We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Debt help

Comments

-

No, but there is scope for a charging order. Hopefully they wouldn't bother or be granted if you are making regular payments. That does allow them to charge statutory interest but is discharged when paid off.Trainspotter90 said:

CCJ what would happen with this would I lose my home?MattMattMattUK said:

Not directly, but I think you are misunderstanding. So if someone has no property and the debtor goes into a DMP the creditor will recognise that they have very little prospect of recovery if they push harder, the debtor could just go bankrupt. If the debtor has property then they are somewhat less free to just walk away from their debts, as such they not going to accept tiny DMP repayments, as evidenced by the OP's monthly figure representing around £100k of repayments over the period they mention.itsthelittlethings said:

I thought you could default and your property would not be affected?MattMattMattUK said:

If you are in a DMP you should have already let the accounts default, if not then you should stop paying until they do.Trainspotter90 said:Hello

wondered if you could help please?I’ve got myself into a tough situation which I know I’m responsible for and have made mistakes over the years I don’t think mentally I was in right place and have got £132,000 worth of debt that I’m now trying to pay off.I’ve gone through Stepchange to step up a DMP with them and making payments to companies I owe money too. Unfortunately some of these accounts are going to default and I’m worried about what’s going to happen next?

We will need a bit more information to be able to help, based on those figures you do not really have an issue with the repayments as you still have £2,892 left for everything else every month, which I am surprised your creditors are allowing you to cut your payments that low on that basis.Trainspotter90 said:Myself and and wife both work full time and bring home £6,200 month after tax in income! We are making payments to Stepchange of £2,754 month to pay off our debts for us! We have a mortgage which we are paying £554 month and no arrears from them!

That totals £132k of debt, give or take. Do you know what you have spent the money on? Have you cut your spending to a bare minimum now?Trainspotter90 said:Below are my debts and current balances- ZOPA BANK LOANS£18,130.29

- ZOPA BANK LOANS£17,663.13

- NOVUNA CONSUMER£13,816.64

- ZOPA BANK LOANS£13,120.72

- ZOPA BANK LOANS£12,618.47

- NOVUNA CONSUMER £12,151.63

- VIRGIN MONEY £10,457.95

- ZOPA BANK LOANS£9,281.49

- VIRGIN MONEY CRE£8,307.97

- MBNA Limited£5,290.15

- ZOPA BANK LOANS£4,727.08

- TSB BANK overdraft£2,246.41

- LINK FINANCIAL O...£1,779.92

- LINK FINANCIAL O...£1,674.54

- VIRGIN MONEY CRE...£1,552.39

You need to post a full SOA and we can help, but you also have to accept that with that level of debt and the fact that you own a property you are going to have to pay most of the debt back, the alternative is to sell your home and buy somewhere smaller, or rent.Trainspotter90 said:With me making payments to Stepchange I should be debt free by June 2028!Any advice on what I could possibly do next to help would be much appreciated, mentally I’m not in a great place been having panic attacks and struggling to sleep too!Thank you in advance and appreciate your help.

There is the theoretical option of a CCJ and a charging order, which secures the debt against the property, they are rare but I would not totally rule it out, especially as £75k of the debt is to one lender, Zopa.

You will need to select a new fix with your existing mortgage supplier until this clears.If you've have not made a mistake, you've made nothing0 -

RAS said:

No, but there is scope for a charging order. Hopefully they wouldn't bother or be granted if you are making regular payments. That does allow them to charge statutory interest but is discharged when paid off.Trainspotter90 said:

CCJ what would happen with this would I lose my home?MattMattMattUK said:

Not directly, but I think you are misunderstanding. So if someone has no property and the debtor goes into a DMP the creditor will recognise that they have very little prospect of recovery if they push harder, the debtor could just go bankrupt. If the debtor has property then they are somewhat less free to just walk away from their debts, as such they not going to accept tiny DMP repayments, as evidenced by the OP's monthly figure representing around £100k of repayments over the period they mention.itsthelittlethings said:

I thought you could default and your property would not be affected?MattMattMattUK said:

If you are in a DMP you should have already let the accounts default, if not then you should stop paying until they do.Trainspotter90 said:Hello

wondered if you could help please?I’ve got myself into a tough situation which I know I’m responsible for and have made mistakes over the years I don’t think mentally I was in right place and have got £132,000 worth of debt that I’m now trying to pay off.I’ve gone through Stepchange to step up a DMP with them and making payments to companies I owe money too. Unfortunately some of these accounts are going to default and I’m worried about what’s going to happen next?

We will need a bit more information to be able to help, based on those figures you do not really have an issue with the repayments as you still have £2,892 left for everything else every month, which I am surprised your creditors are allowing you to cut your payments that low on that basis.Trainspotter90 said:Myself and and wife both work full time and bring home £6,200 month after tax in income! We are making payments to Stepchange of £2,754 month to pay off our debts for us! We have a mortgage which we are paying £554 month and no arrears from them!

That totals £132k of debt, give or take. Do you know what you have spent the money on? Have you cut your spending to a bare minimum now?Trainspotter90 said:Below are my debts and current balances- ZOPA BANK LOANS£18,130.29

- ZOPA BANK LOANS£17,663.13

- NOVUNA CONSUMER£13,816.64

- ZOPA BANK LOANS£13,120.72

- ZOPA BANK LOANS£12,618.47

- NOVUNA CONSUMER £12,151.63

- VIRGIN MONEY £10,457.95

- ZOPA BANK LOANS£9,281.49

- VIRGIN MONEY CRE£8,307.97

- MBNA Limited£5,290.15

- ZOPA BANK LOANS£4,727.08

- TSB BANK overdraft£2,246.41

- LINK FINANCIAL O...£1,779.92

- LINK FINANCIAL O...£1,674.54

- VIRGIN MONEY CRE...£1,552.39

You need to post a full SOA and we can help, but you also have to accept that with that level of debt and the fact that you own a property you are going to have to pay most of the debt back, the alternative is to sell your home and buy somewhere smaller, or rent.Trainspotter90 said:With me making payments to Stepchange I should be debt free by June 2028!Any advice on what I could possibly do next to help would be much appreciated, mentally I’m not in a great place been having panic attacks and struggling to sleep too!Thank you in advance and appreciate your help.

There is the theoretical option of a CCJ and a charging order, which secures the debt against the property, they are rare but I would not totally rule it out, especially as £75k of the debt is to one lender, Zopa.

You will need to select a new fix with your existing mortgage supplier until this clears.

Ok thank you is there anything I should be worried about?RAS said:

No, but there is scope for a charging order. Hopefully they wouldn't bother or be granted if you are making regular payments. That does allow them to charge statutory interest but is discharged when paid off.Trainspotter90 said:

CCJ what would happen with this would I lose my home?MattMattMattUK said:

Not directly, but I think you are misunderstanding. So if someone has no property and the debtor goes into a DMP the creditor will recognise that they have very little prospect of recovery if they push harder, the debtor could just go bankrupt. If the debtor has property then they are somewhat less free to just walk away from their debts, as such they not going to accept tiny DMP repayments, as evidenced by the OP's monthly figure representing around £100k of repayments over the period they mention.itsthelittlethings said:

I thought you could default and your property would not be affected?MattMattMattUK said:

If you are in a DMP you should have already let the accounts default, if not then you should stop paying until they do.Trainspotter90 said:Hello

wondered if you could help please?I’ve got myself into a tough situation which I know I’m responsible for and have made mistakes over the years I don’t think mentally I was in right place and have got £132,000 worth of debt that I’m now trying to pay off.I’ve gone through Stepchange to step up a DMP with them and making payments to companies I owe money too. Unfortunately some of these accounts are going to default and I’m worried about what’s going to happen next?

We will need a bit more information to be able to help, based on those figures you do not really have an issue with the repayments as you still have £2,892 left for everything else every month, which I am surprised your creditors are allowing you to cut your payments that low on that basis.Trainspotter90 said:Myself and and wife both work full time and bring home £6,200 month after tax in income! We are making payments to Stepchange of £2,754 month to pay off our debts for us! We have a mortgage which we are paying £554 month and no arrears from them!

That totals £132k of debt, give or take. Do you know what you have spent the money on? Have you cut your spending to a bare minimum now?Trainspotter90 said:Below are my debts and current balances- ZOPA BANK LOANS£18,130.29

- ZOPA BANK LOANS£17,663.13

- NOVUNA CONSUMER£13,816.64

- ZOPA BANK LOANS£13,120.72

- ZOPA BANK LOANS£12,618.47

- NOVUNA CONSUMER £12,151.63

- VIRGIN MONEY £10,457.95

- ZOPA BANK LOANS£9,281.49

- VIRGIN MONEY CRE£8,307.97

- MBNA Limited£5,290.15

- ZOPA BANK LOANS£4,727.08

- TSB BANK overdraft£2,246.41

- LINK FINANCIAL O...£1,779.92

- LINK FINANCIAL O...£1,674.54

- VIRGIN MONEY CRE...£1,552.39

You need to post a full SOA and we can help, but you also have to accept that with that level of debt and the fact that you own a property you are going to have to pay most of the debt back, the alternative is to sell your home and buy somewhere smaller, or rent.Trainspotter90 said:With me making payments to Stepchange I should be debt free by June 2028!Any advice on what I could possibly do next to help would be much appreciated, mentally I’m not in a great place been having panic attacks and struggling to sleep too!Thank you in advance and appreciate your help.

There is the theoretical option of a CCJ and a charging order, which secures the debt against the property, they are rare but I would not totally rule it out, especially as £75k of the debt is to one lender, Zopa.

You will need to select a new fix with your existing mortgage supplier until this clears.I’ve been making DMP payment with Stepchange since February and no payments missed and on time?

im waiting for MBNA to get back to me regarding the default shall I make contact with them or do Stepchange manage this for me?0 -

Post a full SOA, without that we are having to make a lot of assumptions and guesses.0

-

What is a SOA?MattMattMattUK said:Post a full SOA, without that we are having to make a lot of assumptions and guesses.0 -

Trainspotter90 said:

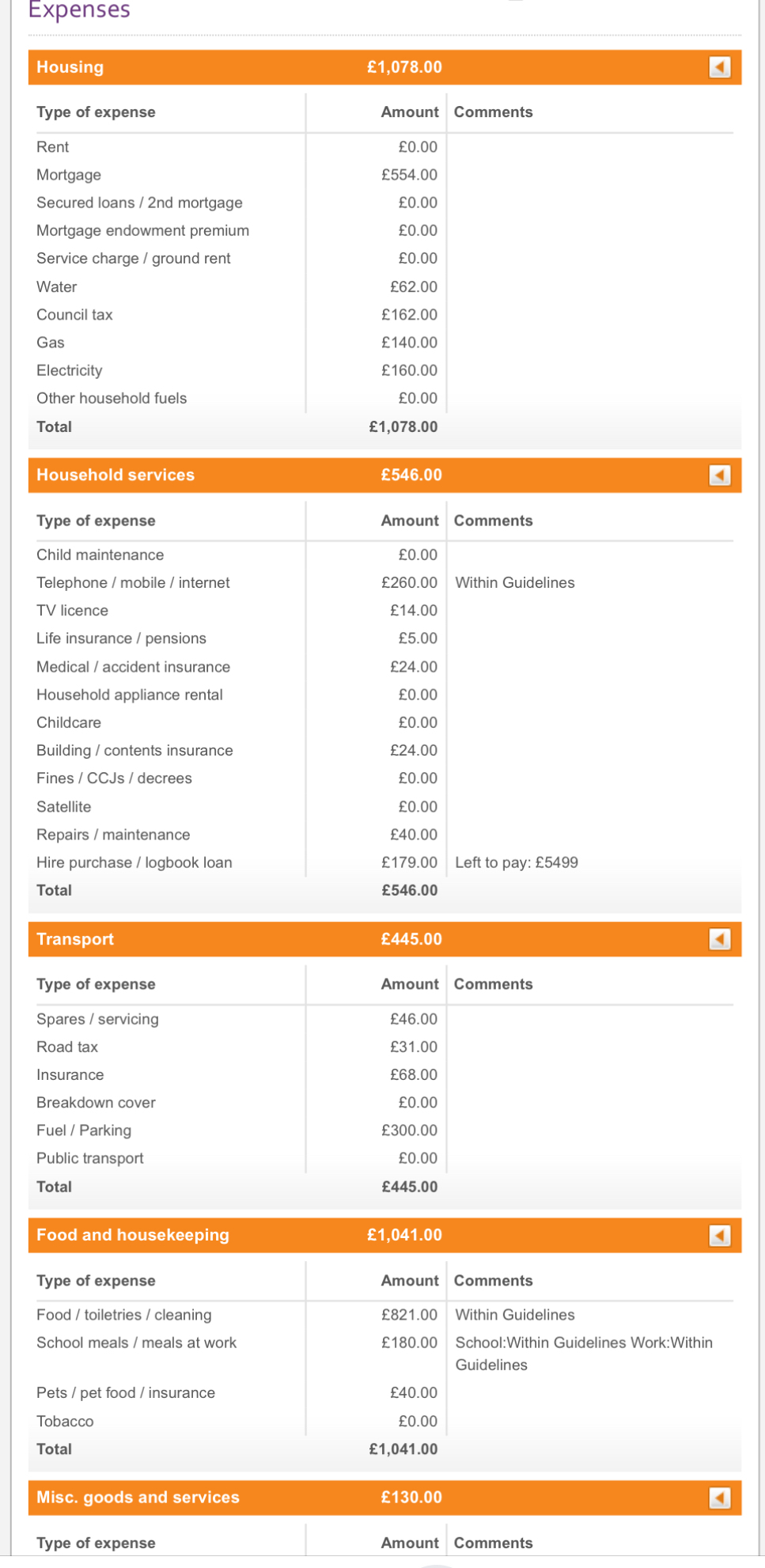

What is a SOA?MattMattMattUK said:Post a full SOA, without that we are having to make a lot of assumptions and guesses.Expenses

- Housing£1,078.00

Type of expense Amount Comments Rent £0.00 Mortgage £554.00 Secured loans / 2nd mortgage £0.00 Mortgage endowment premium £0.00 Service charge / ground rent £0.00 Water £62.00 Council tax £162.00 Gas £140.00 Electricity £160.00 Other household fuels £0.00 Total £1,078.00 - Household services£546.00

- Transport£445.00

- Food and housekeeping£1,041.00

- Misc. goods and services£130.00

- Personal and leisure£284.00

- Sundries and emergencies£59.00

Income

- Income£6,337.00

Type of income Amount Comments Take home pay £4,160.00 Partner’s take home pay £1,993.00 Rent / board received £0.00 Pension received £0.00 Part time job(s) £0.00 Income Support / Universal Credit £0.00 Jobseekers Allowance £0.00 Incapacity Benefit / ESA £0.00 DLA / Personal Independence Payment £0.00 Working Tax Credit £0.00 Child Benefit £184.00 Child Tax Credit £0.00 Child support received £0.00 Total £6,337.00

0 -

Total income£6,337.00Total expenses£3,583.00Surplus£2,754.00

0 -

The link is in this postMattMattMattUK said:First, can you post a full SOA?

https://www.lemonfool.co.uk/financecalculators/soa.phpIf you go down to the woods today you better not go alone.1 -

Those look like the SFS categories that StepChange will have allocated all of your detailed expenses lines too, but it is more helpful for us if we can see all the individual expense lines eg groceries, mobiles, car insurance, clothes etc etc At the moment we have no feel for how realistic it is

Don't worry about defaults, defaults are your friends as they mean your credit record will be clean sooner.

The suggestion to make affordability complaints against the larger creditors looks sensible, eg Zopa, Novuna, Virgin. Any you can win will speed up the DMP.

1 -

This is my income and expenditure that I did with Stepchange0

This is my income and expenditure that I did with Stepchange0 -

Working through those quickly and things that I would queryTrainspotter90 said:This is my income and expenditure that I did with Stepchange

Water: £62 - That is a huge amount of water, either you are on a rateable value or you have a leak if you are on a meter. Get a meter installed and you should be down to £30 ish.

Gas & Electricity: £300 - This is more than twice the average for a family of four, you should be able to halve this.

Telephone/Mobile/Internet: £260 - Insanely high. A SIM Only option should be no more than £10 per month and good home broadband £30, maybe £40 if you have a genuine need (eg. video editing for work) for a very high speed internet connection.

HP Loan £179 - What is this linked to? What asset, what value of asset, what terms?

Spares/Servicing: £46 - Seems high

Road Tax: £31 - Is this for two vehicles?

Insurance: £68 - Is this for two vehicles?

Fuel/Parking £300 - A very round figure and seems high for fuel, it would indicate 2,500 miles a month which even for two people is very high compared to normal usage figures.

Food: £821 - Seems high

That should be an easy saving of £700+ a month which gives you a much more reasonable headroom, allows you to build up an emergency fund a lot more quicky.

Also the money you save whilst not paying the debts so that they default would also be considerable, the £2,700 per month, so you could have a emergency fund of £10k by the time they all default.

Yes, you want them all to default.Trainspotter90 said:

I thought I was doing the right thing by paying into a DMP? So you’re saying I should let them all default now? I have agreed with the companies to make payments via this plan which they have all accepted?

Have you addressed your spending now? Are you and your partner prepared for the next few years being minimal non-essential spending? You are going to be unable to make any additional borrowing for several years going forward now so you need to plan, keep an emergency fund, no impulse spending. I am not saying it is going to be difficult, but it will not be easy initially as it requires a change in mindset and you and your partner both need to accept that or it will not work.Trainspotter90 said:in terms of why? I was the only one working at the time so buying house and unexpected bills didn’t help and needing a new car, but most of it was poor spending and then I’d take out a loan to pay the other one off or a credit card but then something would come up which I needed it for and just hit a rut and didn’t know how to get out

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.6K Work, Benefits & Business

- 602.9K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards