We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

UPFLS versus Drawdown

Comments

-

Thanks for the article. As others have said, you could use drawdown to take the tax free lump sum, invest it in an ISA with the same funds as the pension and the result would be the same. I think there's nothing you can't do with drawdown that you can do with UPFLS. I've learnt a lot about both in this process of understanding.poseidon1 said:

Basically horses for courses , but good that these options exsist ( for now).

0 -

That could make sense.DRS1 said:For some reason I imagine that with FAD people take the tax free cash but leave the taxable bit behind in the pension drawdown account because they don't want to pay any tax or trigger the MPAA.

I thought UFPLS was used by people who have some spare personal allowance and wanted to take taxable income to use up the spare 0% tax band.0 -

I use it because I want to take a regular income from my SIPP. My tax code for this pension is BR. I crystallize once a year and set the monthly withdrawals so the money is exhausted at the end of the year. This seems like the minimum hassle to me with my provider. Others may use it differently: it is after all a flexible product.DRS1 said:For some reason I imagine that with FAD people take the tax free cash but leave the taxable bit behind in the pension drawdown account because they don't want to pay any tax or trigger the MPAA.

2 -

I've got a pot of 700k. I am first going to move a £120k chunk into drawdown because I need 30k of TFC. The other 75% of the amount moved into drawdown (£90k) will then be fully taxable when I take chunks of it. The rest (majority) of my pension I will take UFPLS from.

The big, BIG joker in the pack is Rachel Reeves and whether she fiddles with the TFC maximum amount of 268k - I am not moving into politics by the way. It would scupper my carefully laid out plans for my future income projections totally if she moves the goalposts [again].1 -

Has she moved the pension goalposts before?MetaPhysical said:

The big, BIG joker in the pack is Rachel Reeves and whether she fiddles with the TFC maximum amount of 268k - I am not moving into politics by the way. It would scupper my carefully laid out plans for my future income projections totally if she moves the goalposts [again].1 -

Yes, by including unused DC pots in inheritance tax calculations from 2027.NickPoole said:

Has she moved the pension goalposts before?MetaPhysical said:

The big, BIG joker in the pack is Rachel Reeves and whether she fiddles with the TFC maximum amount of 268k - I am not moving into politics by the way. It would scupper my carefully laid out plans for my future income projections totally if she moves the goalposts [again].

Then again pension rules change on a regular basis, so nothing unusual about that.0 -

Yes. Pensions pots will be subject to IHT. This is a fundamental change that affects the savings of people who in good faith contributed to pensions with an eye to their IHT exempt status, following the rules. A rule change of this magnitude is a total sea change. At the very least, if a change like this is brought in then it should apply to future payments/growth from the moment the legislation is passed and not existing pension accrued. Rule changes like this undermine the public's confidence in pensions which is already rock bottom.

The same goes if there is a raid on the 25% TFC or the 268k limit. People have saved money, according to the rules - money they could have placed elsewhere. The government cannot just pull the rug from under people without causing serious consequences.2 -

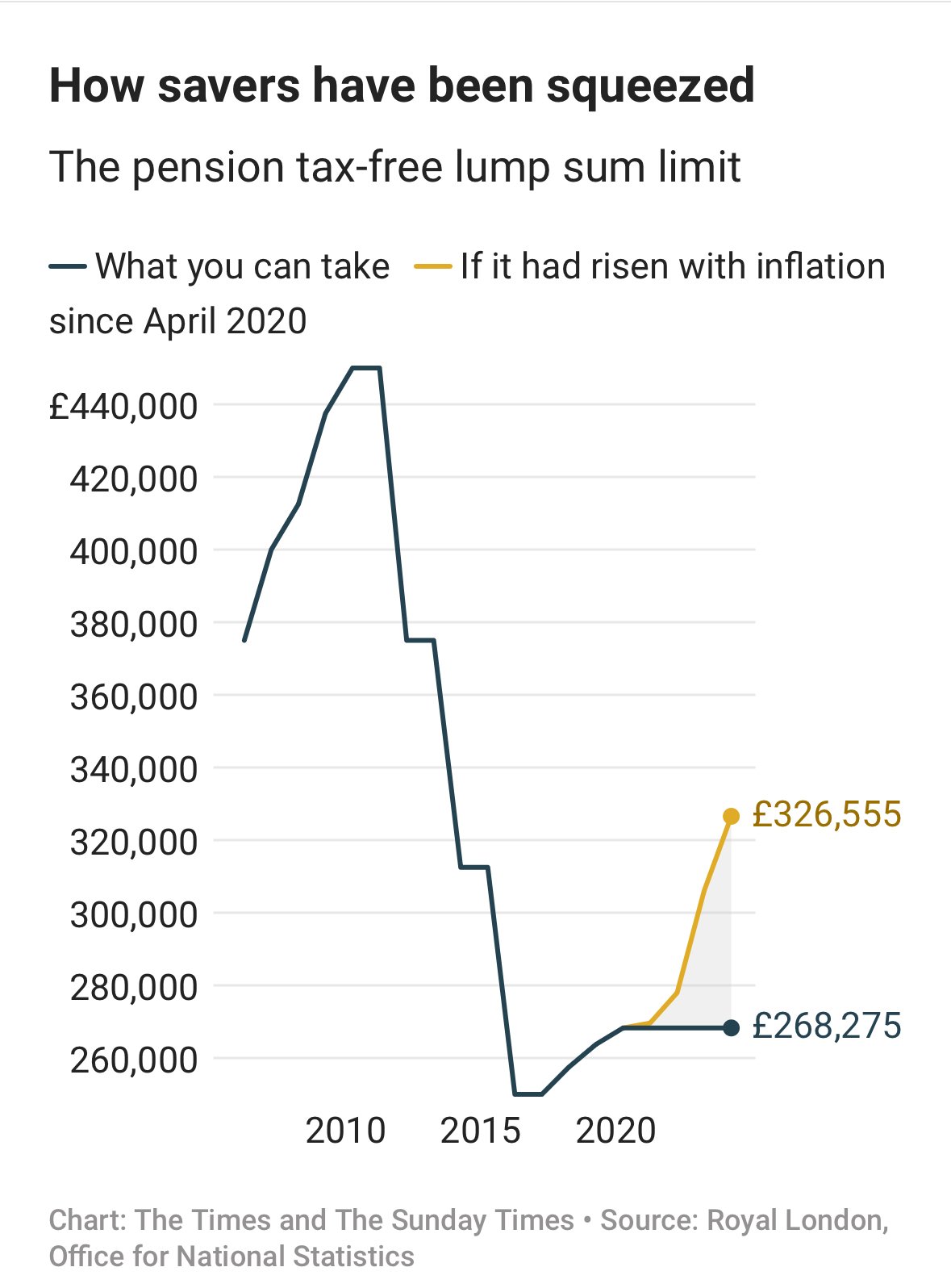

For the second point, the removal or reduction of the 25% will not happen, because as you say it would undermine the idea of pensions too much and be unfair. The Chancellor has many times says she supports the idea of more pension saving, especially for lower income and the self employed. The reduction of the £268K is possible, but unlikely. In real terms inflation has already reduced it by around 25% in recent years.MetaPhysical said:Yes. Pensions pots will be subject to IHT. This is a fundamental change that affects the savings of people who in good faith contributed to pensions with an eye to their IHT exempt status, following the rules. A rule change of this magnitude is a total sea change. At the very least, if a change like this is brought in then it should apply to future payments/growth from the moment the legislation is passed and not existing pension accrued. Rule changes like this undermine the public's confidence in pensions which is already rock bottom.

The same goes if there is a raid on the 25% TFC or the 268k limit. People have saved money, according to the rules - money they could have placed elsewhere. The government cannot just pull the rug from under people without causing serious consequences.

The IHT issue was a loophole, an unforeseen consequence of the pensions reforms of 2015. So although it hurts it is difficult to make a moral case for exempting unused DC pensions ( partly filled with tax relief) from IHT, although some kind of transition period would have been nice.2 -

Agreed.MetaPhysical said:Yes. Pensions pots will be subject to IHT. This is a fundamental change that affects the savings of people who in good faith contributed to pensions with an eye to their IHT exempt status, following the rules. A rule change of this magnitude is a total sea change. At the very least, if a change like this is brought in then it should apply to future payments/growth from the moment the legislation is passed and not existing pension accrued. Rule changes like this undermine the public's confidence in pensions which is already rock bottom.

The same goes if there is a raid on the 25% TFC or the 268k limit. People have saved money, according to the rules - money they could have placed elsewhere. The government cannot just pull the rug from under people without causing serious consequences.

It was normal for a form of grandfathering to be implemented with LTA reductions in previous years.

Surely a similar scheme should be implemented here.

However, the same argument could be made for other recent IHT changes such as the inclusion of agricultural assets and family businesses. That might have some unintended consequences.1 -

A timely, and relevant to this thread, article …

https://www.thetimes.com/business-money/money/article/stick-or-twist-the-pension-savers-tax-free-lump-sum-dilemma-dl8nxs5rq

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards