We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Teetering on the brink

Comments

-

Depends what interest rates Fluid and Aqua card are at. If you can pay it off an interest bearing account, that is what I would do.

Even better if the facility to re use the card remains, if unfortunately

your situation gets worse.2 -

Congratulations! That's amazing news 👏

I agree with ellenvan. If one of those cards can be paid off you'll still have a couple of hundred to keep as an emergency fund, or pay down something else to help increase the chance of balance transfers.MFW -

House purchase £62500

Original mortgage balance 28/08/2014 £52850Original MF date: 2049:eek: Aiming for: 2025

Balance 27/07/2016 £49990

Balance 08/07/2017 £47999

Balance 30/07/2018 £44500

Balance 01/08/2019 £40700

Balance 03/09/2020 £37619

Balance 30/09/2021 £33983

Balance 18/01/2023 £28940

Balance 06/10/2024 £22168

Balance 08/10/2025 £18417

Mortgage free 09/10/2025!! Mortgage paid off in 11 years, 1 month, 11 days 🥳

2 -

@EatingBeans sorry to hear you're feeling so poorly

Don't get disheartened on the weight either, I know mine can vary by a kg overnight at times, you know you can shift it so when you have capacity to do so, you can.

Agree though on the SL repayment- get rid of one of the smaller cards if they're not interest free, one less thing to juggle every month.July 2024 £12,150 July 26 Hfax £4,384, Bclycrd £3,196, Very £102 Total £7,6822 -

All 3 options sound good, great advice above.

You have enough 'extra' to completely clear one of fluid or aqua. Pros - one less thing to think about and manage. Cons may not actually free up much day to day cash

You could pay it off your bigger account and hope to get another 0% offer. Pros - I think that was what you've been trying to do so it would be sticking to the plan. Cons - may not result in an offer, may not free up much day to day.

You could get van fixed. Pros - may not cost the whole 1300 so you'd have extra to use elsewhere, van would be fixed which you need to do at some point so will need to find that money. Cons - none that I can see

You could save it all. Pros - money there hopefully gaining interest, good peace of mind knowing you have some spare cash for anything that crops up, its unexpected money so good to do something that you can instantly see gets you ahead of where you were. Cons - you are going to need it to fix van at some point, its not such a huge amount that the interest gained will be hugely mathematically significant, to gain the best amount of interest it needs to be there for a while.

If it was me, I'd go for van first as that needs done. Whatever is left split between saving and paying something down in your already decided priority. Not as satisfying as completely paying something off but maybe spreads the benefit?

Back in our early days of trying to be more organised whenever we got 'extra' money we settled on a strategy that meant we always knew what to do with it. Whether it was birthday/Xmas money, overtime (very rare we got an opportunity to work overtime), unexpected gift from the in laws etc. Percentages went on each of our priorities- sometimes that was 50% house (repairs or something we needed) 30% savings, 10% to each of us. Other years it was 50/25/25 you get the idea. So, following your plan, any left over from the van fix you could allocate 50% savings, 50% debt. Or 30% future presents for daughters that you are committed to, 30% savings, 30% debt, 10% general income? We just found it easier to know we had a system funding our priorities as we had decided them.

Dxxx22: 3🏅 4⭐ 23: 5🏅 6 ⭐ 24 1🏅 2⭐ 25 🏅 🥈2⭐ 26 🥈 Never save something for a special occasion. Every day is a special occasion. The diff between what you were yesterday and what you'll be tomorrow is what you do today Well organised clutter is still clutter - Joshua Becker If youre not already using a thing you won't start using it more by shoving it in a cupboard- AJMoney The barrier standing between you & what youre truly capable of isnt lack of info, ideas or techniques. The secret is 'do it'5 -

Do you have any sort of emergency fund at the moment? I'd have a min of £500 set aside for the unexpected as no matter how much we try on this journey things WILL go wrong whether its a new tyre, vet visit, boiler call out etc. Some people use a CC for an EF but i tend to follow the Dave Ramsey method of always having actual cash for an EF so that i can focus on reducing the debt and not adding to it.

Hope you feel better soon and get the pain under control, you've not had a good year with it x3 -

Thanks for all your thoughts, it is really useful to have different perspectives.I think I am going to fix the van first otherwise that will become an emergency come MOT time. Depending on how much that comes to I may be naughty and see if I can get a new tent so that dd2 and I can continue our cheap getaway adventures next year before she leaves for uni. I may also pinch a couple of hundred pounds out of it to give the girl’s a Christmas this year since it will be our last one before they start leaving home. 😢 Whatever is left will go off the Fluid credit card as that has the highest interest rate.Now, I know that is probably not the most pro debt busting use of the cash but the way I see it I wasn’t aware that I was even going to get this cash so it wont hurt too much to spend some on the girls. I know I will be very tempted to spend more than I can afford anyway given the short amount of time I have left with them, at least this way I have a fixed budget - at the very max don’t spend more than the extra I am receiving (after the van is fixed).End ofSep-25Oct-25

Brother 7,800.00 7,650.00 Overdraft owed 0.00 0.00 MBNA CC 11,481.53 11,504.06 Barclaycard CC 9,662.17 9,558.10 Fluid CC 1,046.44 1,036.29 NatWest CC 11,705.36 11,693.03 Aqua 1,127.94 1,107.94

Total debt

42,823.44

42,549.42Paid off in the month 211.33 274.02

Interested in my diary? Check out...

https://forums.moneysavingexpert.com/discussion/6580468/teetering-on-the-brink/p13 -

You might be able to get cheap camping gear at this time of year, as out of season. Maybe think about incorporating into Christmas presents anything they may need for uni?

Any amount paid off the fluid card will be a bonus and save money on interest.

How's the £5 challenge going, or is that on hold until you are feeling better1 -

Two other random pieces of good news today.1, I managed to get up yesterday morning, stay properly awake all day, did a bit of light cleaning, managed to put the bin out all by myself (well wrapped up of course), and still felt like a human being at the end of it. The pain was still there but no where near as bad so it seems like the tablets are starting to work! 🎉 dd1 will be glad because yesterday I sent her to the pharmacy for the third time this week and to the post office to post two more items for me. Fingers crossed the next ones I will do myself. 🤞

2, Little dog let me clip a nail this morning! Yes, yes, I know she has many nails so clipping one single nail might not sound like a big deal, but since I’ve had more time on my hands lately, I have been dedicating meal times to trying to get her less fearful of the process. To be fair to her, she does have reason to fear - when she was little I was clipping her nails and she moved at just the wrong moment and I clipped it much shorter than planned and it bled quite a lot. That time obviously hurt and she’s been fearful since. So, for the past week or so I have been bringing the clippers and dremmel to every mealtime. I’ve sat on the floor and asked her for a paw then hand fed her some food every time she gives it to me and lets me play with it, without pulling away. Getting her to keep her foot still is crucial if I am to avoid a repeat of the time that hurt. I’ve been bringing the clippers to her toes for days now and managed to cut three the other day but she’s been too wriggly and tense to make a cut on the one nail that I hurt last time. Today we finally got her to the point where she was obviously calm and non-wriggly so I snipped the end off snd she was like “oh, weird, that didn’t hurt!” She was so proud of herself bless her - she obviously got all her food in celebration. 😁 It might take many sessions to cut all of her nails but if I can get her over her fear it will pay off in the long run. 🎉End ofSep-25Oct-25Brother 7,800.00 7,650.00 Overdraft owed 0.00 0.00 MBNA CC 11,481.53 11,504.06 Barclaycard CC 9,662.17 9,558.10 Fluid CC 1,046.44 1,036.29 NatWest CC 11,705.36 11,693.03 Aqua 1,127.94 1,107.94

Total debt

42,823.44

42,549.42Paid off in the month 211.33 274.02

Interested in my diary? Check out...

https://forums.moneysavingexpert.com/discussion/6580468/teetering-on-the-brink/p16 -

See, that’s what I thought about the tent buying - perfect time to look. 🤞ellenvan said:You might be able to get cheap camping gear at this time of year, as out of season. Maybe think about incorporating into Christmas presents anything they may need for uni?

Any amount paid off the fluid card will be a bonus and save money on interest.

How's the £5 challenge going, or is that on hold until you are feeling better

Thankfully the girl’s pretty much have everything they need for uni already. dd1 has been collecting random bits for ages as she knows there is not going to be a pot of money to kit her out come September. To be honest I think the day when her pink plates and bowls stop appearing in the dishwasher will be when it hits me that she has gone. 😕 (She chose the colour btw, mine are black, dd2 chose white and dd1 went for bright pink!🤦♀️) We must be one of the few households where even the children have their own pizza wheel! 🤣

I digress.

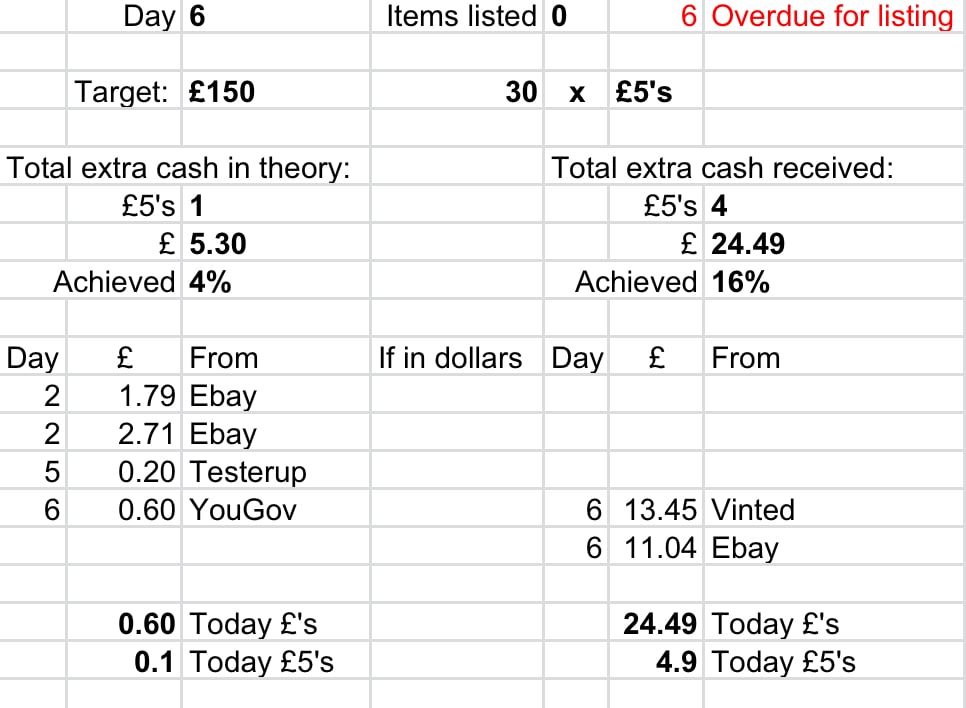

So, £5 challenge. Yes, that’s kind of been on hold whilst I’ve been so ill but will be getting back on it now. I have had a bit of cash coming in so some progress has been made…

End ofSep-25Oct-25Brother 7,800.00 7,650.00 Overdraft owed 0.00 0.00 MBNA CC 11,481.53 11,504.06 Barclaycard CC 9,662.17 9,558.10 Fluid CC 1,046.44 1,036.29 NatWest CC 11,705.36 11,693.03 Aqua 1,127.94 1,107.94

Total debt

42,823.44

42,549.42Paid off in the month 211.33 274.02

Interested in my diary? Check out...

https://forums.moneysavingexpert.com/discussion/6580468/teetering-on-the-brink/p12 -

That sounds like a great dissemination of the unexpected extra. Well done persevering so slowly with little dog, so many people rush these things and think oh I've tried twice clearly its never going to work, fabulous.

Dxx22: 3🏅 4⭐ 23: 5🏅 6 ⭐ 24 1🏅 2⭐ 25 🏅 🥈2⭐ 26 🥈 Never save something for a special occasion. Every day is a special occasion. The diff between what you were yesterday and what you'll be tomorrow is what you do today Well organised clutter is still clutter - Joshua Becker If youre not already using a thing you won't start using it more by shoving it in a cupboard- AJMoney The barrier standing between you & what youre truly capable of isnt lack of info, ideas or techniques. The secret is 'do it'3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards