We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Hopefully debt free before Mortgage renewal in June 2026

Comments

-

I once pointed out to a bank I was remortgaging with that my fee for remaining loyal to them was exactly the same for someone with no history with them. I explained that this would discourage me renewing with them and they waived the fee.

Other thing I would do is determine a minimum level for emergency funds and reduce the amount to be borrowed by as much as possible. Every thousand counts.

Are all these offers with the same bank?Mortgage at 01.01.14 £119,481.83:eek: today £0 Emergency fund £5.5/5.5k & £200/200 cash.:jWeight 24/02/19 14st 7lb now 12st 1lb determined to stop defining myself by my mistakes. Progress not perfection.:T100%through my 1% mortgage challenge. 100% through my pb challenge. I’m not perfect but I’m good enough.1 -

Hi Tezza, if only we had a crystal ball…. What to do?? Firstly, as you suggest maybe it is worth finding out if you can choose something now, but change it before you renew, in case rates do go down (or up).

Secondly, are you sure that staying with your existing lender is the only option available to you? Is it worth speaking to a broker to find out if there are any other deals for you. As you are now a Saver and debt free :)

Next it's the choice of 2 or 5 years. Personally I like to fix, but again we don't know what is going to happen. Do these deals all have ERCs (Early Repayment Charges) on them? If you pick 5 and rates drop a lot, you can always change lender.

You are in a good position with 60% LTV and you have buying power, so for now I'd do the selection with your lender (without signing) and then chat to a broker to see where that leads.

Good luck Tezza V x

1 -

………………………………..

Debts Jan 6th 2025 = £6465.60

Debts Jan 6th 2025 = £6465.60

Natwest CC £0 - 25/12/25If you are interested in investing, you can get free shares up to £100 if you open a Trading212 account with this link > > https://www.trading212.com/invite/FMcH7elUMy Savings T212 investment pie https://www.trading212.com/pies/ltzw4Wew651jgq4oGrepyrZJB4TgC

X (Twitter) : https://x.com/Savvy_Squirrel_0 -

……………………………..….

Debts Jan 6th 2025 = £6465.60

Debts Jan 6th 2025 = £6465.60

Natwest CC £0 - 25/12/25If you are interested in investing, you can get free shares up to £100 if you open a Trading212 account with this link > > https://www.trading212.com/invite/FMcH7elUMy Savings T212 investment pie https://www.trading212.com/pies/ltzw4Wew651jgq4oGrepyrZJB4TgC

X (Twitter) : https://x.com/Savvy_Squirrel_2 -

It would be a nice help if the fee was waved and i could take the lower percentage mortgage.

If i could reduce the amount owed to help with lower monthly repayments then i would for sure but im not in the fortunate position to be able to do that.

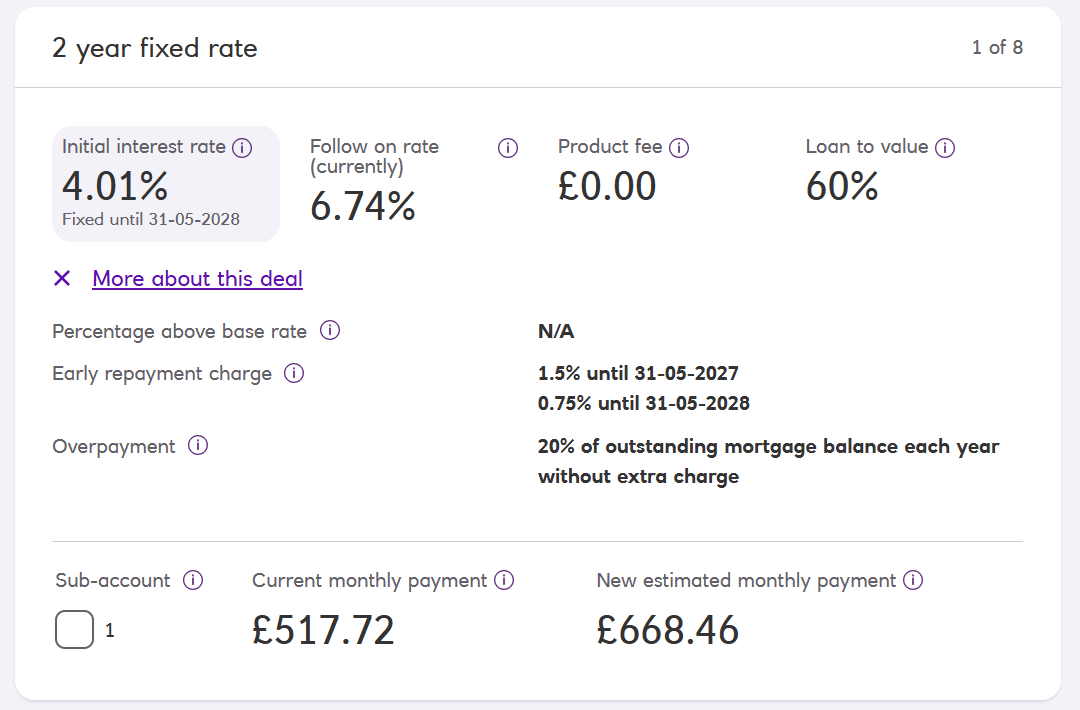

Yes they are all with my current mortgage company and bank Natwest, These are the renewal options i have been given.

Debts Jan 6th 2025 = £6465.60

Natwest CC £0 - 25/12/25If you are interested in investing, you can get free shares up to £100 if you open a Trading212 account with this link > > https://www.trading212.com/invite/FMcH7elUMy Savings T212 investment pie https://www.trading212.com/pies/ltzw4Wew651jgq4oGrepyrZJB4TgC

X (Twitter) : https://x.com/Savvy_Squirrel_0 -

Hi Vamp, yep it sure would be nice to have a crystal ball. From what i have read you can choose a renewal deal now and change it before the renewal date if rates change so i will look into this more this weekend and maybe choose one for now to lock it in to cover any potential rise in rates due to the war.

I have had a quick comparison and the top mortgages are all very similar with Natwest in the list. So to avoid all the hassle of going through all the personal and financial checks with another lender to save a minimal amount its worth just staying with Natwest on this occasion to avoid the hassle of any checks at all.

Yes they all have ERCs attached with them as you can see below.

I still can't decide between 2 or 5 years, its a case of what to do for the best? could end up kicking myself either way.

yes i actually have 55% LTV but the best rate they offer is 60% so its good to have a little bit of collateral to be able to get a slightly better deal. I will look to lock in one of the options this weekend maybe and then weigh up my options before the renewal date.

Thanks for the helpful advice x

Debts Jan 6th 2025 = £6465.60

Natwest CC £0 - 25/12/25If you are interested in investing, you can get free shares up to £100 if you open a Trading212 account with this link > > https://www.trading212.com/invite/FMcH7elUMy Savings T212 investment pie https://www.trading212.com/pies/ltzw4Wew651jgq4oGrepyrZJB4TgC

X (Twitter) : https://x.com/Savvy_Squirrel_0 -

So i had some pretty rubbish news at work today. They are reducing my departments hours from 40 hours per week to 37.5 hours a week from April 6th 2026. It is ultimately to mitigate the rise in national minimum wage increase starting from April.

So i have worked out the following :

What i earn now = 40 x £12.21 = £488.40 (per week), x 52 = £25,396.80 (per year)

What i will earn = 37.50 x £12.71 (including new min wage increase of 50pph) x 52 = £24,784.50 (per year)

Difference = -£612.30 less per year or -£51.02 less per month

The amount i was planning on having after a minimum wage increase (announced on 25th Nov 2025 by the Government) is 40 x £12.71 x 52 = £26,436.80

The amount i will actually receive now the company i work for has decided to cut my hours to 37.5 hours a week = 37.5 x £12.71 x 52 = £24,748.50

The swing in difference of what i was expecting and had planned for in the future to what i am actually going to be getting now is £26,436.80 - £24,748.50 = £1,652.30 per year

So im effectively going to be getting £1650+ per year or £137.69 per month LESS than what i thought i would be getting from next month onwards.

It is really rubbish timing with my mortgage renewal coming up in the next few months aswell. So now i have my eyes closely on the jobs market but i am also wary as i dont want to go from the frying pan into the fire so to speak. It takes me quite a while to find a new job as i want to be sure it is one i will be comfortable doing and not regret my decision. Living alone and solely responsible for all the household bills puts more pressure on getting this decision right. Im unsure whether to try and just make ends meet for now until my mortgage is renewed and to see how the war plays out for the next few months before looking to find alternative employment with better pay or more hours, or both. I'm sure it won't harm to see what is on offer out there at the moment for now.

Just when i think things are going ok 🤦🏼♂️

Debts Jan 6th 2025 = £6465.60

Debts Jan 6th 2025 = £6465.60

Natwest CC £0 - 25/12/25If you are interested in investing, you can get free shares up to £100 if you open a Trading212 account with this link > > https://www.trading212.com/invite/FMcH7elUMy Savings T212 investment pie https://www.trading212.com/pies/ltzw4Wew651jgq4oGrepyrZJB4TgC

X (Twitter) : https://x.com/Savvy_Squirrel_1 -

I still can't decide between 2 or 5 years, its a case of what to do for the best? could end up kicking myself either way.

Firstly, as Martin says - you can make a good decision that ends up with a bad outcome. Thats not something you should kick yourself for. If you do research, do figures, take your own risk aversion into account then you are making a good decision. The outcome is not in your control. So don't get stymied by focusing on the things out your control.

I'd say you answered your own question by noting that you are relying on one income. Id say that suggests you are looking at fixed rates, not tracker or variable as a jump in interest rates may mean you cannot afford to live in your own house. Yes interest rates may come down. Yes they may go up. Not important. The only important thing is what you can afford each month and how long you are happy knowing thats how much you will pay. If you are willing to gamble, take the 2 years. If you want the certainty of knowing for longer, go for 5.

So the next decision is an arithmetic one

looking at the 6 fixes

5 year = 60 months (How much over the first 2 years)

3.85% £657.57 a month x 60 £39,454.20 +£1500 fee = £40,954.20 (x 24 £17,281.68)

3.9% £660.96 a month x 60, £39,657.60 + £1000 fee =£40,657.60 (x 24 £16863.04)

4.02% £669.14 a month x 60 , £40,148.40 (x 24 £16056)

2 year = 24 months

3.68% £646.10 a month x 24, £15506.40+ £1500 fee = £17006.40

3.73% £649.46 a month x 24, £15587.04+ £1000 fee = £16587.04

4.01% £668.46 a month x 24, £16043.04

22: 3🏅 4⭐ 23: 5🏅 6 ⭐ 24 1🏅 2⭐ 25 🏅 🥈2⭐ 26 🥈 Never save something for a special occasion. Every day is a special occasion. The diff between what you were yesterday and what you'll be tomorrow is what you do today Well organised clutter is still clutter - Joshua Becker If youre not already using a thing you won't start using it more by shoving it in a cupboard- AJMoney The barrier standing between you & what youre truly capable of isnt lack of info, ideas or techniques. The secret is 'do it'2 -

So looking at the figures for the 5 year fixes

Saving £11.57 on your monthly payment to get the slightly better interest rate (£657 instead of £669), you actually pay £805 more over the life of the fix. If you need to have the lower monthly figure then thats the cost. Plus you might have to find the fee upfront? Maybe they add it on but of course that makes the figure much higher as you'll pay interest on that fee.

If you compare the 2 year fixes against the first 2 years of the 5 year fixes, again the higher interest no fee is mathematically better - a bigger margin between the highest £1500 fee compared to the no fee. And of course in 2 years you'll be going through this again trying to find a good deal. Interest might be higher, might be lower, who knows, no one therefore the only thing you can weigh against that is how risk averse you feel, how much you want certainty.

Comparing the figures for the 2 year no fee fix and the first 2 years of the 5 year fix there's less than £15 in it - its how important the longer term peace of mind is to you. By then interest rates may be 9% and you'll be glad. They might be 2% and it's enough of a difference to pay the erc and re fix on a new deal. Its a good erc, very low plus being able to overpay by 20% is very good. If you do get a better job or come into some money thats a significant amount you can pay off without extra penalty.

Dxxx

(People my age remember 15% mortgages and the terrible day the rate went up twice in one day. So these percentages being so low for so long is definitely the anomaly but I know its what we have been used to very recently. I took a ten year fix at one point in my mortgage journey. Turned out not great as they gradualky dropped from around the 8 or 9 % to around 5% and we bought out after 6 years I think. Wasnt a bad decision, even though for a while we paid more a month than we might have (certainty was really really important to us) just a less favourable outcome.)

22: 3🏅 4⭐ 23: 5🏅 6 ⭐ 24 1🏅 2⭐ 25 🏅 🥈2⭐ 26 🥈 Never save something for a special occasion. Every day is a special occasion. The diff between what you were yesterday and what you'll be tomorrow is what you do today Well organised clutter is still clutter - Joshua Becker If youre not already using a thing you won't start using it more by shoving it in a cupboard- AJMoney The barrier standing between you & what youre truly capable of isnt lack of info, ideas or techniques. The secret is 'do it'3 -

the job news is shocking but you have shown massive resilience so far. I’m sure you’ll deal with this equally as well. With the reduction in hours, could you look at taking on a part time job? It’d help minimise both financial risk and dependency on your main employer.

Mortgage at 01.01.14 £119,481.83:eek: today £0 Emergency fund £5.5/5.5k & £200/200 cash.:jWeight 24/02/19 14st 7lb now 12st 1lb determined to stop defining myself by my mistakes. Progress not perfection.:T100%through my 1% mortgage challenge. 100% through my pb challenge. I’m not perfect but I’m good enough.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards