We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

I know they say don’t try to time the market but…..

Comments

-

Thanks everyone! I think I am even more confused on the best approach to take now and therefore maybe I should reconsider a fund like HSBC Global Strategy or Vanguard Lifestrategy…0

-

There will always be market dips when you’ll be able to buy equities cheaper than the day or week or even month before…but not necessarily cheaper than you can buy today. In a month, the price of your HSBC fund might fall 3% but during that month it may have gone up 7%. So will you buy when it falls 3% or will you hold on in case it drops a little more…you could end up doing nothing and be paralysed by looking for that “bottom”.

I’m more of a time in the market man, so I’d be going in with at least 50%. Then if markets climb you’ve made gains…if they fall you can average down. The main thing is to have confidence in the fund you’ve chosen and be happy to buy even it falls…after all, if you think it’s a good buy today surely it’s a better buy at a lower price. Then invest up to the % you want e.g. 75% of the money you have available today. Fwiw, that HSBC fund is what I have the largest % in, it’s a top fund…1 -

Thanks, what you’ve said makes so much sense and is originally what I was thinking. As a new investor it’s so daunting! Do you have any suggestions for the “safer” element? I’ve only really researched finding my equities fund at this point, so bonds, gold etc are next on my list to research!thunderroad88 said:Fwiw, that HSBC fund is what I have the largest % in, it’s a top fund…0 -

The fact you are worried about timing the market when you know the best advice is time in the market is paramount for compounding shows you are not yet ready for equities.

I've been investing for over 40 years, max money into ISA (and older versions) on April 6 the vast majority of years and weathered many downturns. The thing is to only invest what you don't need now and forget about it. Many studies have shown that not being invested for the best few days of the year can halve your gain for that year, which when compounded leads to significant underperformance. If the thought of dropping 40% in a few days, and needing perhaps a year or two to get back into profit is too much, then go for a more conservative capital preservation fund, you may beat inflation and lag a global tracker by quite a bit, but may sleep well at night, which might be more important.2 -

Prioritising growth only makes sense if you have the stomach for big losses. Yes, bond prices fell from a great height recently. They are now reasonably priced by historical standards. They would nonetheless be wiped out by hyper-inflation, along with cash. Bonds have never been a reliable hedge for equities, but neither has anything else.CompoundQueen25 said:

I am trying to prioritise growth and I am keeping 25% back in cash for now until I’ve got my head round bonds and other defensive investments. I feel I still have a lot to learn on that side. Not sure if this is totally correct, but in the covid crash, didn’t bonds also tank? Are they still as reliable to de-risk as they once were?GeoffTF said:

If you do that the market might wait 6 months and then crash. Why why you think the market will be safer in 6 months time? If you go 100% equities, you could be facing a loss after 10 years and could even be wiped out. If you cannot take that, include a percentage of bonds.CompoundQueen25 said:Perhaps I could take a hybrid approach and 50% lump sum and DCA the rest over 6 months?1 -

I suggest that you buy a packaged fund with an appropriate risk profile. That will have been put together by people who know what they are doing. That does not mean it will necessarily work out well. Nobody knows the future.CompoundQueen25 said:I’m guessing a mix of govt and corporate bonds, maybe an ETF for ease? Maybe some gold? It’s a lot to consider as a new investor!0 -

Both these are actually a series of funds at different risk levels.CompoundQueen25 said:Thanks everyone! I think I am even more confused on the best approach to take now and therefore maybe I should reconsider a fund like HSBC Global Strategy or Vanguard Lifestrategy…

The HSBC funds have a higher US% and in recent years this has meant they have performed a bit better than the VLS funds, which have a highish UK % but currently not so.

1 -

Quite agree - I’ve been investing for 35 years + and trying to second guess the market to any great degree will not bring success. You may win some of the time, but in the long run it will result in an overall loss. You never know what’s around the corner that will affect your investment.talexuser said:The fact you are worried about timing the market when you know the best advice is time in the market is paramount for compounding shows you are not yet ready for equities.

I've been investing for over 40 years, max money into ISA (and older versions) on April 6 the vast majority of years and weathered many downturns. The thing is to only invest what you don't need now and forget about it. Many studies have shown that not being invested for the best few days of the year can halve your gain for that year, which when compounded leads to significant underperformance. If the thought of dropping 40% in a few days, and needing perhaps a year or two to get back into profit is too much, then go for a more conservative capital preservation fund, you may beat inflation and lag a global tracker by quite a bit, but may sleep well at night, which might be more important.

2 -

Unless your job is a fairly high position in the stocks and shares section of a bank, you cannot time the market. There are thousands of people along with their plans and games around the world knowing what's likely to happen more than you, weeks ahead of you. So don't kid yourself you can. As in most things, the simple answer is the most likely and it's time IN the market.

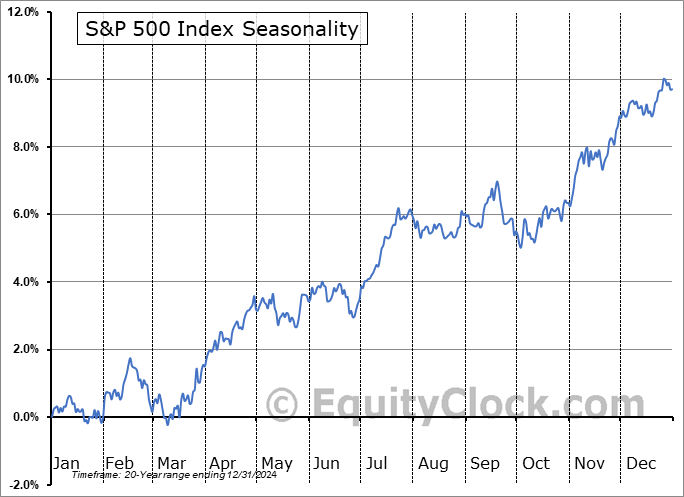

The only thing I have 'noticed' after a few years watching my diversified funds go up and down is that everything seems to go downhill in January and takes a few months to come back, and then spends the rest of the year going higher than the last. This is also just speculation and a trend that could end or has ended any time. As I have no idea when things could go up or down on both sides of that scenario, I don't bother doing anything, even with a vague 'hunch' I could be.1 -

Might be worth a look at the S&P500 seasonality chart. Not a guarantee, just a guide.

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards