We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

Income and Dividend taxes : Update

Comments

-

@probate_slave thank you, you have been so incredibly helpful. If I can I indulge you for one more (hopefully final) question please.

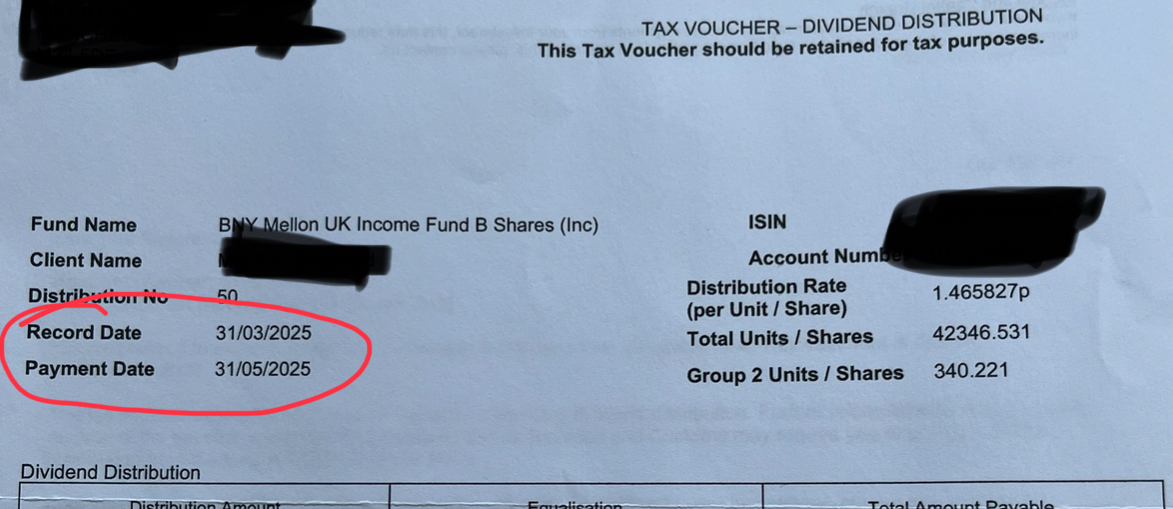

Does the tax fall due relative to the payment date or the record date

i.e. does the following apply to tax year 24/25 (record date) or 25/26 (payment date). I am reading conflicting advice online. Many thanks0

Many thanks0 -

I believe it's the payment date that's relevant for income tax. The record date will be within a couple of days of the ex-dividend date.

1 -

One more

")

How do we treat a pension payment recieved after death I.e. paid in arrears

Is this considered as income to the estate or do we include it as part of the estate value at time of death?0 -

Pension arrears and lump sum benefits are normally assets of the deceased estate, liable both for IHT and income tax on the deceased.

In some rare cases (eg alternatively secured pension funds) they are treated differently, as discussed in the IHT400 notes to schedule IHT409.

1 -

Just when I thought it was all sorted...

Have received an unexpected Dividend Cheque from a Stocks&Shares ISA.The dividend period is prior to death but the payment date is after death/grant of probate and after the ISA was closed/cashed-in.

What is the correct treatment of the Dividend, does it retain its tax-free ISA status or is it now subject to normal Dividend Taxation as part of the estate?

thanks.0 -

If there was any IHT to pay then the dividend should have been part of the estate to calculate that I am afraid.

But, if not, in terms of tax, it should be ok. I think the ISA retains its tax free status for 3 years (if not inherited by spouse when it will be forever as an extra one off entitlement)

So no dividend tax I think.0 -

There is no IHT to pay.SadCodeMan said:If there was any IHT to pay then the dividend should have been part of the estate to calculate that I am afraid.

But, if not, in terms of tax, it should be ok. I think the ISA retains its tax free status for 3 years (if not inherited by spouse when it will be forever as an extra one off entitlement)

So no dividend tax I think.

From https://www.gov.uk/individual-savings-accounts/if-you-die

"Your ISA will end when either:- your executor closes it

- the administration of your estate is completed

Otherwise, your ISA provider will close your ISA 3 years and 1 day after you die."

Hence the question re ISA status because it was closed after the dividend was declared but prior to the dividend being paid.0 -

Ah. Sorry. I sligtly misread that.

I am fairly sure the payment of the dividend will still be part of the ISA. Indeed, I think the ISA provider should have known about the outstanding dividend and possibly shouldn't have fully shut the wrapper until it was settled.

0 -

I did search to see if I could find a definative answer on any HMRC page but no absolutely specific one jumped out.

The closest I could find was from a much more generic page on dividends:

https://www.gov.uk/tax-on-dividends

But this does say:

You do not pay tax on dividends from shares in an ISA.

Your case above absolutely is a dividend from a share in an ISA because the point the estate was legally entitled to the payment (ex date) the ISA was open and the entitlement was directly as a result of the ownership of that share held in that ISA.

0 -

Actually, I take that all back. I think I am wrong. Sorry...

I just found this:

https://assets.publishing.service.gov.uk/media/5a81ed77e5274a2e87dc039a/ISA_guidance_notes_investor_dies_extract.pdf

Unfortnately there is a section which says:

12.10 When an investor dies on or after 6 April 2018 the savings of a deceased investor can continue to benefit from the tax advantages of an ISA during the administration period of the estate. Any interest, dividends or gains in respect of investments in a continuing account of a deceased investor that arise (which in general terms means ‘paid’) after the date of death to the date of closure of the ISA are exempt from tax (see paragraph 3.23 – 3.28).

That does sound like any dividends paid after the closure are maybe not considered exempt.

I hope there is maybe enough tax allowance in the estate to cover the payment?

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards