We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Creditor still registering default markers / won’t change status of debt post DRO Moratorium

Bernard_Nurse

Posts: 42 Forumite

Good morning

I unfortunately ended up being subject to a DRO in 2023 with the moratorium period ending in December 2024.

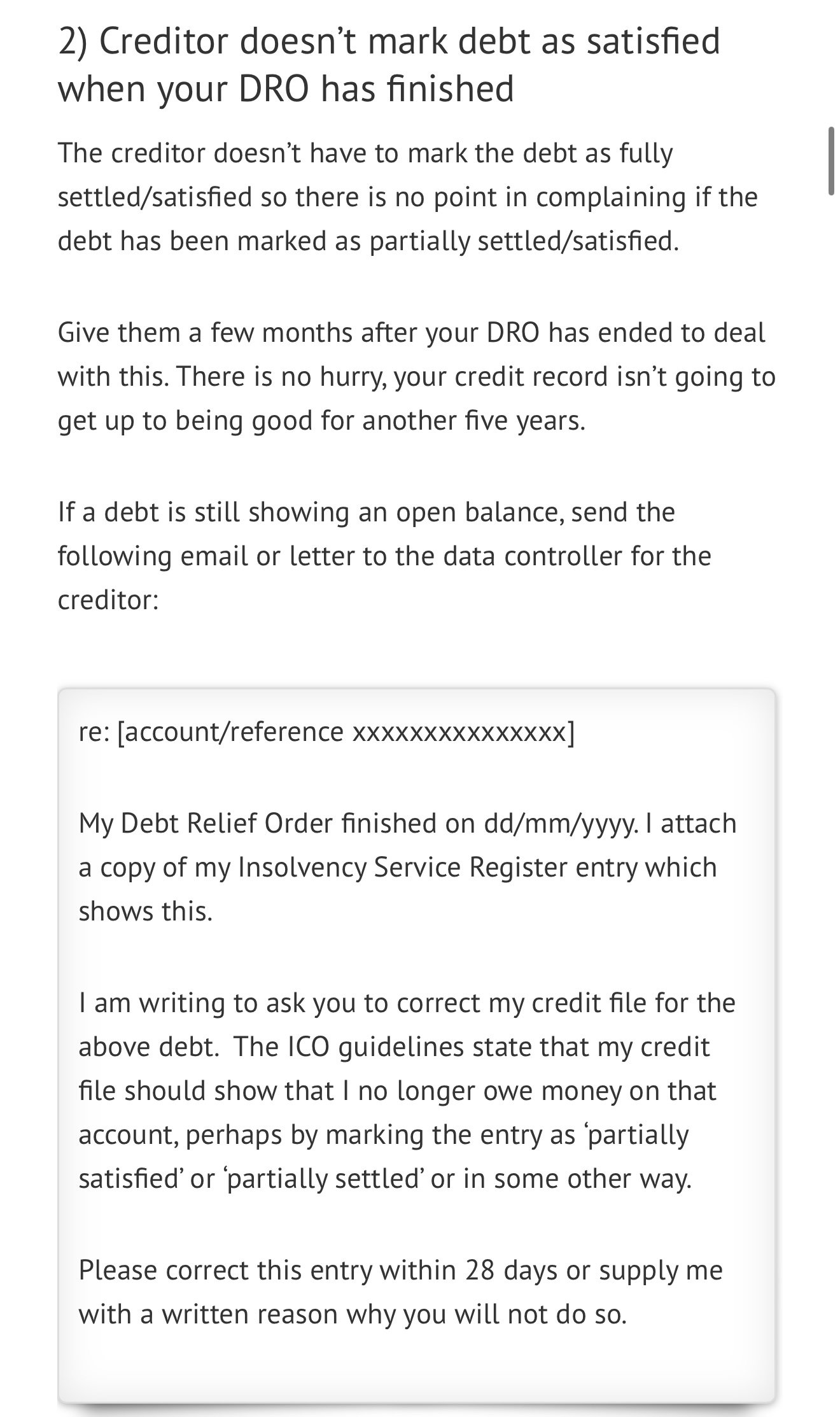

According to both the StepChange and Debt Camel sites, once this has ended a creditor should mark any debts that fell under it as either Satisfied or Partially Settled.

I have been struggling for months with one particular creditor who have only now responded in a meaningful way after a complaint was raised with the Financial Ombudsman.

Their most recent response from them is as follows:

’I can now confirm that your loan with us has been fully discharged in line with your DRO.

Your account has been updated, and I have informed the team to amend your credit file.

However, under credit reporting rules, please note that a default will continue to show on your credit file for six years from the date your DRO was granted’

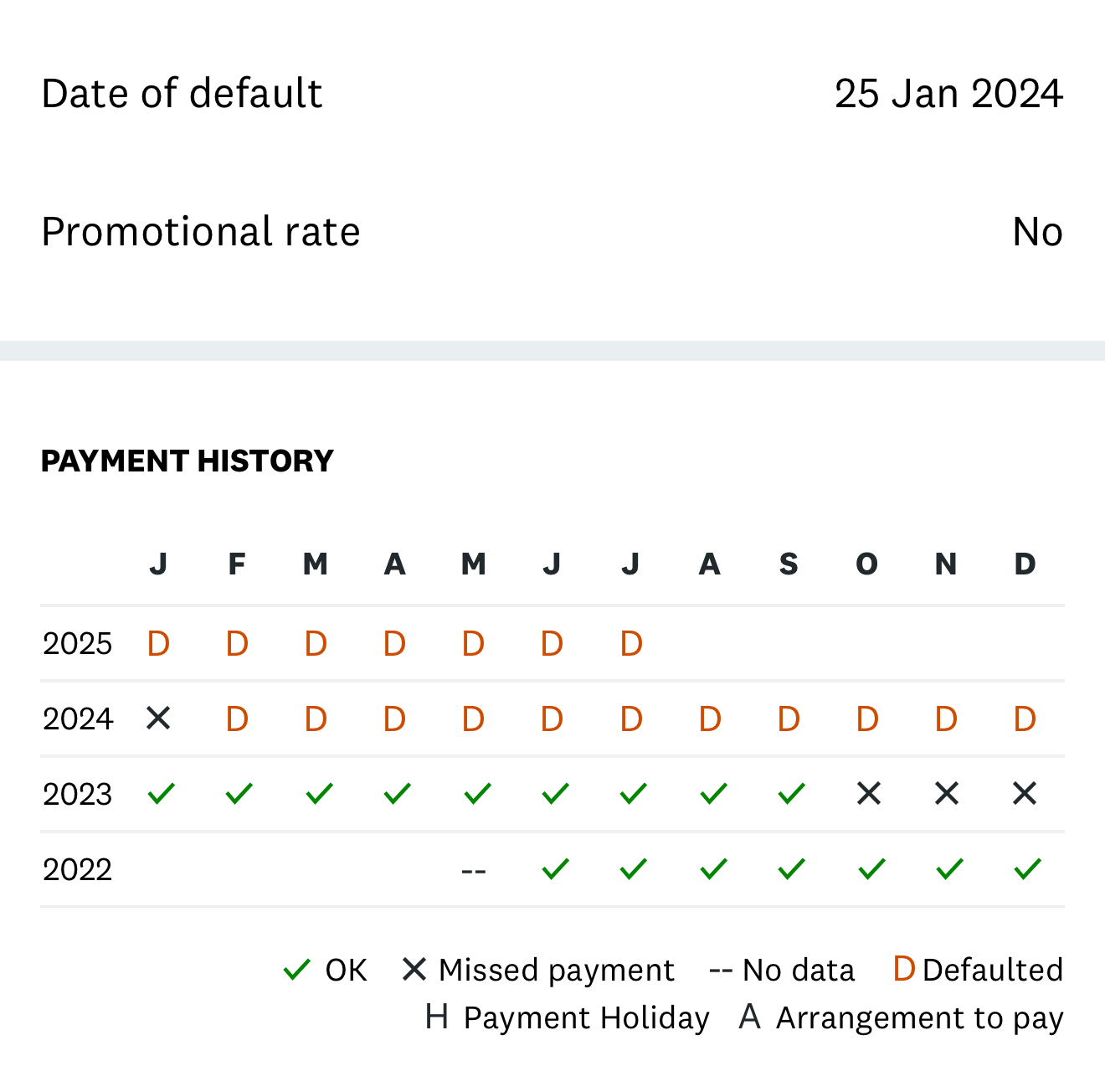

As we speak, the account is showing as Open and with a status of Default. Date of default is showing as nearly two months after the date the DRO was made.

In addition, as per the picture below they’re continuing to register default markers as well.

So, before I go back to them can anyone please advise on who is correct on what the status of the debt should be and if it should indeed be Satisfied or Partially Settled, is there any more other than continuing with the complaint with the Financial Ombudsman I can do to force the issue.

Thank you in advance for any advice.

I unfortunately ended up being subject to a DRO in 2023 with the moratorium period ending in December 2024.

According to both the StepChange and Debt Camel sites, once this has ended a creditor should mark any debts that fell under it as either Satisfied or Partially Settled.

I have been struggling for months with one particular creditor who have only now responded in a meaningful way after a complaint was raised with the Financial Ombudsman.

Their most recent response from them is as follows:

’I can now confirm that your loan with us has been fully discharged in line with your DRO.

Your account has been updated, and I have informed the team to amend your credit file.

However, under credit reporting rules, please note that a default will continue to show on your credit file for six years from the date your DRO was granted’

As we speak, the account is showing as Open and with a status of Default. Date of default is showing as nearly two months after the date the DRO was made.

In addition, as per the picture below they’re continuing to register default markers as well.

So, before I go back to them can anyone please advise on who is correct on what the status of the debt should be and if it should indeed be Satisfied or Partially Settled, is there any more other than continuing with the complaint with the Financial Ombudsman I can do to force the issue.

Thank you in advance for any advice.

0

Comments

-

They are correct in that the default status will show for 6 years regardless of anything else.

Defaults are not removed or replaced by insolvency, no matter what happens, or what you do, nothing removes the default until it expires after 6 years.

Your account should however be marked separately as satisfied or settled, but in the grand scheme of things your credit file won`t improve until the default has gone anyway.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter2 -

Thank you… so where would they report it ‘separately’ as partially settled / satisfied?

0 -

Is there a balance showing?1

-

Usually where the balance is shown on your report, it should show as zero or settled/satisfied, any of those are good enough.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1

-

Balance is showing £0 on one app. On another the account is still showing a balance and as still open.

You can also see on that on they’re still registering default markers as per the pic I posted up previously.0 -

As stated earlier, the default will show for 6 years from the date it was registered, nothing will change that.

Can`t see much of a reason for a complaint here to be fair.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

The following is from the Debt Camel site:sourcrates said:As stated earlier, the default will show for 6 years from the date it was registered, nothing will change that.

Can`t see much of a reason for a complaint here to be fair. As per above, the debt is showing as open, status set to Default and with a positive balance as we speak on at least one CR app.

As per above, the debt is showing as open, status set to Default and with a positive balance as we speak on at least one CR app.

So yes, it would appear there is something to complain about and I’ll update the thread again once the Financial Ombudsman passes judgement in due course.0 -

Its the default that causes issues credit wise, that will not be removed or altered in any way, it shows for 6 years regardless!!

The fact a balance is still showing is an annoyance granted, but she also states that your credit record won`t improve for another 5 years, after the default is removed anyway.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

Well I’ve just checked my credit file again and pleased to be able to report that the status of the debt has been corrected from Default to Satisfied and with a balance of zero and all default markers registered after the end of the moratorium period had ended removed.sourcrates said:Its the default that causes issues credit wise,

that will not be removed or altered in any way, it shows for 6 years regardless!!

The fact a balance is still showing is an annoyance granted, but she also states that your credit record won`t improve for another 5 years, after the default is removed anyway.

The ‘Date of Default’ is the only thing - rightfully - left.

Whether it ultimately makes any difference to my credit score or not is not the key issue (for me at least).

What is, is that the information registered should be accurate (be it good or bad) and when it isn’t, it should be corrected with minimal effort on the part of those who it relates to.

Instead I’ve had to push for months and the lender only dealing with it when after they were made aware a complaint had been initiated with the Financial Ombudsman.An unnecessary waste of time and effort which perhaps would be less essential if so much these days wasn’t potentially impacted by a credit score.0 -

Nothing is impacted by credit score as lenders never even see them.Bernard_Nurse said:

Well I’ve just checked my credit file again and pleased to be able to report that the status of the debt has been corrected from Default to Satisfied and with a balance of zero and all default markers registered after the end of the moratorium period had ended removed.sourcrates said:Its the default that causes issues credit wise,

that will not be removed or altered in any way, it shows for 6 years regardless!!

The fact a balance is still showing is an annoyance granted, but she also states that your credit record won`t improve for another 5 years, after the default is removed anyway.

The ‘Date of Default’ is the only thing - rightfully - left.

Whether it ultimately makes any difference to my credit score or not is not the key issue (for me at least).

What is, is that the information registered should be accurate (be it good or bad) and when it isn’t, it should be corrected with minimal effort on the part of those who it relates to.

Instead I’ve had to push for months and the lender only dealing with it when after they were made aware a complaint had been initiated with the Financial Ombudsman.An unnecessary waste of time and effort which perhaps would be less essential if so much these days wasn’t potentially impacted by a credit score.

A correct reflection of your credit history is important, and glad you got it fixed through persistenceSam Vimes' Boots Theory of Socioeconomic Unfairness:

People are rich because they spend less money. A poor man buys $10 boots that last a season or two before he's walking in wet shoes and has to buy another pair. A rich man buys $50 boots that are made better and give him 10 years of dry feet. The poor man has spent $100 over those 10 years and still has wet feet.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards