We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Money left to children

Comments

-

Thanks for your replies. There was me thinking the money would just get locked away for a few years and that would be that. Haha0

-

No, a minor cannot make a deed of variation.silvercar said:Would a deed of variation work? Only those who potentially lose out would have to agree to it.1 -

This is in the will as well (not sure if it could make a difference). And all other people named are adults - apart from my 3 children. Thanks0

This is in the will as well (not sure if it could make a difference). And all other people named are adults - apart from my 3 children. Thanks0 -

If you have a co-operative family, then no one is likely to sue someone for breaching the exact wording of the will. With a similar clause, we just put the money in accounts in the names of the children, the parents controlled the accounts of the minors and the parents chose when to reveal to their offspring their inheritance. If the worse had happened and one of the grandchildren not survived to 21, then theoretically the other grandchildren could have asked for their share of the deceased’s inheritance. But I couldn’t imagine that anyone would have behaved like that. If a deceased grandchild had spent the money and not survived to 21, I suppose that another grandchild could have demanded their share of the money from the executors, which would have been their own parent and the parent of the deceased. I can’t imagine anyone in our family behaving like that.Keep_pedalling said:

No, a minor cannot make a deed of variation.silvercar said:Would a deed of variation work? Only those who potentially lose out would have to agree to it.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0 -

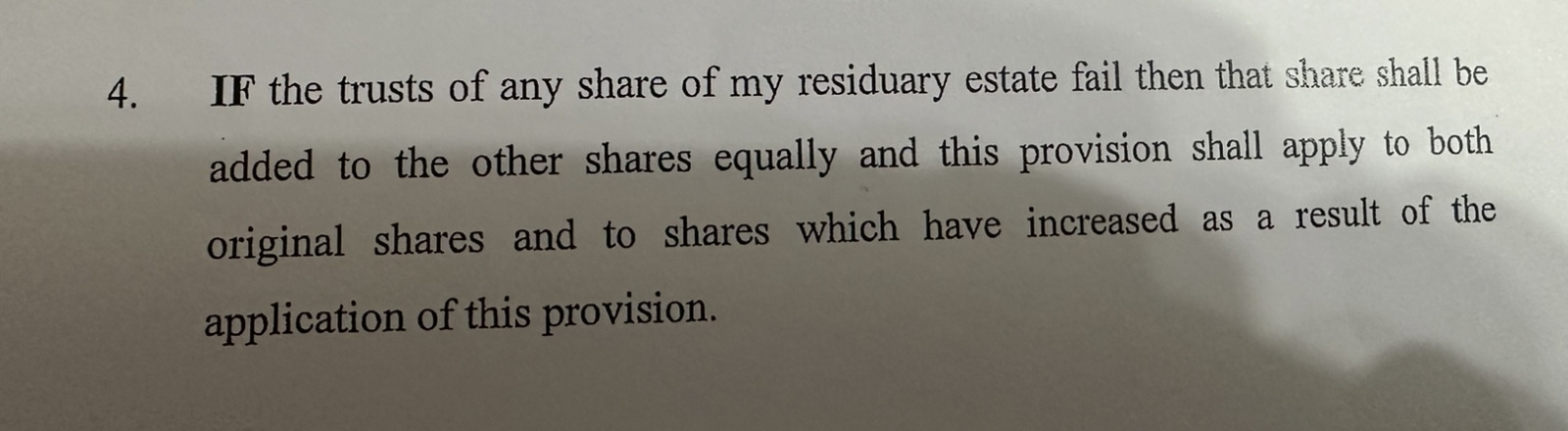

That clause does not assist since it only comes into play if all 5 children die before the age 21 vesting age, leaving no children to take that pot. As Keep_pedalling pointed out minors cannot engage in deeds of variation, which is what would be needed to eliminate the survivial contingency between them.blokeandbird said:This is in the will as well (not sure if it could make a difference). And all other people named are adults - apart from my 3 children. Thanks1 -

Sure, the executor/trustee could ignore the instructions in the will that imposed the primary responsibility on them ( rather than the children's respective parents) to preserve the trust funds until each child attains the appropriate vesting age.silvercar said:

If you have a co-operative family, then no one is likely to sue someone for breaching the exact wording of the will. With a similar clause, we just put the money in accounts in the names of the children, the parents controlled the accounts of the minors and the parents chose when to reveal to their offspring their inheritance. If the worse had happened and one of the grandchildren not survived to 21, then theoretically the other grandchildren could have asked for their share of the deceased’s inheritance. But I couldn’t imagine that anyone would have behaved like that. If a deceased grandchild had spent the money and not survived to 21, I suppose that another grandchild could have demanded their share of the money from the executors, which would have been their own parent and the parent of the deceased. I can’t imagine anyone in our family behaving like that.Keep_pedalling said:

No, a minor cannot make a deed of variation.silvercar said:Would a deed of variation work? Only those who potentially lose out would have to agree to it.

However, the additional risk in that scenario ( apart from child dying early ) is the respective parents not fulfilling the task delegated to them either by misappropriation of the child's funds for their own benefit, or making inappropriate investments and losing all or part of the money as a result.

As to the risk of misappropriation by the parent, I have seen a couple stories on this forum of that exact thing happening ( not everyone live in perfect family bliss and harmony like the Waltons). In any event if a particular child's trust fund goes pear shaped ( for whatever reason) the buck stops with the original trustee/executor both morally and legally, and the child/children concerned can (and should) pursue the original trustee for recompense.

I would suggest the larger the sums of money involved the higher the risk of undesirable outcomes if one attempts ( as primary trustee) to delegate ones duties in this casual way.1 -

So presumably a simple bank account in the children’s names but held in trust by the executors (only 1 executor is the parent - the rest are aunties/uncles) until the children are 21 is not an option.I am trying to arrange an appointment with the solicitors but just trying to go armed with possible solutions.Thanks again0

-

The parents couldn’t appropriate the funds as they were put in the names of their children.poseidon1 said:

Sure, the executor/trustee could ignore the instructions in the will that imposed the primary responsibility on them ( rather than the children's respective parents) to preserve the trust funds until each child attains the appropriate vesting age.silvercar said:

If you have a co-operative family, then no one is likely to sue someone for breaching the exact wording of the will. With a similar clause, we just put the money in accounts in the names of the children, the parents controlled the accounts of the minors and the parents chose when to reveal to their offspring their inheritance. If the worse had happened and one of the grandchildren not survived to 21, then theoretically the other grandchildren could have asked for their share of the deceased’s inheritance. But I couldn’t imagine that anyone would have behaved like that. If a deceased grandchild had spent the money and not survived to 21, I suppose that another grandchild could have demanded their share of the money from the executors, which would have been their own parent and the parent of the deceased. I can’t imagine anyone in our family behaving like that.Keep_pedalling said:

No, a minor cannot make a deed of variation.silvercar said:Would a deed of variation work? Only those who potentially lose out would have to agree to it.

However, the additional risk in that scenario ( apart from child dying early ) is the respective parents not fulfilling the task delegated to them either by misappropriation of the child's funds for their own benefit, or making inappropriate investments and losing all or part of the money as a result.

As to the risk of misappropriation by the parent, I have seen a couple stories on this forum of that exact thing happening ( not everyone live in perfect family bliss and harmony like the Waltons). In any event if a particular child's trust fund goes pear shaped ( for whatever reason) the buck stops with the original trustee/executor both morally and legally, and the child/children concerned can (and should) pursue the original trustee for recompense.

I would suggest the larger the sums of money involved the higher the risk of undesirable outcomes if one attempts ( as primary trustee) to delegate ones duties in this casual way.

It wasn’t a casual way, it was a deliberate decision to minimise the costs of administering trusts etc in order that the beneficiaries inheritance is maximised. Also, 2 of the grandchildren were already over 21, 1 over 18 and 1 over 16, so the time before a DoV could have been done was relatively short.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.1 -

Not that this helps the OP, just mentioning it for others reading along, but I do wish people would talk through their intentions about what they've done with a will before it comes to light after their death. My parents had something similarly nonsensical in their wills when leaving to Grandchildren about them getting to 25. Only one has reached that age so far, the others are still younger and these Wills if parents had died would have taken 14 years for the youngest to get to the 'magic' age.

Fortunately it came to light when I had reason to ask them about their wills and discovered it along with other barmy stuff like one of them leaving me a property they didn't own - seriously. They'd made their wills at a time of high emotional stress and just weren't thinking about what they said. Thankfully I was able to point this out and they went back to (a different) solicitor showed them what they'd put and what they wanted and the new solicitor suggested starting again but I'm well aware of what a mess could have ben left if my parents had died with their old wills in place.

2 -

There were a load of wills drafted by someone working for or with a major top 5 banks some years ago, often for relatively affluent people. These typically divided assets into different classes and left each to different people. Spouse got the named house (and shared assets), children and sometimes grandchildren then shared or were allocated different assets. So the son might get the shareholding and daughter the savings.

That house might have been sold, the shares converted to cash, or the other way round. Or a less scrupulous spouse moved everything into the shared accounts.

More recent nightmares include parents leaving their portion of the house to the children and a IPDI trust to protect their spouse, but failing to sever the tenancy.If you've have not made a mistake, you've made nothing1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards