Personally, I think the biggest problem for DIY investors is psychological, e.g., when panic sets in during a downturn - there were even threads on the bogleheads forum after the GFC suggesting a 'Plan B' of getting out of equities for those who couldn't stomach seeing their portfolios shrink further). For some, an IFA might provide a useful 'cool head' in such times (otherwise, these boards might be useful!)

*Personally, I think the 'risk' concept (i.e., volatility) is not a useful one in retirement since one aim is to secure core income (e.g., through gilt ladders or annuities).

An SWR does not help much since it is based on just avoiding running out of money at the worst time.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards