We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Property probate trust nightmare

Comments

-

That's it - thank you0 -

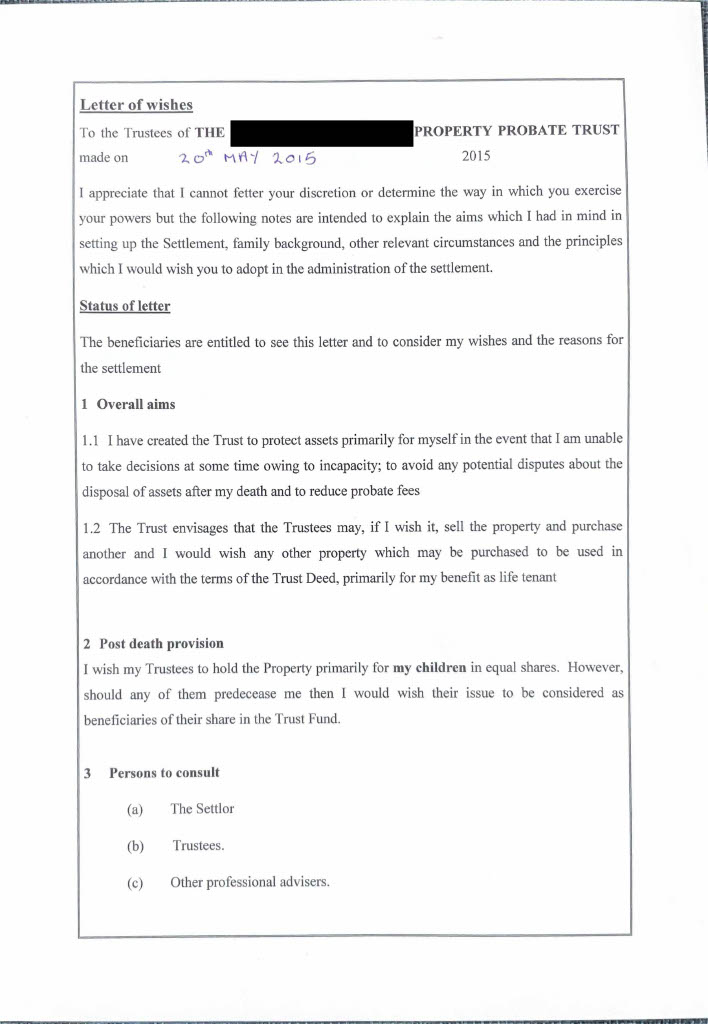

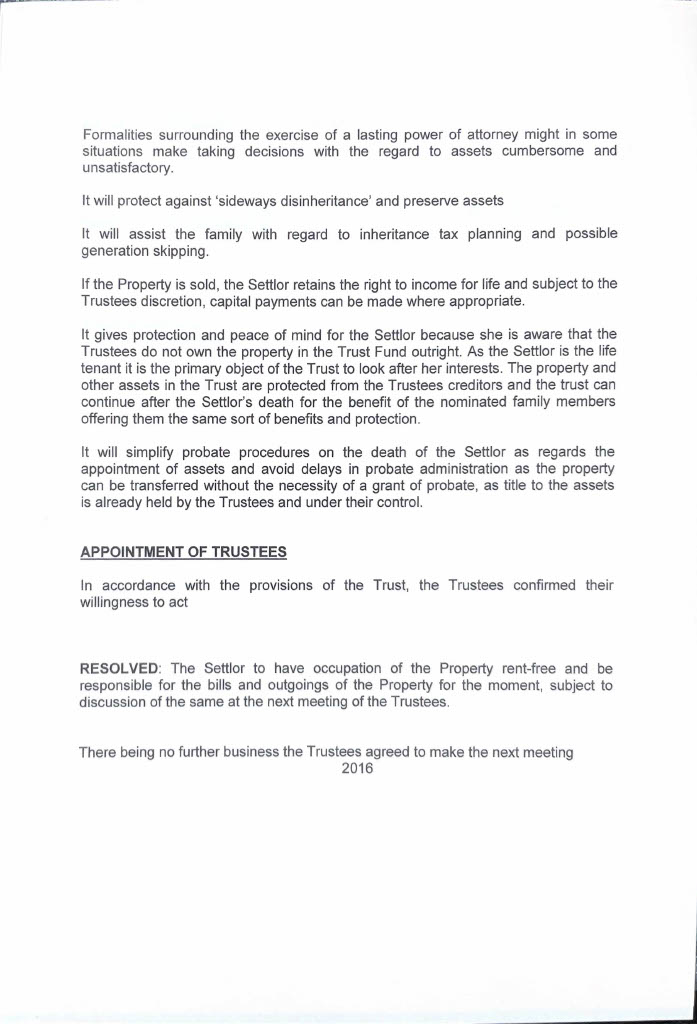

Having examined the pertinent clauses of the deed, sad to report that the family have indeed been lumbered with an unnecessarily complex trust that does not terminate on the life tenant's death.

Instead, a discretionary trust now exists following the death of the mother, and a further deed appointing the benefit of the property to the beneficiaries will be needed to bring it to an end. The discretionary trust may also have a pernicious effect on the residence nil rate bands (RNRB).

As regards tax compliance matters note the following:

* The value of the property at date of mother's death is reportable for probate and IHT purposes. An IHT return will be required

* As indicated above the deceased husband and mother's RNRBs of £175k each may now well be in question because the direct heirs do not automatically inherit the property on the mother's death. A potentially calamitous result of the continuing discretionary trust. However, both parents £325k nil rate bands should remain available as long as no part of the husband's nil rate band was used on his death.

*The discretionary trust does have a fast approaching 10 year anniversary IHT reporting obligation in May this year. If the Trust is not terminated prior to, there may likely be a 6% IHT charge on the value of the property exceeding the nil rate band.

* Capital gains tax - this is unclear. Had the trust automatically terminated on death in favour of the children, the automatic uplift to market value would have erased all prior years capital appreciation from the date the trust was established. There is a question mark here therefore, whether at trust level the original value of the property at the date of gift is still extant. Professional advice therefore required to ensure whether at trust level the main residence CGT exemption can be claimed by the trustees via the life tenant's prior period of occupation of the property. On the positive note, I see nothing in the trust preventing that possibility.

You are now in urgent deed of professional (competent) advice to deal with both probate and termination of the trust. You need to find a STEP qualified law firm ASAP whose first order of business will be termination of the trust before the anniversary date in May. STEP is the Society of Trust and Estate Practitioners and represents the higher echelons of expertise in trust and estate matters. Link to the STEP directory below

https://www.step.org/about-step/public

Hopefully deprivation of the resident nil rate bands will not trigger an IHT liability on your mother's death, but if so perhaps the law firm will be able to advise if you have a cause of action to sue the Will writing/Trust firms responsible for any loss in this regard.

As a side comment, these forms of overly complex trusts have absolutely no place in the estate planning for average members of the public whose primary assets are the family home. In the present case, what should have been a simple transition ( by will ) from mother to children has become a monstrously complex dismantling process of a trust structure that should never have been conceived for such a small simple estate.

5 -

I think the wording in the trust document regarding probate, has actually been put there as ‘evidence’ that the reason for the trust was not to avoid care costs, in reality the estate anyone who dies who was a beneficiary of a substantial trust is going to have to submit an IHT return which means a probate application as well.There must be many thousands of families out there who are in blissful ignorance of the difficulties they are going to face once their parents die and they have to deal with the mess these sharks have created.0

-

OMG. This is a disaster. I can't now even find a firm to take this on, all too busy dealing with existing clients :'(0

-

I agree, the supporting written evidence very carefully avoids mentioning care home fees avoidance, but one can guarantee this arose verbally both before and after execution of the deed, since for such a small simple estate there is no other valid reason for such a trust.Keep_pedalling said:I think the wording in the trust document regarding probate, has actually been put there as ‘evidence’ that the reason for the trust was not to avoid care costs, in reality the estate anyone who dies who was a beneficiary of a substantial trust is going to have to submit an IHT return which means a probate application as well.There must be many thousands of families out there who are in blissful ignorance of the difficulties they are going to face once their parents die and they have to deal with the mess these sharks have created.

I am sure you are absolutely correct about there being many thousands of unsuspecting families having been outright conned into these arrangements. My last specific thread on the subject (link below) is just one small example, but this time sadly perpetrated by a law firm in Scotland going bust with 20,000 Trusts on its books.

https://forums.moneysavingexpert.com/discussion/6599276/family-protection-trusts-why-not#latest

When unscrupulous law firms jump on this bandwagon, it becomes problematical trying to point people in the direction of safe and trustworthy advisory services.

0 -

OK to widen your options, you could try and locate a Chartered Accountancy firm listed on the ICAEW register of firms authorised to conduct probate work.beadlebunny said:OMG. This is a disaster. I Can't now even find a firm to take this on :'(

Some of these firms may well have Trust departments with STEP qualified practitioners. Tax compliance and reporting is of course their every day bread and butter ( more so compared to solicitors) but with regard to drafting of legal deeds they maybe able to refer their clients to solicitors they work with. Worth reaching out in that direction - see link below to the ICAEW search engine

https://www.icaew.com/regulation/probate-services/probate-consumer-hub/icaew-probate-register2 -

And this should show why these companies should be avoided like the plague. Many claim to be legal experts when in fact they are not. In my line of work it is amazing how many estates are considered intestate because the wills have been declared void. I and other have for many years been screaming for will writing companies to be regulated. The government were given advice after some investigations into these companies that it would be beneficial to regulate but chose not to.

With regards to the OP. Are the banks asking for you to obtain probate or are the amounts being held less than circa 15k. Just because the house does not form part of the estate, if there is a will then probate may well be needed.

Rob0 -

Hi, No one except the will drafting company has mentioned probate yet as the estate is otherwise low value... However I i think we may have found a local STEP accredited firm of solicitors who are trust and probate specialists. I cannot thank you enough for your advice and will report back on how things pan out. If anyone else reading this is in any way involved in one of these, please please think about how you will navigate all of this along with grieving for the death of the person involved and all of the other things that my poor sister as executor has had to do - funeral, bank closures, bills, death registration and certificates, not to mention the insane cost to extricate ourselves from this and use a lot of the money that mum and step-dad spent their lives working for and tried to protect for us. It is OUTRAGEOUS that these sharks are allowed to exist and scam people.6

-

Good luck with the future and I now hope you and your family can grieve the loss of the loved one in the ways each of you want to.beadlebunny said:Hi, No one except the will drafting company has mentioned probate yet as the estate is otherwise low value... However I i think we may have found a local STEP accredited firm of solicitors who are trust and probate specialists.

Rob0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards