We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Almost nobody in my workplace invests in the stock market for their retirement, it's insane.

Comments

-

They aren't below (or on, or just above) the bread line.AmityNeon said:Altior said:Someone can rent a room in a shared property, and live a decent life, not on the bread line. It's a different topic (altho I concede, the 'bread line' theme is already a deviation from the thread topic!).

Of course people can rent in shared accommodation, live a decent life and save/invest for a healthy retirement. Childless likely.

A lot of it is about choices, compromises and sacrifices (not everything, a lot). I was born and raised in London, I soon figured if I stayed there I would be effectively working just to live. So I chose to live somewhere that was a lot cheaper, and wouldn't be working just to pay the mortgage or the rent, with little disposable income.

I still stayed in the south east, there are even much more cost effective places to live in the UK, which I may consider when I stop work well before NRA (an opportunity that has opened up to me as I chose not to live in the city where I was born).

It's beyond me really, but plenty of people opt to struggle and stay (or even move into!) incredibly expensive London, and be a slave to the bank/landlord during their working life. Up to them obviously (choices/compromises/sacrifices), but they can't then legitimately complain that they have it worse than previous generations, in my view. Same as I couldn't complain about being isolated, and having to travel 40 miles to visit my friends in London.

3 -

Altior said:AmityNeon said:Altior said:

Someone can rent a room in a shared property, and live a decent life, not on the bread line. It's a different topic (altho I concede, the 'bread line' theme is already a deviation from the thread topic!).

Of course people can rent in shared accommodation, live a decent life and save/invest for a healthy retirement. Childless likely.

They aren't below (or on, or just above) the bread line.

A decent life and a healthy retirement is obviously not anywhere close to the breadline.

2 -

£10! £10!! I used to dreeeam about earning £10! My paper round when I was in school (1966), earned me £1, and I thought that was good. Mind you, I only had to walk 2 miles to school! 😏Altior said:

Suspect we're about the same age. My first earning job was £10 a week for 7 days a week paper round, 5 of them before taking a 5 mile trip to school (bussing and walking). First proper p/t job was £3.30 an hour, I seem to recall some tax and NI was deducted off that.QrizB said:

In 1991, straight out of Compton sorry uni and before minimum wage legislation, I was pleased to get a casual job on £3.50 an hour. Inflated to today, that would be £7.90. current minimum wage is 50% higher than that so I'd suggest that the low-waged are substantially better off today than they were then.Altior said:Not particularly directed at the poster I quoted, but unfortunately we do have people/posters who seem very often to try and make out it's 'so bad' right now, when it actually isn't. It really isn't, in my view. If it is, however, let's see some tangible evidence.Altior said:RL is our employer pension provider, we regularly get RL reps to come in and deliver pension presentations, with AMA time at the end. I work in a fin tech business, with an employee profile that is tilted to the young. Most colleagues have at least a basic grasp of accounting and finance, to get through the door. Almost everyone zones out, so many young people just don't care about pensions.

Our provider is Scottish Widows. They provide quarterly pensions talks via Teams and it's quite noticeable that most of the self-selecting audience are from the mature end of the age range.Having said that, a few of the young uns in the office were talking about risking a few hundred on day trading, so us old fogeys pointed out that they had much bigger stock market investments in their pensions. That got them thinking about their investment strategies and at least a few of them decided to increase their contributions from the minimum. So ther might be hope for them yet!2 -

Well thank god I can at least influence my own children's financial education because there are some reality checks down the line from anyone that thinks the state pension will really give them a decent retirement.[Deleted User] said:

Nope. If you don't like it tough.artyboy said:

Please, please, PLEASE tell me that is sarcasm.[Deleted User] said:

Personally I don't classify investing as being 'financially responsible'. Far from it in fact, its gambling with your hard earned money, in fact its worse. Its letting some other pleb gamble with your hard earned money.[Deleted User] said:I work in a slightly below average pay job and I've probably spoken to about 20 out of the 30 colleagues about investing, just to gauge how common it is among "regular" people.

And literally not one person I spoke to said they invest in the stock market, even when I asked about the workplace pension, about half of them said they opted out because "money now is better than money when I'm dead" which is just silly because the average life expectancy in the UK is 82... So what are they going to do to get by until they die? The state pension only? Yeah good luck with that.

One guy I spoke to who was in his mid 20's said he saves some money but in a savings account with a bank. I asked him what the interest rate was and he didn't even know... So probably like 1.5% if it's a regular high street bank which I suspect it is. I didn't have the heart to tell him he's actually losing money to inflation, not saving it...

It just seems like not enough people are being financially responsible and taking steps to ensure they have a comfortable retirement. I absolutely promise you when you're 65 and freezing cold in your home because you can't afford to put the heating on, eating from food banks and having no money to do anything, you'll totally regret not being frugal and investing for your future.

I think too many people live in the here and now without a seconds thought for the future. I understand that money is tight for many people but surely you can put a little bit away each month to supplement your pension when you're old?

I think financial education should be mandatory in schools with students being shown videos of old people living in poverty because they didn't invest in their retirements.

Saving yes, investing no.

You could lose not gain. Not just in comparison to inflation but proper loss.

And life is for living, especially when you're young.

Good for them I say.

Smh.6 -

A major factor today that wasn't around for most in the 1960/70's is inheritance. I think a lot of younger people know they have something significant coming their way and live accordingly.4

-

Maybe a bit less significant if the planned IHT raid goes ahead...subjecttocontract said:A major factor today that wasn't around for most in the 1960/70's is inheritance. I think a lot of younger people know they have something significant coming their way and live accordingly.2 -

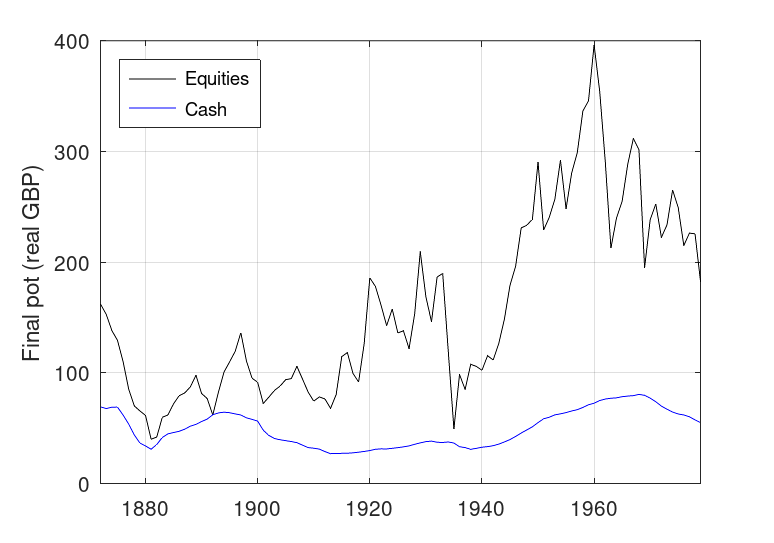

While no-one can predict the future, historically, those investing in the UK stock market for long enough have virtually always done better than those saving. For example, the following graph shows the amount of money (in real terms) accumulated after investing or saving £1 per year (inflation linked) for 40 years* for different starting years.[Deleted User] said:

Personally I don't classify investing as being 'financially responsible'. Far from it in fact, its gambling with your hard earned money, in fact its worse. Its letting some other pleb gamble with your hard earned money.[Deleted User] said:I work in a slightly below average pay job and I've probably spoken to about 20 out of the 30 colleagues about investing, just to gauge how common it is among "regular" people.

And literally not one person I spoke to said they invest in the stock market, even when I asked about the workplace pension, about half of them said they opted out because "money now is better than money when I'm dead" which is just silly because the average life expectancy in the UK is 82... So what are they going to do to get by until they die? The state pension only? Yeah good luck with that.

One guy I spoke to who was in his mid 20's said he saves some money but in a savings account with a bank. I asked him what the interest rate was and he didn't even know... So probably like 1.5% if it's a regular high street bank which I suspect it is. I didn't have the heart to tell him he's actually losing money to inflation, not saving it...

It just seems like not enough people are being financially responsible and taking steps to ensure they have a comfortable retirement. I absolutely promise you when you're 65 and freezing cold in your home because you can't afford to put the heating on, eating from food banks and having no money to do anything, you'll totally regret not being frugal and investing for your future.

I think too many people live in the here and now without a seconds thought for the future. I understand that money is tight for many people but surely you can put a little bit away each month to supplement your pension when you're old?

I think financial education should be mandatory in schools with students being shown videos of old people living in poverty because they didn't invest in their retirements.

Saving yes, investing no.

You could lose not gain. Not just in comparison to inflation but proper loss.

And life is for living, especially when you're young.

Good for them I say.

While there were several occasions late in the 19th century and one just prior to WWII where the final pot value was similar for both cash and equities, for the vast majority of cases those who invested in equities ended up with more money after 40 years than those who saved in cash. While I've not shown them, for shorter periods (e.g., 20 years) there were a few more periods where cash and equities ended up with pots of comparable size, but still not that many. So if it is gambling, the odds in the past have definitely favoured the stock market!

I note that holding a combination of equities, bonds, and cash (e.g., the latter as part of an emergency fund) is probably more common on these boards than solely holding equities.

* Return data for UK equities and UK 3-month bills (similar to easy access cash accounts) and inflation from macrohistory.net.

5 -

Well it is gambling in so much as there is market risk. Inflation is the risk to cash.

A cash pound saved is still a pound. But a pound in 10 years will most likely not buy as much as a pound today. If one takes some risk with that pound there are many outcomes, it could be zero but has no upper limit. There are many ways to minimise that zero outcome and will help hold the purchasing power. Of course money at risk is also afflicted by inflation but it has the chance to outstrip it. That's never the case with cash.

It seems a shame that this knowledge doesn't spread to more poeple. Those without much money can;t accumulate more, this lack of understanding keeps them poor and those with a good income it can impede them maintaining their wealth if its all in cash.

The sneakyspectator has encountered not just that opinion but worse not only do people not want the market risk for financial security in a life after work they would rather evade it by spending today. Deffered gratification is not an available option prefering to spend rather than make provisions for later. Like the kids in the marshmallow experiment. Not a good role model for your financial planning.

4 -

Go back a couple of generations on both sides of my family and you'd find something similar (albeit perhaps not to that extreme). Hiding from the milkman on a Friday morning was a common thing.(Removed by Forum Team)

So I'm hardly part of the landed gentry, just made a few good and/or fortunate decisions with my life (and the odd disastrous one) and worked my backside off along the way. Trying not to step on anyone, and paying a shedload of tax in the process. It's not exactly rocket science, but I'll still always find myself on the wrong side of the politics of envy for daring to rise above my station and actually plan for a comfortable future.Heigh ho.

(And yes, I do have to echo Eskbanker, just a little TMI!)0 -

I could have said that myself. I came from a one parent family and looking back, I can now appreciate how tight our finances were - something I did not understand at the time. But later had one or two moments on the road to Damascus and invested a much as I could and treated people as I would want to be treated. I’m very fortunate in having a loving family also.artyboy said:

Go back a couple of generations on both sides of my family and you'd find something similar (albeit perhaps not to that extreme). Hiding from the milkman on a Friday morning was a common thing.(Removed by Forum Team)

So I'm hardly part of the landed gentry, just made a few good and/or fortunate decisions with my life (and the odd disastrous one) and worked my backside off along the way. Trying not to step on anyone, and paying a shedload of tax in the process. It's not exactly rocket science, but I'll still always find myself on the wrong side of the politics of envy for daring to rise above my station and actually plan for a comfortable future.Heigh ho.

(And yes, I do have to echo Eskbanker, just a little TMI!)2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards