We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Is the real average global equity return only 4.87%?

Comments

-

And like I said I can withdraw 100% of the isa without paying any tax but a pension you pay tax after the first 25% or whatever it is.Pension wrapper still beats ISA wrapper from a tax point of view. So, you are missing out financially if you do not use the pension.

It is all about balance. Leave enough for the short term, enough for the medium term and enough for the long term. Then as you get closer to retirement, you can transfer the ISA money into the pension.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

It's important to make sure you are using the average compounding return and not just the arithmetic mean. I think the OP's linked site is doing that. Also when people look at their portfolio they usually look at it just as it is right now, they don't reduce it to account for inflation. Finally a critical factor in portfolio growth is the amount you invest and also you employer puts in. Hopefully this will increase over the years. If people start early and contribute a larger amounts each year and get average returns it's perfectly possible to become a millionaire. Of course for many people today their low pay and lack of employment security do make long term investing very difficult.And so we beat on, boats against the current, borne back ceaselessly into the past.0

-

OK, what you meant was "not suitable for my personal investing requirements". It seems strange you were talking about FIRE so much at first, though.[Deleted User] said:

I think you misunderstood what I meant.EthicsGradient said:

Few people think "investing for your pension" is "incredibly risky". It is, after all, the point of FIRE, which is what you're talking about. Investing over a long period is less risky than a short one. And you'll still come out ahead, as long as you withdraw less than your salary was when you contributed.[Deleted User] said:

True but this is incredibly risky as you're effectively locking that money away until 55, soon to be 57 and probably 60+ by the time I retire. Also you pay tax if you withdraw over a certain amount in 1 year or whatever.leosayer said:

For example, instead of investing via an ISA, salary sacrificing into a pension can mean you pay much less tax on your income.

At least with a stocks and shares isa I have access anytime I need it and it's tax free anyway.

Currently 95% of all the money I have is in a global index fund in a stocks and shares ISA. The other 5% is in an emergency cash isa account. I can withdraw from both at anytime without penalty and have the money in my bank account within 2 days. That to me screams safety.

However if 95% of my money was locked away in a private pension that I wasn't allowed to withdraw from until the age of 57+, that would give me huge anxiety because if I ever needed that money but couldn't access it I'd be screwed. Sure I'd have some money in my emergency cash isa account but if that run out I'd literally have no money.

Besides my company only matches my contribution up to 7.5% so if I contributed 20% they'd still only contribute 7.5%. Also I'm not a high earner so the tax I pay is the lowest amount anyway.

And like I said I can withdraw 100% of the isa without paying any tax but a pension you pay tax after the first 25% or whatever it is.

I hope you are taking advantage of the matching 7.5%, anyway - that's free money. leosayer mentioned salary sacrifice, which is when you employer contributes to the pension outside of your salary; this means they and you don't pay National Insurance on the contribution - another saving for you.0 -

Of course I'm taking the full 7.5% because like you say, it's free money.EthicsGradient said:

OK, what you meant was "not suitable for my personal investing requirements". It seems strange you were talking about FIRE so much at first, though.[Deleted User] said:

I think you misunderstood what I meant.EthicsGradient said:

Few people think "investing for your pension" is "incredibly risky". It is, after all, the point of FIRE, which is what you're talking about. Investing over a long period is less risky than a short one. And you'll still come out ahead, as long as you withdraw less than your salary was when you contributed.[Deleted User] said:

True but this is incredibly risky as you're effectively locking that money away until 55, soon to be 57 and probably 60+ by the time I retire. Also you pay tax if you withdraw over a certain amount in 1 year or whatever.leosayer said:

For example, instead of investing via an ISA, salary sacrificing into a pension can mean you pay much less tax on your income.

At least with a stocks and shares isa I have access anytime I need it and it's tax free anyway.

Currently 95% of all the money I have is in a global index fund in a stocks and shares ISA. The other 5% is in an emergency cash isa account. I can withdraw from both at anytime without penalty and have the money in my bank account within 2 days. That to me screams safety.

However if 95% of my money was locked away in a private pension that I wasn't allowed to withdraw from until the age of 57+, that would give me huge anxiety because if I ever needed that money but couldn't access it I'd be screwed. Sure I'd have some money in my emergency cash isa account but if that run out I'd literally have no money.

Besides my company only matches my contribution up to 7.5% so if I contributed 20% they'd still only contribute 7.5%. Also I'm not a high earner so the tax I pay is the lowest amount anyway.

And like I said I can withdraw 100% of the isa without paying any tax but a pension you pay tax after the first 25% or whatever it is.

I hope you are taking advantage of the matching 7.5%, anyway - that's free money. leosayer mentioned salary sacrifice, which is when you employer contributes to the pension outside of your salary; this means they and you don't pay National Insurance on the contribution - another saving for you.

But now you've got me thinking, I already have a pretty sizeable amount in my stocks and shares ISA that would cover me for multiple years of unemployment if worst came to worst.

What I could do is instead of saving 40% of my income post tax into the S&S ISA, I could change the amount I save into the pension from 7.5% to 60% for a few years to bump up the pension as it would be before tax so I'd pay no income tax at all (according to mse calculator).

Basically this was my plan the entire time.

Do the 7.5% matched pension

Aggressively save into S&S ISA

Retire at 55.

Withdraw 70% from the S&S ISA to buy a home

Live off a 4% withdrawal rate of the other 30% until I get access to my private pension.

Live off a 6% withdrawal rate until I get access to my state pension. (assuming it still exists by that point).

Nothing is set in stone but this is generally along the lines of what my plans are. The reason I didn't want to over contribute to the pension is because if I withdraw 70% of it in 1 lump sum to buy a home I would be taxed heavily. But with a S&S ISA there is no withdrawal tax.1 -

[Deleted User] said:

Of course I'm taking the full 7.5% because like you say, it's free money.EthicsGradient said:

OK, what you meant was "not suitable for my personal investing requirements". It seems strange you were talking about FIRE so much at first, though.[Deleted User] said:

I think you misunderstood what I meant.EthicsGradient said:

Few people think "investing for your pension" is "incredibly risky". It is, after all, the point of FIRE, which is what you're talking about. Investing over a long period is less risky than a short one. And you'll still come out ahead, as long as you withdraw less than your salary was when you contributed.[Deleted User] said:

True but this is incredibly risky as you're effectively locking that money away until 55, soon to be 57 and probably 60+ by the time I retire. Also you pay tax if you withdraw over a certain amount in 1 year or whatever.leosayer said:

For example, instead of investing via an ISA, salary sacrificing into a pension can mean you pay much less tax on your income.

At least with a stocks and shares isa I have access anytime I need it and it's tax free anyway.

Currently 95% of all the money I have is in a global index fund in a stocks and shares ISA. The other 5% is in an emergency cash isa account. I can withdraw from both at anytime without penalty and have the money in my bank account within 2 days. That to me screams safety.

However if 95% of my money was locked away in a private pension that I wasn't allowed to withdraw from until the age of 57+, that would give me huge anxiety because if I ever needed that money but couldn't access it I'd be screwed. Sure I'd have some money in my emergency cash isa account but if that run out I'd literally have no money.

Besides my company only matches my contribution up to 7.5% so if I contributed 20% they'd still only contribute 7.5%. Also I'm not a high earner so the tax I pay is the lowest amount anyway.

And like I said I can withdraw 100% of the isa without paying any tax but a pension you pay tax after the first 25% or whatever it is.

I hope you are taking advantage of the matching 7.5%, anyway - that's free money. leosayer mentioned salary sacrifice, which is when you employer contributes to the pension outside of your salary; this means they and you don't pay National Insurance on the contribution - another saving for you.

But now you've got me thinking, I already have a pretty sizeable amount in my stocks and shares ISA that would cover me for multiple years of unemployment if worst came to worst.

What I could do is instead of saving 40% of my income post tax into the S&S ISA, I could change the amount I save into the pension from 7.5% to 60% for a few years to bump up the pension as it would be before tax so I'd pay no income tax at all (according to mse calculator).

Basically this was my plan the entire time.

Do the 7.5% matched pension

Aggressively save into S&S ISA

Retire at 55.

Withdraw 70% from the S&S ISA to buy a home

Live off a 4% withdrawal rate of the other 30% until I get access to my private pension.

Live off a 6% withdrawal rate until I get access to my state pension. (assuming it still exists by that point).

Nothing is set in stone but this is generally along the lines of what my plans are. The reason I didn't want to over contribute to the pension is because if I withdraw 70% of it in 1 lump sum to buy a home I would be taxed heavily. But with a S&S ISA there is no withdrawal tax.

If you think to retire at 55, so what is the problem to maximise the pension contributions? Have you thought about, that the tax relief money will be working for you to make money ( as more you invest, as more you will expect to make ) and instead of staying in government's pocket, it will be in yours and work for you?2 -

Contributing to tax-deferred and after-tax tax advantaged accounts gives you flexibility in account access and also to plan your taxes. I've always had money growing in DC pensions, tax free investments, general investment accounts and also in real estate while seeking to have a good base of guaranteed income from SP and DB benefits. Diversity is a good thing, so don't over concentrate in any one area. I can assure you that it is possible to end up with 7 figure portfolios and to retire early, but it takes some common sense, frugality and perseverance.[Deleted User] said:

Of course I'm taking the full 7.5% because like you say, it's free money.EthicsGradient said:

OK, what you meant was "not suitable for my personal investing requirements". It seems strange you were talking about FIRE so much at first, though.[Deleted User] said:

I think you misunderstood what I meant.EthicsGradient said:

Few people think "investing for your pension" is "incredibly risky". It is, after all, the point of FIRE, which is what you're talking about. Investing over a long period is less risky than a short one. And you'll still come out ahead, as long as you withdraw less than your salary was when you contributed.[Deleted User] said:

True but this is incredibly risky as you're effectively locking that money away until 55, soon to be 57 and probably 60+ by the time I retire. Also you pay tax if you withdraw over a certain amount in 1 year or whatever.leosayer said:

For example, instead of investing via an ISA, salary sacrificing into a pension can mean you pay much less tax on your income.

At least with a stocks and shares isa I have access anytime I need it and it's tax free anyway.

Currently 95% of all the money I have is in a global index fund in a stocks and shares ISA. The other 5% is in an emergency cash isa account. I can withdraw from both at anytime without penalty and have the money in my bank account within 2 days. That to me screams safety.

However if 95% of my money was locked away in a private pension that I wasn't allowed to withdraw from until the age of 57+, that would give me huge anxiety because if I ever needed that money but couldn't access it I'd be screwed. Sure I'd have some money in my emergency cash isa account but if that run out I'd literally have no money.

Besides my company only matches my contribution up to 7.5% so if I contributed 20% they'd still only contribute 7.5%. Also I'm not a high earner so the tax I pay is the lowest amount anyway.

And like I said I can withdraw 100% of the isa without paying any tax but a pension you pay tax after the first 25% or whatever it is.

I hope you are taking advantage of the matching 7.5%, anyway - that's free money. leosayer mentioned salary sacrifice, which is when you employer contributes to the pension outside of your salary; this means they and you don't pay National Insurance on the contribution - another saving for you.

But now you've got me thinking, I already have a pretty sizeable amount in my stocks and shares ISA that would cover me for multiple years of unemployment if worst came to worst.

What I could do is instead of saving 40% of my income post tax into the S&S ISA, I could change the amount I save into the pension from 7.5% to 60% for a few years to bump up the pension as it would be before tax so I'd pay no income tax at all (according to mse calculator).

Basically this was my plan the entire time.

Do the 7.5% matched pension

Aggressively save into S&S ISA

Retire at 55.

Withdraw 70% from the S&S ISA to buy a home

Live off a 4% withdrawal rate of the other 30% until I get access to my private pension.

Live off a 6% withdrawal rate until I get access to my state pension. (assuming it still exists by that point).

Nothing is set in stone but this is generally along the lines of what my plans are. The reason I didn't want to over contribute to the pension is because if I withdraw 70% of it in 1 lump sum to buy a home I would be taxed heavily. But with a S&S ISA there is no withdrawal tax.And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

While using average returns is a good start (but they completely depend on the start and end point of the period in use) - the 26 years of the GBP data in your link is not really sufficient to provide a meaningful average (even the 46 years for the USD version is not really good enough).[Deleted User] said:I'm looking at this fund https://curvo.eu/backtest/en/market-index/msci-world?currency=gbp and it shows the average annual return is only 7.69%. But if we deduct the average UK inflation rate of 2.82% that gives a real return of a measly 4.87%. Why is it so low?

But if you switch currencies to USD it shows 9.9%. And if you deduct the average US inflation rate of 3.8% you get a real return of 6.1%

I'm not really sure how people are becoming millionaires through index funds when the average return is so low. Even if you invested £500 a month for 35 years at a 4.87% compounded interest rate you'd only have £626,000 at the end of it.

I've been reading up about this whole "FIRE" investing thing but it seems like none of the youtubers talking about it are taking the inflation rate into account. They're all using pre inflation returns. Which if you did would give you a cool £1m after 33 years.

So there's a discrepancy of like 400 grand between pre inflation returns and post inflation returns...

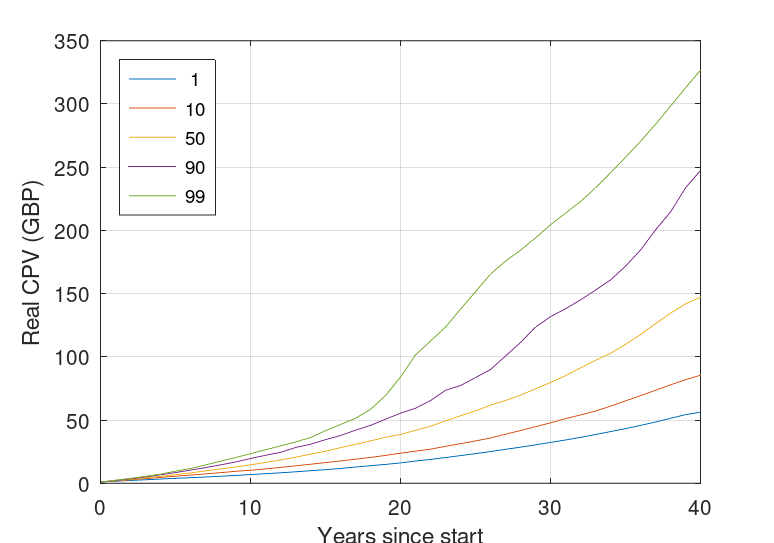

The following graph shows the real portfolio value as a function of time assuming an annual investment of an inflation linked £1 for different historical percentiles (1st percentile is close to the worst case, 50th percentile is the median, and 99th percentile is close to the best case)*.

While the exact numbers will depend on the portfolio, the key thing to take away are that

1) the amount accumulated varied considered from (after 40 years) just over 50 real pounds to over 300 real pounds (i.e., a factor of 6 between the best and worst cases)

2) In the worst case, the amount accumulated was, in real terms, only a bit more than the contributions made (40 real pounds after 40 years).

Which path future accumulation periods will follow is impossible to predict - hopefully it will not be close to the worst historical case.

* 40% UK equities, 40% US equities, 10% UK long maturity bonds, and 10% UK cash. Asset returns and inflation for 1872 onwards from macrohistory.net

1 -

* 40% UK equities, 40% US equities, 10% UK long maturity bonds, and 10% UK cash. Asset returns and inflation for 1872 onwards from macrohistory.net

With hindsight it's easy to say what people could/should have done. Totally white washing Japan (for example) from Investment History fails to reflect reality.2 -

I think the point is to show the historical variability of returns rather than the effects of geographical asset allocation. But, yes, asset allocation is a factor in returns and if you happen to be Japanese and lived through the Lost Decade there will have been a lot of pain.Hoenir said:* 40% UK equities, 40% US equities, 10% UK long maturity bonds, and 10% UK cash. Asset returns and inflation for 1872 onwards from macrohistory.net

With hindsight it's easy to say what people could/should have done. Totally white washing Japan (for example) from Investment History fails to reflect reality.And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

Bostonerimus1 said:

I think the point is to show the historical variability of returns rather than the effects of geographical asset allocation. But, yes, asset allocation is a factor in returns and if you happen to be Japanese and lived through the Lost Decade there will have been a lot of pain.Hoenir said:* 40% UK equities, 40% US equities, 10% UK long maturity bonds, and 10% UK cash. Asset returns and inflation for 1872 onwards from macrohistory.net

With hindsight it's easy to say what people could/should have done. Totally white washing Japan (for example) from Investment History fails to reflect reality.Yes, it was supposed to illustrative of the variability in outcomes - I even said "While the exact numbers will depend on the portfolio".

The effect of the Japanese stock market (it formed about 35% of the global market in 1987) on the world market in 1990 can be seen using the https://curvo.eu/backtest/en/market-index/msci-world?currency=usd where there was fall of 17% in that year. From an accumulator’s point of view, that would have been a positive (cheap equities!), so the detailed numbers would have changed slightly but not by a factor of six which is the difference between the best and worst cases (in other words, small changes in the construction of the portfolio will generally make small changes to the spread of outcomes).A recent article by William Bernstein (https://www.advisorperspectives.com/articles/2025/02/10/merton-share-why-dont-use-retirement-calculators – scroll down to the section labelled ‘retirement calculators’ onwards for the most relevant parts) succinctly expresses a view that I can largely agree with.

For the OP, the table in the ‘start on the back of the envelope’ section of Bernstein's article illustrates an answer to your implicit question of how much should you save (for a shorter period of accumulation than 40 years, the monthly figures will be greater, real $ can be replaced by real £). Since the historical average returns of whatever index do not give much more than a vague indication of future returns, the practical answer is probably to save as much as you can for the future without making your present life miserable and review this every few years. I also note that https://tpawplanner.com (excel versions are available athttps://www.bogleheads.org/wiki/Total_portfolio_allocation_and_withdrawal) might be of interest.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards