We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Debt help

Comments

-

Thank you for your help and adviceMattMattMattUK said:

Working through those quickly and things that I would queryTrainspotter90 said:

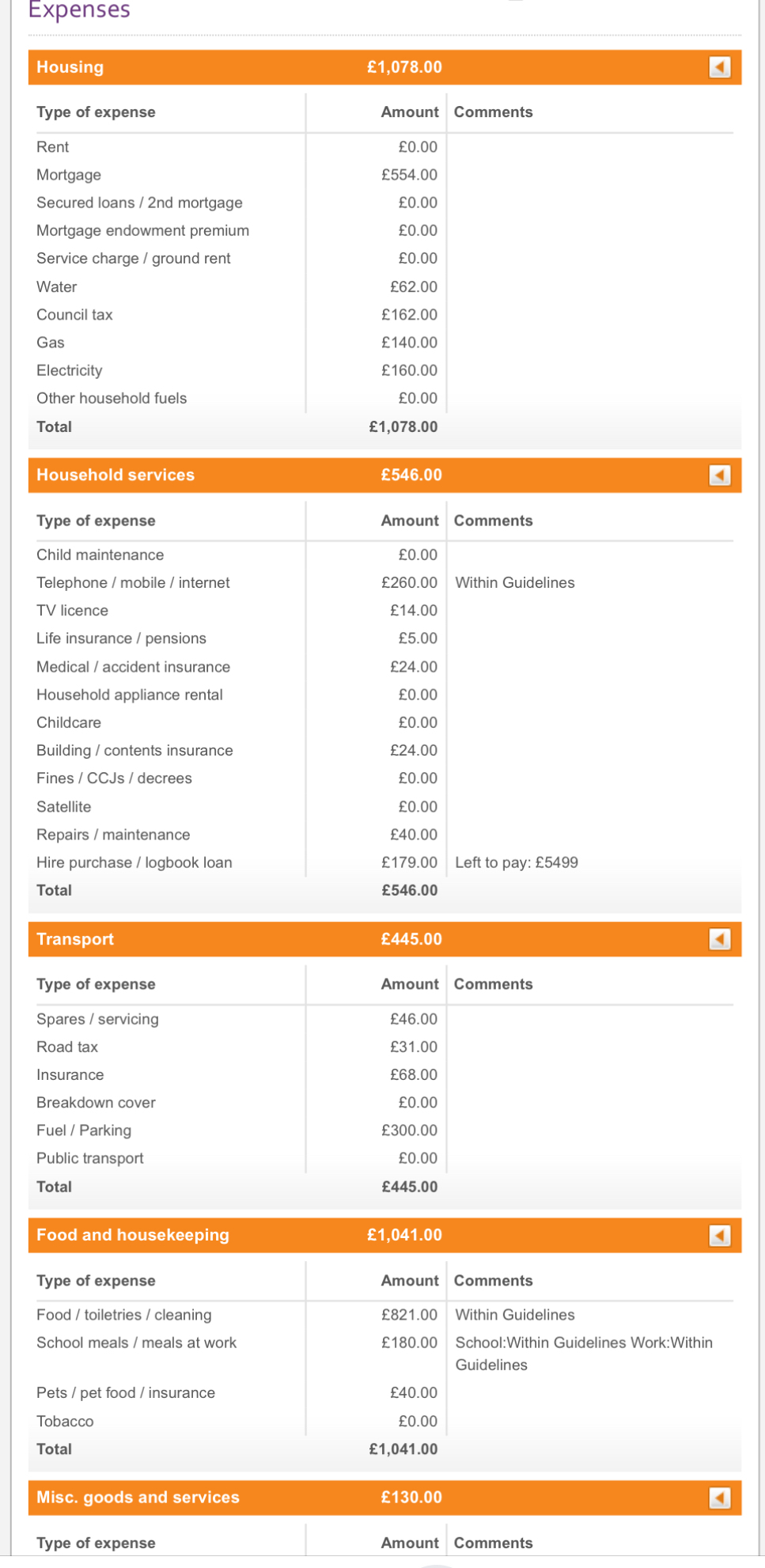

This is my income and expenditure that I did with Stepchange

This is my income and expenditure that I did with Stepchange

Water: £62 - That is a huge amount of water, either you are on a rateable value or you have a leak if you are on a meter. Get a meter installed and you should be down to £30 ish.

Gas & Electricity: £300 - This is more than twice the average for a family of four, you should be able to halve this.

Telephone/Mobile/Internet: £260 - Insanely high. A SIM Only option should be no more than £10 per month and good home broadband £30, maybe £40 if you have a genuine need (eg. video editing for work) for a very high speed internet connection.

HP Loan £179 - What is this linked to? What asset, what value of asset, what terms?

Spares/Servicing: £46 - Seems high

Road Tax: £31 - Is this for two vehicles?

Insurance: £68 - Is this for two vehicles?

Fuel/Parking £300 - A very round figure and seems high for fuel, it would indicate 2,500 miles a month which even for two people is very high compared to normal usage figures.

Food: £821 - Seems high

That should be an easy saving of £700+ a month which gives you a much more reasonable headroom, allows you to build up an emergency fund a lot more quicky.

Also the money you save whilst not paying the debts so that they default would also be considerable, the £2,700 per month, so you could have a emergency fund of £10k by the time they all default.

Yes, you want them all to default.Trainspotter90 said:

I thought I was doing the right thing by paying into a DMP? So you’re saying I should let them all default now? I have agreed with the companies to make payments via this plan which they have all accepted?

Have you addressed your spending now? Are you and your partner prepared for the next few years being minimal non-essential spending? You are going to be unable to make any additional borrowing for several years going forward now so you need to plan, keep an emergency fund, no impulse spending. I am not saying it is going to be difficult, but it will not be easy initially as it requires a change in mindset and you and your partner both need to accept that or it will not work.Trainspotter90 said:in terms of why? I was the only one working at the time so buying house and unexpected bills didn’t help and needing a new car, but most of it was poor spending and then I’d take out a loan to pay the other one off or a credit card but then something would come up which I needed it for and just hit a rut and didn’t know how to get out

water not on a meter just monthly rate I’ve been given based in wales

hp loan is for my van I have have 3 years left on it to pay off

road tax and insurance is for two vehicles

fuel I have a diesel van so more expensive and travelling back and fore to work and football coach do clock up a lot of mileage

food this is for family of 4 probably could get it down a bit we do but a lot of fresh food and cook a lot but is an area I could look at year thank you

with the accounts defaulting I was just worried I would lose my house I’ve never been in this situation and still don’t really know what I’m doing …would step change advise me to default? I don’t have any emergency funds at moment

In terms of credit etc once I’ve paid all this off in 4 years I will never borrow again because of this experience I have gone through0 -

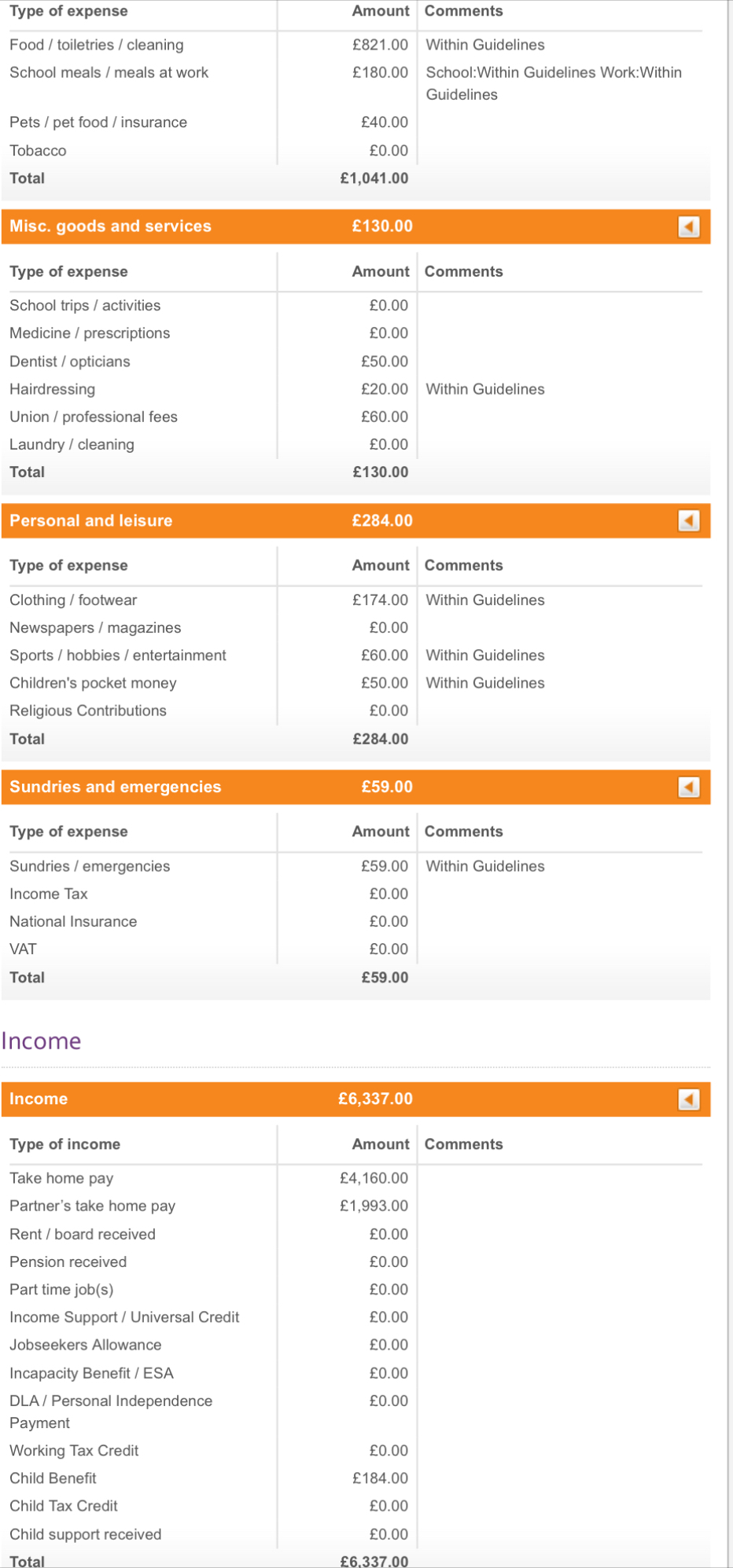

I see that there's pocket money for the kids but nothing for school trips or activities? Either the kids are very young or perhaps they're old enough to have after school jobs to fund extras themselves.

edited to add: when you gave the explanation about how you got into so much debt I almost laughed as it sounded much too similar to me. It's take a while but all the debts will be cleared this year which is such a relief. It might take you longer than you think but getting things under control is excellent.I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅0 -

It will only be a small saving, but get a meter installed, everything helps.Trainspotter90 said:

Thank you for your help and adviceMattMattMattUK said:

Working through those quickly and things that I would queryTrainspotter90 said:This is my income and expenditure that I did with Stepchange

Water: £62 - That is a huge amount of water, either you are on a rateable value or you have a leak if you are on a meter. Get a meter installed and you should be down to £30 ish.

Gas & Electricity: £300 - This is more than twice the average for a family of four, you should be able to halve this.

Telephone/Mobile/Internet: £260 - Insanely high. A SIM Only option should be no more than £10 per month and good home broadband £30, maybe £40 if you have a genuine need (eg. video editing for work) for a very high speed internet connection.

HP Loan £179 - What is this linked to? What asset, what value of asset, what terms?

Spares/Servicing: £46 - Seems high

Road Tax: £31 - Is this for two vehicles?

Insurance: £68 - Is this for two vehicles?

Fuel/Parking £300 - A very round figure and seems high for fuel, it would indicate 2,500 miles a month which even for two people is very high compared to normal usage figures.

Food: £821 - Seems high

That should be an easy saving of £700+ a month which gives you a much more reasonable headroom, allows you to build up an emergency fund a lot more quicky.

Also the money you save whilst not paying the debts so that they default would also be considerable, the £2,700 per month, so you could have a emergency fund of £10k by the time they all default.

Yes, you want them all to default.Trainspotter90 said:

I thought I was doing the right thing by paying into a DMP? So you’re saying I should let them all default now? I have agreed with the companies to make payments via this plan which they have all accepted?

Have you addressed your spending now? Are you and your partner prepared for the next few years being minimal non-essential spending? You are going to be unable to make any additional borrowing for several years going forward now so you need to plan, keep an emergency fund, no impulse spending. I am not saying it is going to be difficult, but it will not be easy initially as it requires a change in mindset and you and your partner both need to accept that or it will not work.Trainspotter90 said:in terms of why? I was the only one working at the time so buying house and unexpected bills didn’t help and needing a new car, but most of it was poor spending and then I’d take out a loan to pay the other one off or a credit card but then something would come up which I needed it for and just hit a rut and didn’t know how to get out

water not on a meter just monthly rate I’ve been given based in wales

Ok, so not much you can do about the vehicle cost, but still a lot of miles, make sure you are claiming for the miles you do for work correctly, either via your mileage, or self assessment.Trainspotter90 said:hp loan is for my van I have have 3 years left on it to pay off

road tax and insurance is for two vehicles

fuel I have a diesel van so more expensive and travelling back and fore to work and football coach do clock up a lot of mileage

Even then it still seems high and cooking from fresh should save you money, not cost you more. Try to recipe plan, reduce wastage, use less red meat etc. It is amazing how small changes can save quite a lot of money and have zero impact on one's enjoyment of the food and meals. Also considering getting an additional freezer if you have space for it, for the £200-300 initial outlay it is amazing how much you can save if you buy certain things, especially meat, when it is reduced or on offer.Trainspotter90 said:

food this is for family of 4 probably could get it down a bit we do but a lot of fresh food and cook a lot but is an area I could look at year thank you

Nope, that will not happen. You do need to think about who your mortgage is, vs any of the other debts and ideally not default on those. Also if you have any debts linked to your current account then you need a new current account before you default. Brie, FatBelly and others can give much clearer advice on the defaulting process and how to manage it, but essentially you want you need to stop paying, save that money and let all the debts default.Trainspotter90 said:

with the accounts defaulting I was just worried I would lose my house I’ve never been in this situation and still don’t really know what I’m doing …would step change advise me to default? I don’t have any emergency funds at moment

It is not the four years time you need to think about now, it is four days four weeks and four months. The spending patterns that have happened to build up more than £130k of debt take a real mindset change. When the next thing comes along that you would have previously resorted to debt to fund what will you do? That is where the need for an emergency fund comes in, if you hit a pot hole and need to repair your work van you have the money, if your fridge dies and you need a new one you have the money, but also the frivolous purchases cannot happen. You need a small "fun" budget, especially as you have children, you need to live not just exist, but equally expenditure has to be budgeted and affordable and that does take a mindset change, it is something you and your partner will need to talk about regularly to support each other through this as it will feel tough at points, when friends are booking holidays abroad, buying new cars, going out for meals etc. you will have to be restrained and that adjustment takes time and will be much easier if you work through it together.Trainspotter90 said:

In terms of credit etc once I’ve paid all this off in 4 years I will never borrow again because of this experience I have gone through

3 -

You are now in debt management, and have started down the road to paying off your debt, this is a good thing.

Normally, we do advise defaulting first, for reasons already stated by others, but in your case, with such a large amount of debt, you might not want to be able to start borrowing again anytime soon, so your credit file should not be your greatest concern.

Even in debt management, CCJ`s are possible, especially with any large single debt, the creditor may want to strengthen their position by securing the debt on your home by way of a charging order, now this is fairly common amongst those with an asset with large amounts of equity, but as long as payments are maintained, that creditor cannot obtain an order for sale, which in themselves are now so rare, official figures are no longer kept.

So you will not lose your home over this, you have a good income between you, keep up the payments, your accounts will default at some point, and if they don`t you can complain about that.

Another important thing is to try and save an emergency fund, you will get settlement offers in time, that you may want to take advantage of, to get out of debt quicker, so keep that in mind, just a case of knuckling down now really, and keep your spending in check, as next time you may not be so lucky.

Good luck with it, any questions, feel free to ask on this thread.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

Thank you for the advice much appreciatedsourcrates said:You are now in debt management, and have started down the road to paying off your debt, this is a good thing.

Normally, we do advise defaulting first, for reasons already stated by others, but in your case, with such a large amount of debt, you might not want to be able to start borrowing again anytime soon, so your credit file should not be your greatest concern.

Even in debt management, CCJ`s are possible, especially with any large single debt, the creditor may want to strengthen their position by securing the debt on your home by way of a charging order, now this is fairly common amongst those with an asset with large amounts of equity, but as long as payments are maintained, that creditor cannot obtain an order for sale, which in themselves are now so rare, official figures are no longer kept.

So you will not lose your home over this, you have a good income between you, keep up the payments, your accounts will default at some point, and if they don`t you can complain about that.

Another important thing is to try and save an emergency fund, you will get settlement offers in time, that you may want to take advantage of, to get out of debt quicker, so keep that in mind, just a case of knuckling down now really, and keep your spending in check, as next time you may not be so lucky.

Good luck with it, any questions, feel free to ask on this thread.

we have only been in the DMP for 4 months but our mentality has definitely changed and we do budget more now setting specific amounts weekly and making sure we don’t go over and only buying what we need and no more impulsive buys this month especially has been difficult with people we know going on holidays but it is what it is we can do camping trips which is still affordable it is tough and been a strain on our marriage but I take responsibility as I pay all the bills etc, I’ve never missed any payments until January when we struggled but always paid mortgage and priority bills are all up to date!Can I just ask even though I’m on a DMP and payments plans with the companies I owe money too I should just stop paying ? Won’t that affect my agreement with Stepchange?Also what’s the likely of what happens next with MBNA and Zopa as both have defaulted? What would the next steps be?Thank you all again for your help to say I’m embarrassed is an understatement0 -

I’m going to give you an idea that you can get your food shopping down quite a bit. I shop for a minimum of six people, but i can feed anywhere up to 11 people if all my kids are at home and all their partners are here as well. My food budget each week is £150. This is packed lunches for five people, includes all toiletries and cleaning stuff. My older two kids sometimes get themselves something for dinner, but I feed everyone breakfast every day. Eight people live here permanently. You currently have a budget of £1000 per month for food including meals at school/work. So I’m already spending less than you and I’m feeding more kids. One of my boys is a teenager who can eat and eat and eat.In addition your clothing allowance looks high each month. I budget £100 each month and that is five peoples clothes, uniforms, shoes etc. again my older two girls buy their own clothes now as they are working. My husband buys his own clothes and shoes from his spending money usually but if I’m out and I know he needs something I will buy it.

Although to be fair I have been budgeting for a while and I did go through a time when I literally had very little money to live on, so I got used to shopping on a budget. Even though my budget is £150 a week, I very rarely actually spend £150 a week. Normally it’s between £120 and £130 a week. I think once you have had very little you get used to spending very little and don’t then increase your budget when you have the more money. Back about five years ago I was feeding myself and my six kids on max of £80 a week because I also needed petrol money to get to work and the only money I had coming in was child benefit and a small bit of child maintenance. I know this was a few years ago and prices have gone up but I haven’t increased my weekly food budget that much. What I have increased is my discretionery spending. So I now have a weekly pot for any guilt free spends I want, another pot for anything the kids need for school etc.

The other thing that has made a massive difference to me is every week when I get to the end of the week, if I have money over it goes into whatever I am saving for at the time, so could be a holiday, could be anything really. It’s amazing how quickly the money that is left adds up.2 -

As said in my earlier post, now your in it, I`d stick with it, given the amount of debt you have.Trainspotter90 said:

Thank you for the advice much appreciatedsourcrates said:

Normally, we do advise defaulting first, for reasons already stated by others, but in your case, with such a large amount of debt, you might not want to be able to start borrowing again anytime soon, so your credit file should not be your greatest concern.Can I just ask even though I’m on a DMP and payments plans with the companies I owe money too I should just stop paying ? Won’t that affect my agreement with Stepchange?Also what’s the likely to happen next with MBNA and Zopa as both have defaulted? What would the next steps be?

You do not really want county court judgements and charging orders, and all the extra hassle that creates.

If you didn`t own a house, the advice would be different, yes, stop paying and let them all default first.

But in your circumstances, with that amount of debt a CCJ and CO are a real possibility, you should do all you can to avoid that.

That`s my opinion, others may see it differently.

Not much will happen now after default, as you are paying via the DMP.

Debts may be sold/assigned to collectors or stay in-house, whatever happens, stepchange will pay whoever is allotted to collect the debt, that`s it.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter2 -

How will i stop ccj or co? Really worried now you mentioned this …I thought setting up a DMP with Stepchange and maintaining the payments would of be ok?sourcrates said:

As said in my earlier post, now your in it, I`d stick with it, given the amount of debt you have.Trainspotter90 said:

Thank you for the advice much appreciatedsourcrates said:

Normally, we do advise defaulting first, for reasons already stated by others, but in your case, with such a large amount of debt, you might not want to be able to start borrowing again anytime soon, so your credit file should not be your greatest concern.Can I just ask even though I’m on a DMP and payments plans with the companies I owe money too I should just stop paying ? Won’t that affect my agreement with Stepchange?Also what’s the likely to happen next with MBNA and Zopa as both have defaulted? What would the next steps be?

You do not really want county court judgements and charging orders, and all the extra hassle that creates.

If you didn`t own a house, the advice would be different, yes, stop paying and let them all default first.

But in your circumstances, with that amount of debt a CCJ and CO are a real possibility, you should do all you can to avoid that.

That`s my opinion, others may see it differently.

Not much will happen now after default, as you are paying via the DMP.

Debts may be sold/assigned to collectors or stay in-house, whatever happens, stepchange will pay whoever is allotted to collect the debt, that`s it.0 -

You are mis-understanding what I`m saying.

What you have done already is the best way to remove the threat of further action by any particular creditor.

In my opinion you are doing the right thing, given your circumstances, so relax.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

How will i stop ccj or co? Really worried now you mentioned this …I thought setting up a DMP with Stepchange and maintaining the payments would of be ok?

I agree with @sourcrates advice to stay in the StepChange DMP.

You have a solution that looks like its going to work for you and its reasonably fast. It's when we see people with 12 or 20 year DMPs that they need to find other routes.

It is possible to get a CCJ when you are in a StepChange DMP, but it is very unlikely when you are paying a lot per month so the DMP will be over quickly. Suppose you are one of your creditors, it looks as though you will repay their debt in about 4 years, that sounds great to them. Why would they go to court for a CCJ when they are highly unlikely to get repaid any faster? Creditors (including debt collectors) aren't vindictive; they just like the money rolling in fast.

Your groceries and other expenses, perhaps you could get these down. For many people on here, that is one way they can speed up debt repayment, by cutting expenses. But you dont need to do this, you can if you want to. If you would rather have more days out with the kids, or want to emerge from the DMP with a bit of savings, then look for economies. But there is no particular need to speed up the DMP.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.6K Work, Benefits & Business

- 602.9K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards