We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Solicitor wants updated offer from broker who I have paid already

To quote from my solicitor:

"I need an updated offer to proceed. They have claimed this as being ‘ridiculous’ "

In essence, the solicitor wants to ensure legality on the sale of the house, but the brokers feel this particular change is unnecessary/ridiculous.

I'm not sure what I can do at this time. I have already paid the broker as they requested payment when I received my Mortgage Offer and I have paid them.

Please does anyone have any advice?

Comments

-

Updated in what sense? What do you mean by "ensuring legality on the sale of the house"? Do you mean the house you're purchasing or is this something connected to your sale?1

-

Super unclear post.DaffyDuck316 said:Hi, my solicitor is seeking an updated Mortgage offer from my broker but has not heard from them in two weeks.

To quote from my solicitor:

"I need an updated offer to proceed. They have claimed this as being ‘ridiculous’ "

In essence, the solicitor wants to ensure legality on the sale of the house, but the brokers feel this particular change is unnecessary/ridiculous.

I'm not sure what I can do at this time. I have already paid the broker as they requested payment when I received my Mortgage Offer and I have paid them.

Please does anyone have any advice?

What legality is the solicitor trying to ensure?

- Is this on a property you're selling and you need a redemption statement? Or on a purchase, in which case what has changed that would require an update?

What is the broker saying is ridiculous? Either something has changed or it hasn't.

1 -

When does your current mortgage offer lapse?

When is completion planned for ?0 -

To clarify a bit, I'm trying to buy a house with a Gifted Deposit and this is what I received from my solicitor and broker respectively:

-----From Solicitor:

I have never ever had this issue before, your brokers have been told by Nationwide and ourselves to rekey the application. We simply cannot proceed until the purchase price in the mortgage offer reflects the legally binding contractual documents that you are signing for the purchase.

No solicitor will ever be able to go ahead until the documents all state the same purchase price, I have spoken to multiple colleagues about this and I am left baffled by the brokers stance here.

It is completely fine that you are being gifted funds from the equity but the purchase price in the contract is £257,000 and the offer has to state the same. The sum of £257,000 will also be what is received by the seller’s solicitor on completion so we cannot change the purchase price to £265,000 unless you are paying £265,000.

---

From Broker:

I have done a concessionary purchase many of times and never had an issue at all.

The purchase price needs to be £265K with a concessionary purchase of £257K

0 -

Anyone spoken to the Nationwide. As they appear to either be not aware of this arrangement or not willing to accept it. £8k appears little more than some sleight of hand massaging by the broker. Not significant enough to be viewed as a gifted deposit possibly.DaffyDuck316 said:The purchase price needs to be £265K with a concessionary purchase of £257K

0 -

Thanks for your comment, that is a scary answer as the gifted deposit is very significant to me. But actually I did receive this earlier message from the Broker shortly before those two messages

---

From Broker:

I have spoken to the underwriter if the solicitors need the application to be changed to Genuine Bargain Price then the application would need to be re submitted.The best thing to do is confirm to the solicitors that the purchase price is £265K and the landlord is gifting you the equity of 8K like we originally discussed right at the very start. This will be the quickest way to the get the completion date.1 -

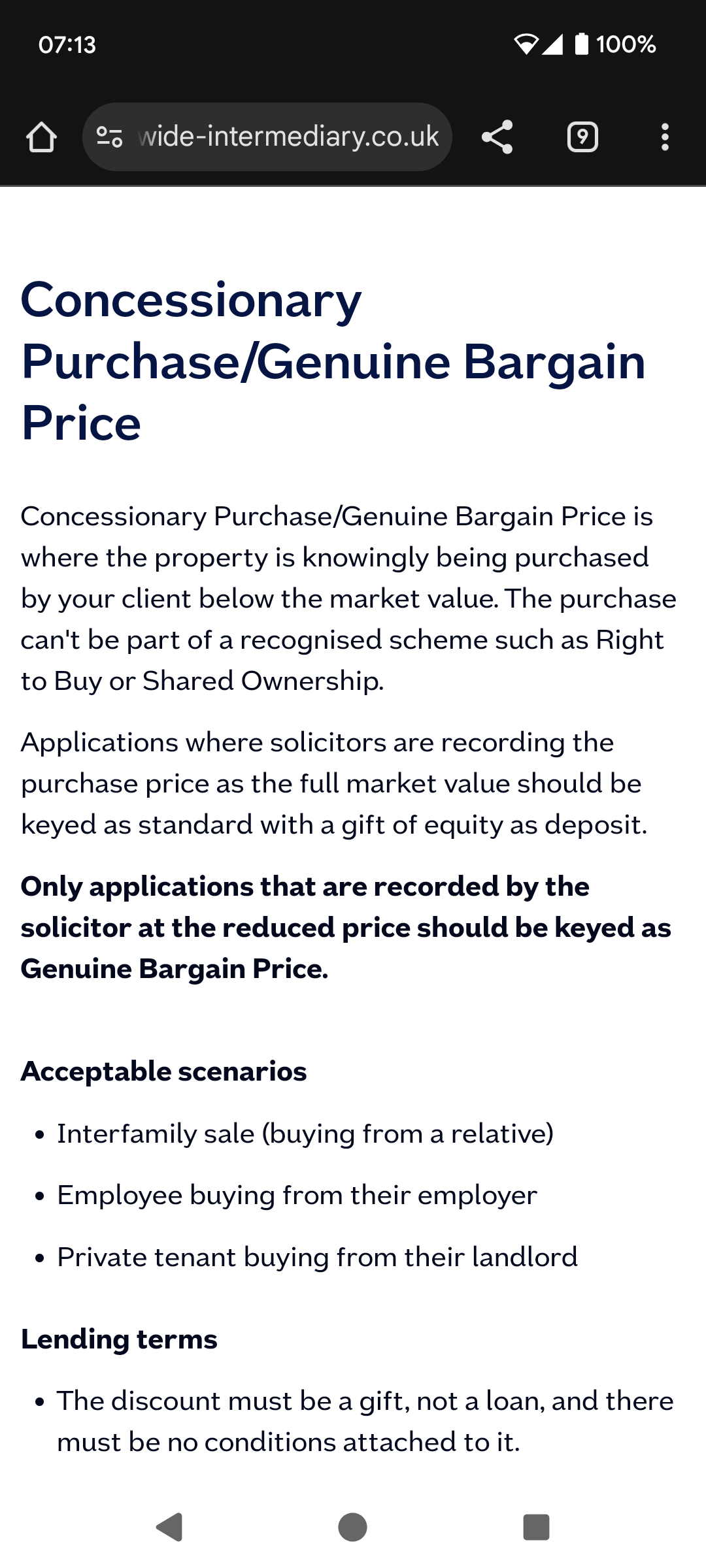

This is straight from Nationwide lending criteria.

I'm wondering if the bit in bold applies?

https://www.nationwide-intermediary.co.uk/lending-criteria/purchase-types

0 -

Thank you so much, that was very insightful, I wish I had thought to do that myself.

I have just a message to my solicitor as follows...

"This is straight from Nationwide lending criteria.---Applications where solicitors are recording the purchase price as the full market value should be keyed as standard with a gift of equity as deposit.Only applications that are recorded by the solicitor at the reduced price should be keyed as Genuine Bargain Price.---This is from you:---It is completely fine that you are being gifted funds from the equity but the purchase price in the contract is £257,000 and the offer has to state the same. The sum of £257,000 will also be what is received by the seller’s solicitor on completion so we cannot change the purchase price to £265,000 unless you are paying £265,000.---In my head, these two statements from Nationwide and yourself are conflictual. Should we not be recording the full market value as the purchase price?

"

Does anyone have any thoughts on this, was that the right thing to say?1 -

DaffyDuck316 said:

Does anyone have any thoughts on this, was that the right thing to say?

The problem seems to be that there are 2 ways of dealing with the mortgage for this...- 1) A sale at full market value of £265k - where the seller is gifting you a deposit of £8k

- 2) A sale at a 'Genuine Bargain Price' (or 'Concessionary Price') of £257k - with no gifted deposit

Your broker has treated it as option 1...

... but your solicitor is unhappy with that, and wants it treated as option 2.

And your broker is saying that switching from option 1 to option 2 will mean resubmitting your mortgage application.

(TBH, I've no idea whether your solicitor is wrong to reject option 1.)

Just to make sure there is no confusion - has your seller signed a "gifted deposit declaration" letter - which you have passed to your solicitor?

1 -

Thanks eddddy,

That does seem to be the case indeed. But I don't understand why the solicitor would reject option 1, she says

"we cannot change the purchase price to £265,000 unless you are paying £265,000."

But surely you could say the same thing to anyone who has ever applied for a Gifted Deposit, there is always going to be a void of money. I'll ask her this line of questioning as she is still adamant the offer needs to match her contract and not the contract needs to match her offer.

I do have a Gifted deposit declaration, thankfully.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards