We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Accidentally transferred money into junior ISA

Nataliel14

Posts: 9 Forumite

I’ve accidentally transferred an my universal credit payment into my son’s junior isa, which only had £64 in (he’s 10). The bank (nationwide) have said they can’t give it back as it now belongs to the child but it was a genuine mistake. I was trying to move it to my savings account but I clicked the isa instead. Is there anything I can do?

0

Comments

-

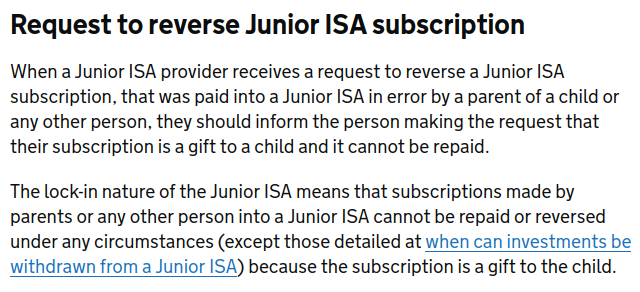

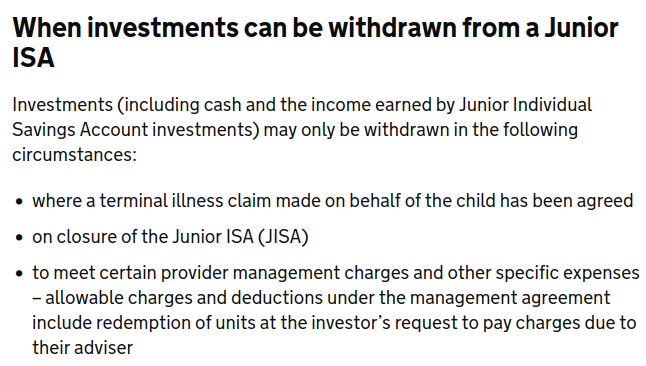

Unfortunately I think they are right and it can't be withdrawn until the child is 18.

Close, void or withdraw investments from a Junior ISA as an ISA manager - GOV.UK0 -

Once in the JISA it can’t be taken out and it is now your son’s money.2

-

Do you have a second bank account? It would be best to set up any accounts belonging to your son as payees on an account that doesn’t receive income, so that a similar mistake can be avoided in future.

While they are correct that money transferred to an account in your son’s name is legally his, it’s unfortunate that it was a JISA as it is that that is stopping the money from being accessed until he is 18. There will be parents who have borrowed from the normal savings of a child and replaced it when funds became available to do so, but the mechanism isn’t there with a JISA. There would only be a way around it if the ISA had been opened in the last 14 days (in which case you would need to ask to cancel the whole JISA under the cooling off period.)

Is there anyone who might have been planning to pay into the JISA that you could ask to pay you instead, so that you aren’t left with no money for a month?0 -

I opened the JISA when he was born, it’s not what I wanted I wanted one of the saving books but they stopped doing them so I ended up with an ISA. That was 10 years ago. I’ve only ever paid £60 in there and it has gained £2 interest over the 10 years. It was a genuine mistake and the first time I’ve made that mistake. Sleep deprivation doesn’t do me any good but I have a new born! I’m going to the bank today to speak to them, I’m not happy with having an overdraft as that’s just going to get me into debt but that was there only solution.Kim_13 said:Do you have a second bank account? It would be best to set up any accounts belonging to your son as payees on an account that doesn’t receive income, so that a similar mistake can be avoided in future.

While they are correct that money transferred to an account in your son’s name is legally his, it’s unfortunate that it was a JISA as it is that that is stopping the money from being accessed until he is 18. There will be parents who have borrowed from the normal savings of a child and replaced it when funds became available to do so, but the mechanism isn’t there with a JISA. There would only be a way around it if the ISA had been opened in the last 14 days (in which case you would need to ask to cancel the whole JISA under the cooling off period.)

Is there anyone who might have been planning to pay into the JISA that you could ask to pay you instead, so that you aren’t left with no money for a month?0 -

I'd also ensure you delete that payee to prevent it happening againRemember the saying: if it looks too good to be true it almost certainly is.0

-

I can’t remove the JISA from my account, it’s linked. I’ve got to go to the bank this morning so I’ll speak to them. I’ve never made this mistake before I’m fuming with myself.jimjames said:I'd also ensure you delete that payee to prevent it happening again0 -

In light of this I would consider opening up a current account with someone other than Nationwide (it’s perfectly acceptable and in fact best practice to retain two or more current accounts with different banks, in case of interrupted service from the first) and get DWP/employer/anyone else to pay into that account, so that you have to actively move money to Nationwide to fund your son’s JISA and can’t make an accidental subscription again.Nataliel14 said:

I can’t remove the JISA from my account, it’s linked. I’ve got to go to the bank this morning so I’ll speak to them. I’ve never made this mistake before I’m fuming with myself.jimjames said:I'd also ensure you delete that payee to prevent it happening again

While Nationwide’s hands are tied by the JISA rules, they haven’t dealt with you well on the basis that:

a) Passbooks weren’t actually withdrawn until February this year, so they could have opened the type of account you wanted. Even if there were no child accounts with passbooks on sale 10 years ago, there should have been a savings card version which worked in the same way and which would have been a closer match to what you asked for than a JISA that locks away money until the child is 18. They will rely on you had 14 days from opening to realise that the account wasn’t actually suitable and close it and given the time that’s passed there’s unlikely to be evidence of you being advised incorrectly.

b) When I withdrew from a Nationwide Help To Buy ISA, there was a prominent warning that this was an ISA and references to allowances - so it seems very poor that an internal transfer about to go to a JISA and be locked away is not flagged in a similar way. The absence of a similar warning obviously contributed to the mistake that now leaves you in a very bad situation: overdrawn, and with a moral obligation to find the same for your new child at some point so that the two are treated fairly.

I don’t think there’s anything to lose by complaining that although you understand their hands are tied by the scheme rules, you feel let down that their poor advice and lack of warning has contributed to the situation. It might get a small goodwill ‘go away’ payment or period of 0% overdraft which is better than nothing.

1 -

I have spoken to HMRC and they told me that it can be reversed, I need to speak to nationwide but nationwide aren’t even communicating with me now. I tried to phone earlier and when i eventually got through to someone, I got cut off! I have now contacted nationwide via twitter because it seems that’s the only place they listen.Kim_13 said:

In light of this I would consider opening up a current account with someone other than Nationwide (it’s perfectly acceptable and in fact best practice to retain two or more current accounts with different banks, in case of interrupted service from the first) and get DWP/employer/anyone else to pay into that account, so that you have to actively move money to Nationwide to fund your son’s JISA and can’t make an accidental subscription again.Nataliel14 said:

I can’t remove the JISA from my account, it’s linked. I’ve got to go to the bank this morning so I’ll speak to them. I’ve never made this mistake before I’m fuming with myself.jimjames said:I'd also ensure you delete that payee to prevent it happening again

While Nationwide’s hands are tied by the JISA rules, they haven’t dealt with you well on the basis that:

a) Passbooks weren’t actually withdrawn until February this year, so they could have opened the type of account you wanted. Even if there were no child accounts with passbooks on sale 10 years ago, there should have been a savings card version which worked in the same way and which would have been a closer match to what you asked for than a JISA that locks away money until the child is 18. They will rely on you had 14 days from opening to realise that the account wasn’t actually suitable and close it and given the time that’s passed there’s unlikely to be evidence of you being advised incorrectly.

b) When I withdrew from a Nationwide Help To Buy ISA, there was a prominent warning that this was an ISA and references to allowances - so it seems very poor that an internal transfer about to go to a JISA and be locked away is not flagged in a similar way. The absence of a similar warning obviously contributed to the mistake that now leaves you in a very bad situation: overdrawn, and with a moral obligation to find the same for your new child at some point so that the two are treated fairly.

I don’t think there’s anything to lose by complaining that although you understand their hands are tied by the scheme rules, you feel let down that their poor advice and lack of warning has contributed to the situation. It might get a small goodwill ‘go away’ payment or period of 0% overdraft which is better than nothing.I agree that there should be some sort of warning when transferring into the ISA. There was no warning at all. I’m usually very very careful when I transfer money.I need my money back, there’s no if or buts about that unfortunately. Even if they offer a good will payment, which I don’t think they will, that’s not what needs to happen. I have spoken to a few people who have made a similar mistake and have had their money returned.0 -

Nataliel14 said:

I have spoken to HMRC and they told me that it can be reversed, I need to speak to nationwide but nationwide aren’t even communicating with me now. I tried to phone earlier and when i eventually got through to someone, I got cut off! I have now contacted nationwide via twitter because it seems that’s the only place they listen.Kim_13 said:

In light of this I would consider opening up a current account with someone other than Nationwide (it’s perfectly acceptable and in fact best practice to retain two or more current accounts with different banks, in case of interrupted service from the first) and get DWP/employer/anyone else to pay into that account, so that you have to actively move money to Nationwide to fund your son’s JISA and can’t make an accidental subscription again.Nataliel14 said:

I can’t remove the JISA from my account, it’s linked. I’ve got to go to the bank this morning so I’ll speak to them. I’ve never made this mistake before I’m fuming with myself.jimjames said:I'd also ensure you delete that payee to prevent it happening again

While Nationwide’s hands are tied by the JISA rules, they haven’t dealt with you well on the basis that:

a) Passbooks weren’t actually withdrawn until February this year, so they could have opened the type of account you wanted. Even if there were no child accounts with passbooks on sale 10 years ago, there should have been a savings card version which worked in the same way and which would have been a closer match to what you asked for than a JISA that locks away money until the child is 18. They will rely on you had 14 days from opening to realise that the account wasn’t actually suitable and close it and given the time that’s passed there’s unlikely to be evidence of you being advised incorrectly.

b) When I withdrew from a Nationwide Help To Buy ISA, there was a prominent warning that this was an ISA and references to allowances - so it seems very poor that an internal transfer about to go to a JISA and be locked away is not flagged in a similar way. The absence of a similar warning obviously contributed to the mistake that now leaves you in a very bad situation: overdrawn, and with a moral obligation to find the same for your new child at some point so that the two are treated fairly.

I don’t think there’s anything to lose by complaining that although you understand their hands are tied by the scheme rules, you feel let down that their poor advice and lack of warning has contributed to the situation. It might get a small goodwill ‘go away’ payment or period of 0% overdraft which is better than nothing.I agree that there should be some sort of warning when transferring into the ISA. There was no warning at all. I’m usually very very careful when I transfer money.I need my money back, there’s no if or buts about that unfortunately. Even if they offer a good will payment, which I don’t think they will, that’s not what needs to happen. I have spoken to a few people who have made a similar mistake and have had their money returned.You really need to get something in writing from HMRC saying that to take to Nationwide, because it runs completely contrary to what is published on the gov.uk website by HMRC. It is not in the gift of Nationwide to make an exception to the rules, but HMRC could instruct them to do it (though not legally, as far as I can see*).This is the official guidance from HMRC to Nationwide and other ISA managers (as linked above):

* Relevant legislation:1

* Relevant legislation:1 -

Exactly how similar (recognising that JISA isn't like other types of account when it comes to reversal of deposits, except perhaps fixed term non-ISA accounts)?Nataliel14 said:

I have spoken to a few people who have made a similar mistake and have had their money returned.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards