We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

NatWest - Drydens

username1062

Posts: 19 Forumite

Hi,

I’m awaiting debts to default on advice from members before setting up payment plans. I have a large NatWest loan (affordability complaint turned down from NatWest but currently with FOS).

I’m awaiting debts to default on advice from members before setting up payment plans. I have a large NatWest loan (affordability complaint turned down from NatWest but currently with FOS).

The amount outstanding is just under £23,000.

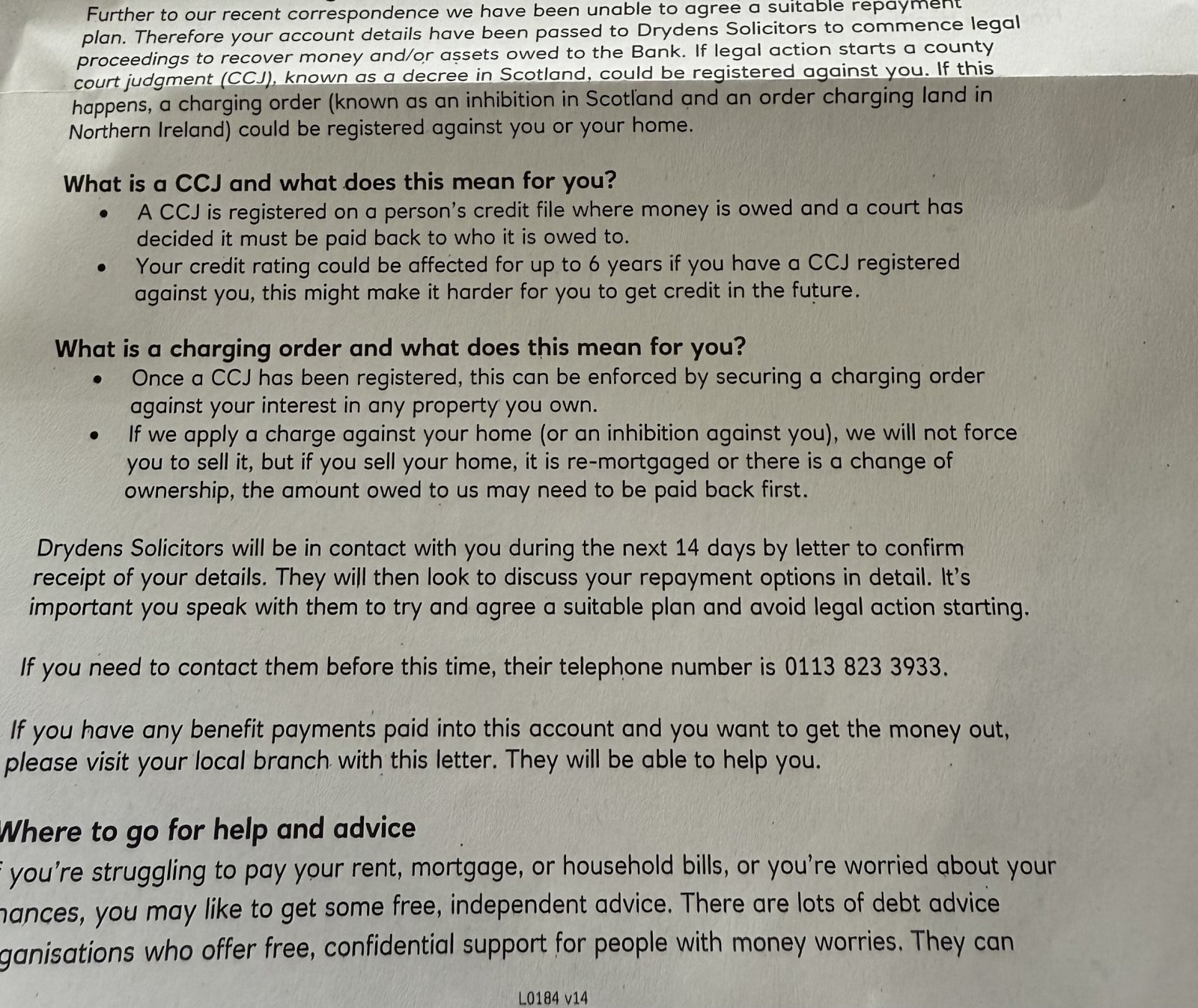

Ive not had a formal default letter from NatWest for the loan yet. However, a letter today (attached)

I really cannot have a CCJ and this has caused me mass panic!

Ive not had a formal default letter from NatWest for the loan yet. However, a letter today (attached)

I really cannot have a CCJ and this has caused me mass panic!

What can I do?

0

Comments

-

Re-read the letter and look at what it says. Look at the "if"s and "could"s that are used repeatedly. That means that nothing is happening yet, simply that NW have passed your file along to a debt collector.

So supposedly within 2 weeks you'll hear from Dryden's. When you do respond to them - by snail mail. Don't ring them or text or email. Tell them that you are looking at your budget and will respond to them within 60 days giving an update on what you consider will be affordable. They may respond after a couple of weeks and agree to 30 days. If you are working with a debt advice agency get them to respond on your behalf. Don't be afraid to insist that everything has to be in writing by post.

Should you never respond to any of their queries they may very well progress to a CCJ. But if you are paying £1 a month or whatever they will likely just tick along with that until they get bored and pass the file back to NW. Who will then send it out to a different debt collector and repeat the whole process.I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅🏅0 -

Neither Drydens or anyone else can commence legal action against you until the default is registered against your debt. The law requires that the relationship has completely broken down.

They shouldn't be chasing further if the case is referred to the Ombudsman, but being charitable, maybe NatWest haven't got round to advising Drydens that the debt case has been appealed to the Ombudsman?

Keep calm, check the relevant credit record agency and act once the default is registered.If you've have not made a mistake, you've made nothing0 -

If Dryden's do instigate legal action, there will be plenty of warning, a letter before action is the first step, it is a document designed to reach an agreement without the need to progress to a claim, and comes with a 30 day return window.

So if you get one of those, it will clearly state what it is, you must respond to avoid a CCJ.

Legal action by an original creditor is rare, but does happen, its likely because you have 23k outstanding to them

And just to clarify the situation regarding default notices and legal action, as until now I was not actually fully aware of this, a lender must issue a default notice before it can take legal action, that is all, just a default notice.It is a written communication from your creditor within which it will clearly state:

"Default notice served under section 87(1) Consumer Credit Act 1974"

Whether the debt actually defaults or not is irrelevant to them taking action.

They can take legal action 14 days from the date the notice was issued.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

Thank you all for your input.

What are the options here? I cannot/do not want a CCJ and apart from paying off in full (which I cannot afford) - what can I do to prevent this?

I am in full panic mode0 -

Stop panicking, if you do receive a letter before action come back for further advice, CCJs don't just appear out of thin air the creditor must go through the full legal process.If you go down to the woods today you better not go alone.0

-

You offer a reasonable payment before it gets to a CCJ.

I'd suggest you double check your SOA against your actual expenditure and maybe share it. You don't want to be promising Dryden's something you can't maintain or to be paying them so much you jeopardise the situation with smaller debts. Nor is living on beans on toast a sustainable option.

From the creditor's point of view, getting a decent sum from you without the cost of court action is usually better than paying court costs and getting less per month.If you've have not made a mistake, you've made nothing0 -

Thanks - is it likely they’ll write to me first ask for a repayment plan or go straight to legal action as the letter insinuates?Is it worth informing them that an affordability complaint is currently with the FOS?0

-

Please read my above post again, it details the legal process, and how to avoid it escalating to a claim.username1062 said:Thanks - is it likely they’ll write to me first ask for a repayment plan or go straight to legal action as the letter insinuates?Is it worth informing them that an affordability complaint is currently with the FOS?

The letter before action is your opportunity to come to an arrangement without the need to progress to court.

If a CCJ is so detrimental to you, then why are you going down the default route at all, why not just make arrangements to pay, and avoid the risk altogether?I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

The steps to a CCJ are:

- formal Default Notice (this is not the same as having a default added to your credit record) - have you received this?

- Letter Before Action (sometimes called other things, but the attachments include a Reply Form)

- N1 form from the court - that starts a claim.

They WILL NOT start a court case before sending a Default notice

They SHOULD NOT start a court case while an Ombudsman complaint is underway. Make sure you tell Drydens that you dispute the debt and it is at FOS

At the moment these are just nasty letters. But as @sourcrates says, why not make an arrangement to pay if you are very worried? The FOS case isnt likely to clear the whole balance is it?

0 -

Thanks ManyWays.ManyWays said:The steps to a CCJ are:

- formal Default Notice (this is not the same as having a default added to your credit record) - have you received this?

- Letter Before Action (sometimes called other things, but the attachments include a Reply Form)

- N1 form from the court - that starts a claim.

They WILL NOT start a court case before sending a Default notice

They SHOULD NOT start a court case while an Ombudsman complaint is underway. Make sure you tell Drydens that you dispute the debt and it is at FOS

At the moment these are just nasty letters. But as @sourcrates says, why not make an arrangement to pay if you are very worried? The FOS case isnt likely to clear the whole balance is it?

I am happy to make an AP but will Drydens likely accept an offer to pay? I’ve calculate an amount which is around £110 per month - I can likely increase this late next year with a payrise.

Ive been successful in a few affordable lending complaints already0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards