We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

UPFLS versus Drawdown

Comments

-

Multiple people in this thread talk about leaving funds in their pension, in order to be able to use more of the tax free cash limit. This actually makes no sense at all. You do just as well taking it out early, investing it in an ISA in the same way as the pension, and letting it grow outside. Say you had £160k in the pension and your preferred investment mix doubled in value over the next 10 years. If you leave it untouched for those ten years, then you can indeed take £80k rather than £40k tax free. But if you had taken the £40k and invested it in the same way in you and your partner's ISAs then you'd have exactly the same £80k. All you've achieved is increasing your risk of being over the TFLS limit when you do take it - unless you think it's likely that there will be a significant increase in the limit.2

-

It's not the same if you expect to die before you're 75. Or before the IHT changes come into play in a couple of years.Triumph13 said:Multiple people in this thread talk about leaving funds in their pension, in order to be able to use more of the tax free cash limit. This actually makes no sense at all. You do just as well taking it out early, investing it in an ISA in the same way as the pension, and letting it grow outside. Say you had £160k in the pension and your preferred investment mix doubled in value over the next 10 years. If you leave it untouched for those ten years, then you can indeed take £80k rather than £40k tax free. But if you had taken the £40k and invested it in the same way in you and your partner's ISAs then you'd have exactly the same £80k. All you've achieved is increasing your risk of being over the TFLS limit when you do take it - unless you think it's likely that there will be a significant increase in the limit.

(from you beneficiary's point of view, that is)2 -

That speculation lead to people cashing in pensions before. I’m sure it will again, or gets leaked that’s the direction. Wouldn’t be surprising at some point, after all a stopped clock is right twice a day.Juno_Moneta said:A timely, and relevant to this thread, article …

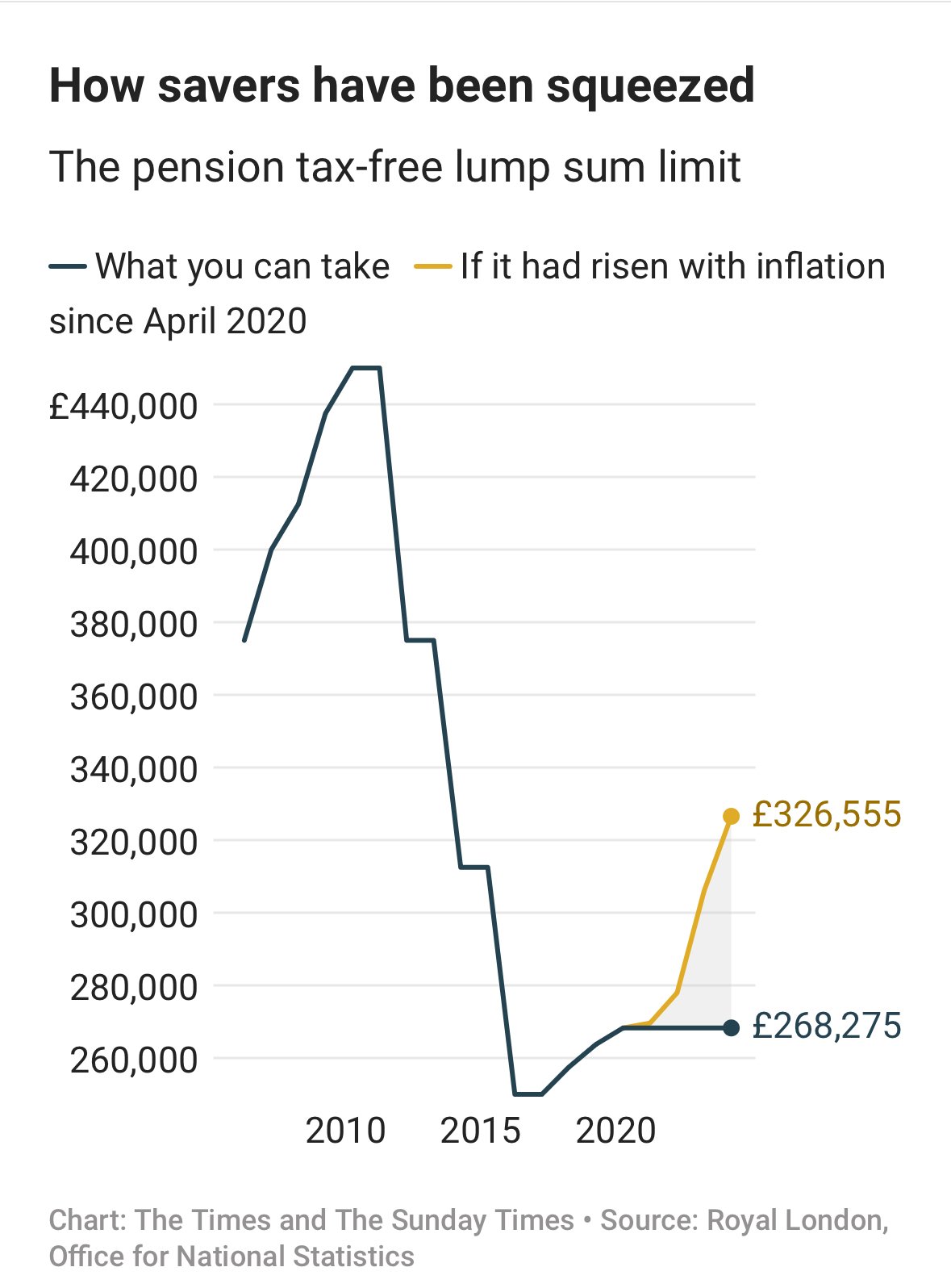

https://www.thetimes.com/business-money/money/article/stick-or-twist-the-pension-savers-tax-free-lump-sum-dilemma-dl8nxs5rq 2

2 -

There are those of us who can and do have the means to maximum fund ISAs each year without ever considering accessing pension pots to do so.Triumph13 said:Multiple people in this thread talk about leaving funds in their pension, in order to be able to use more of the tax free cash limit. This actually makes no sense at all. You do just as well taking it out early, investing it in an ISA in the same way as the pension, and letting it grow outside. Say you had £160k in the pension and your preferred investment mix doubled in value over the next 10 years. If you leave it untouched for those ten years, then you can indeed take £80k rather than £40k tax free. But if you had taken the £40k and invested it in the same way in you and your partner's ISAs then you'd have exactly the same £80k. All you've achieved is increasing your risk of being over the TFLS limit when you do take it - unless you think it's likely that there will be a significant increase in the limit.

We seek to increase our overall wealth via both tax free accrual opportunities.2 -

I agree but it's fair to say it's probably a minority of people that are in this situation. When people read these posts it's normal to assume the most common context which is as Triumph13 stated. It constantly confuses me when people state they are doing things that seem counter intuitive to the the most typical case, without explaining why their specific circumstances make it beneficial. My conclusion to the original question is that UFPSL is simply a specific case of drawdown (ignoring IHT)There are those of us who can and do have the means to maximum fund ISAs each year without ever considering accessing pension pots to do so.

We seek to increase our overall wealth via both tax free accrual opportunities.2 -

Your correct but this is a very specific point. The general point made by Triumph13 is an important clarification in order to fully understand funds don't need to be left in the pot to maximise the use of the tax free limit in most circumstances, which I feel the majority of posts suggest.MeteredOut said:

It's not the same if you expect to die before you're 75. Or before the IHT changes come into play in a couple of years.

(from you beneficiary's point of view, that is)1 -

Thanks. This is what I now believe and would rather it's explained as such rather than something different.squirrelpie said:UFPLS is just the limit case of FAD where you always take all the crystallised cash, both tax free and taxed. So there is nothing you can do with UFPLS that you can't do with a particular style of FAD withdrawals. It is convenient to have a name for that special case, perhaps.0 -

Hi,

I disagree quite strongly with this. The clue is in the name "pension". Once pensions started being used for anything other than providing a retirement income then they were always going to be a target for taxation to address that behaviour. What is surprising is the length of time it took for the government to take action. I don't see how the change affects confidence in pensions since it has no effect on anyone's retirement income.MetaPhysical said:Yes. Pensions pots will be subject to IHT. This is a fundamental change that affects the savings of people who in good faith contributed to pensions with an eye to their IHT exempt status, following the rules. A rule change of this magnitude is a total sea change. At the very least, if a change like this is brought in then it should apply to future payments/growth from the moment the legislation is passed and not existing pension accrued. Rule changes like this undermine the public's confidence in pensions which is already rock bottom.

The only argument that could be deployed in support of not applying inheritance tax would be something around pensions representing a form of life insurance in the event of early death - e.g. you could make an argument that inheritance tax should not be applied to the inheritance of pensions by directly descended / adopted children under the age of 18. The government chose not to see it that way though.The same goes if there is a raid on the 25% TFC or the 268k limit. People have saved money, according to the rules - money they could have placed elsewhere. The government cannot just pull the rug from under people without causing serious consequences.This I do agree with. I doubt that any government will bother to tamper with this, it will be simply left to inflation to render it fiscally irrelevant.

4 -

Re-visited this thread with interest following my Pensionwise call. My core income is secured at £28k PA and I will have a £150k DC pot to access (maybe over 5-6 years) and considering UPFLS, drawdown and fixed term annuities. I think I'll see what a couple of financial advisors can conjure up...that doesn't involve investing in overseas properties.

I hadn't really considered UPFLS.0 -

my plan, according to current rules but with an eye to the expected IHT changes, is to UFPLS with the taxable income part up to the top of the 20% band but this is more than we need (can afford) so the excess will go into a S&S ISA in similar investmentsTriumph13 said:Multiple people in this thread talk about leaving funds in their pension, in order to be able to use more of the tax free cash limit. This actually makes no sense at all. You do just as well taking it out early, investing it in an ISA in the same way as the pension, and letting it grow outside. Say you had £160k in the pension and your preferred investment mix doubled in value over the next 10 years. If you leave it untouched for those ten years, then you can indeed take £80k rather than £40k tax free. But if you had taken the £40k and invested it in the same way in you and your partner's ISAs then you'd have exactly the same £80k. All you've achieved is increasing your risk of being over the TFLS limit when you do take it - unless you think it's likely that there will be a significant increase in the limit.I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards