We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

The Old Regular Savers Discussion Thread 28/12/24-29/1/26

Comments

-

Not necessarily!flaneurs_lobster said:

** NOTE TO SELF **wmb194 said:

I think it's indicating that it's not yet cleared. On Saturday when I made the DC deposit it also showed an asterisk as well but this morning it's disappeared.Aidanmc said:Hanley BS RS

Any idea what the little asterisk means, if anything?

Next month make deposit to Hanley BS RS by DC, because it'll clear quicker than my FP which is still nowhere to be seen.

I paid by debit card on the first as it's supposed to be immediate. Some sort of "rare" occurrence happened, according to them, and I am still waiting for it to be credited to my account. Apparently they can see it but it's not within their control yet so we have to keep waiting until that happens. I am assured they will backdate it so that I won't loose interest though.0 -

Salutations. Are you overthinking, perhaps? Why not just w/d the £3k? It''ll get due interest paid on the 11th and you're good to go for another year, by whatever means. No risk of lock out for a year.CricketLady said:Good morning all,

I need to withdraw £3000 from my Halifax regular saver which is due to mature on the 11th (Tuesday) as I have a big bill to pay today. I managed to withdraw £3000 from my Bank of Scotland (well, £2999, I left £1 in for the interest to have something to "stick to" when it gets added on at maturity, also on Tuesday) but with my Halifax I only have the option to RENEW.

If I renew does that mean I'll be able to get my cash out and start again with another £250 or will that £3000 stay in the account until 11th November 2026?

I definitely need this cash and can't wait till Tuesday so is there a better way to access the £3k?

Sorry for silly question but CricketLady has definitely reached a certain age!

And sending you all lots of love xx0 -

The only regular saver accounts that I hold that require deposit from nominated accounts are my Manchester and my Newcastle Monument account. (but not my 5.25% Newcastle reg)francoghezzi said:

I prefer to pay from the nominated account in order to avoid any problems and because, frankly, I don't remember which BS accept payments even from other sources. So I prefer the easy way, but it is just personal. I edited my post to make sure that this is clearer . Wherever your money comes from the on line banking should be updated at some point todayKim_13 said:

You mentioned nominated accounts, but I wasn’t aware that funds had to come from the nominated account? I nominated the account the cheque came from as I thought that would be easier but would rather pay in from another account going forward if possible.francoghezzi said:SCOTTISH BUILDING SOCIETY SO

Just had a chat with a nice lady at the Scottish BS regarding the timing to update the online banking with the standing orders from nominated bank accounts. It looks that is normally taking 48 hours. So for those still wondering if their money sent last week-end or during Sunday night safely landed the best advice is to check the on line portal at some point today and remember this quite slow process for the months to come (and brace yourselves when it comes to the deposit on the first of January :-) )

1 -

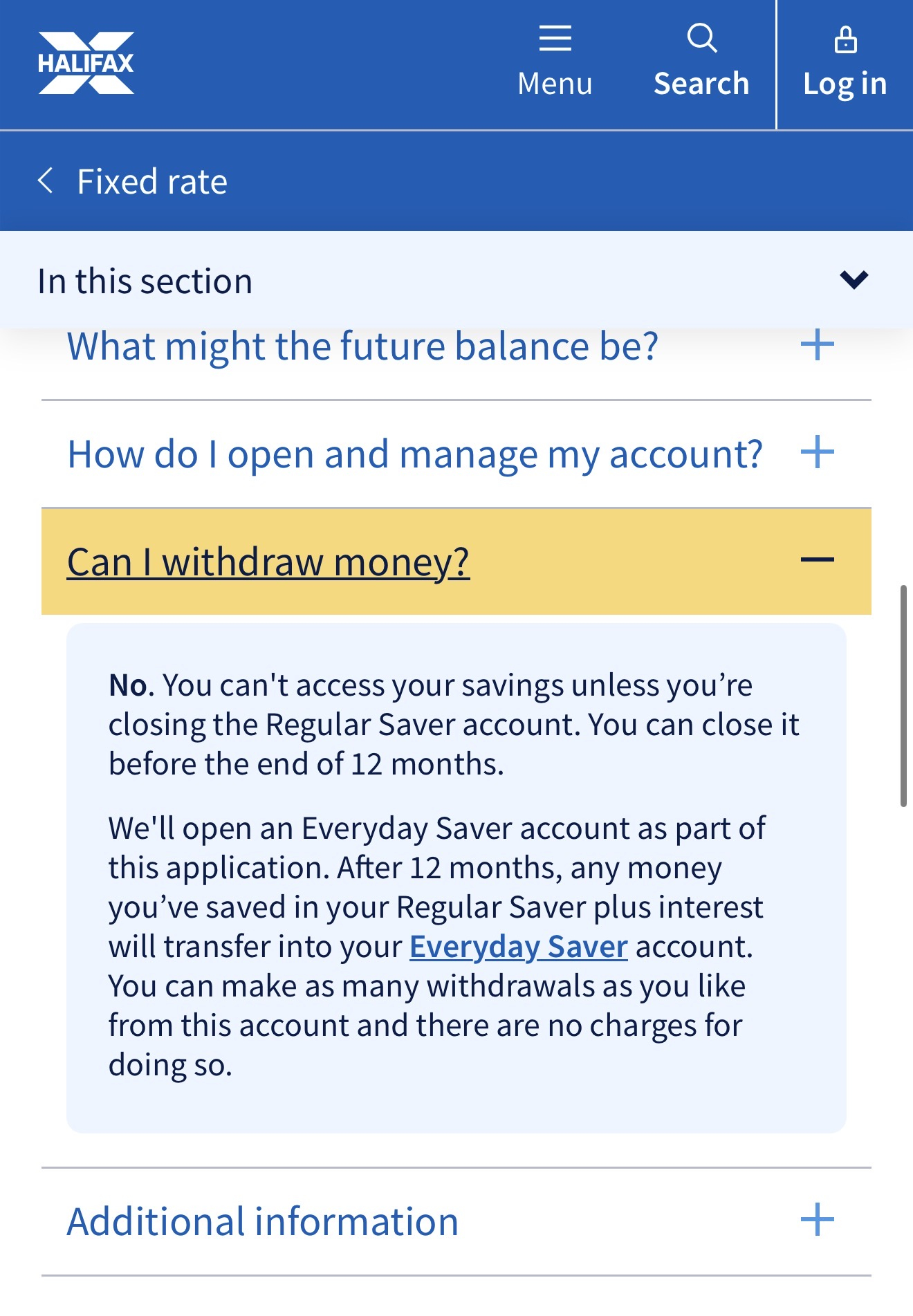

Withdrawals aren’t permitted without closure/renewal.soulsaver said:

Salutations. Are you overthinking, perhaps? Why not just w/d the £3k? It''ll get due interest paid on the 11th and you're good to go for another year, by whatever means. No risk of lock out for a year.CricketLady said:Good morning all,

I need to withdraw £3000 from my Halifax regular saver which is due to mature on the 11th (Tuesday) as I have a big bill to pay today. I managed to withdraw £3000 from my Bank of Scotland (well, £2999, I left £1 in for the interest to have something to "stick to" when it gets added on at maturity, also on Tuesday) but with my Halifax I only have the option to RENEW.

If I renew does that mean I'll be able to get my cash out and start again with another £250 or will that £3000 stay in the account until 11th November 2026?

I definitely need this cash and can't wait till Tuesday so is there a better way to access the £3k?

Sorry for silly question but CricketLady has definitely reached a certain age!

And sending you all lots of love xx

3 -

Halifax doesn't work like Lloyds. The Lloyds is easy access; the Halifax you have to close to access your moneyfrancoghezzi said:

It works exactly like Lloyds. Do not close it, just renew it choosing between the savings accounts with low interests rates, then take your money and interests accrued to today, close immediately the new account with a lower interest and re-open the regular saver 5.5% that will re-appear between your options clicking on the apply button. I have done it on 31/10 so as to be able to deposit twice in 24 hours starting again the RSCricketLady said:Good morning all,

I need to withdraw £3000 from my Halifax regular saver which is due to mature on the 11th (Monday) as I have a big bill to pay today. I managed to withdraw £3000 from my Bank of Scotland (well, £2999, I left £1 in for the interest to have something to "stick to" when it gets added on at maturity, also on Monday) but with my Halifax I only have the option to RENEW.

If I renew does that mean I'll be able to get my cash out and start again with another £250 or will that £3000 stay in the account until 11th November 2026?

I definitely need this cash and can't wait till Monday so is there a better way to access the £3k?

Sorry for silly question but CricketLady has definitely reached a certain age!

And sending you all lots of love xxI consider myself to be a male feminist. Is that allowed?1 -

Halifax don't allow withdrawals, early closure/renewing only. If you renew the whole balance is immediately available in the Easy Saver or whatever you renew to, whereas requesting closure might well lead to manual intervention being required and slowing down the process.soulsaver said:

Salutations. Are you overthinking, perhaps? Why not just w/d the £3k? It''ll get due interest paid on the 11th and you're good to go for another year, by whatever means. No risk of lock out for a year.CricketLady said:Good morning all,

I need to withdraw £3000 from my Halifax regular saver which is due to mature on the 11th (Tuesday) as I have a big bill to pay today. I managed to withdraw £3000 from my Bank of Scotland (well, £2999, I left £1 in for the interest to have something to "stick to" when it gets added on at maturity, also on Tuesday) but with my Halifax I only have the option to RENEW.

If I renew does that mean I'll be able to get my cash out and start again with another £250 or will that £3000 stay in the account until 11th November 2026?

I definitely need this cash and can't wait till Tuesday so is there a better way to access the £3k?

Sorry for silly question but CricketLady has definitely reached a certain age!

And sending you all lots of love xx1 -

So is there like a "renew" button to press or is it renew in the sense that we use the word in this forum and there's a process to follow that leads to renewal. (if this makes sense! )Kim_13 said:

Halifax don't allow withdrawals, early closure/renewing only. If you renew the whole balance is immediately available in the Easy Saver or whatever you renew to, whereas requesting closure might well lead to manual intervention being required and slowing down the process.soulsaver said:

Salutations. Are you overthinking, perhaps? Why not just w/d the £3k? It''ll get due interest paid on the 11th and you're good to go for another year, by whatever means. No risk of lock out for a year.CricketLady said:Good morning all,

I need to withdraw £3000 from my Halifax regular saver which is due to mature on the 11th (Tuesday) as I have a big bill to pay today. I managed to withdraw £3000 from my Bank of Scotland (well, £2999, I left £1 in for the interest to have something to "stick to" when it gets added on at maturity, also on Tuesday) but with my Halifax I only have the option to RENEW.

If I renew does that mean I'll be able to get my cash out and start again with another £250 or will that £3000 stay in the account until 11th November 2026?

I definitely need this cash and can't wait till Tuesday so is there a better way to access the £3k?

Sorry for silly question but CricketLady has definitely reached a certain age!

And sending you all lots of love xx0 -

There is a prominent 'Renew' button beside the account on the Halifax Landing pages71hj said:

So is there like a "renew" button to press or is it renew in the sense that we use the word in this forum and there's a process to follow that leads to renewal. (if this makes sense! )Kim_13 said:

Halifax don't allow withdrawals, early closure/renewing only. If you renew the whole balance is immediately available in the Easy Saver or whatever you renew to, whereas requesting closure might well lead to manual intervention being required and slowing down the process.soulsaver said:

Salutations. Are you overthinking, perhaps? Why not just w/d the £3k? It''ll get due interest paid on the 11th and you're good to go for another year, by whatever means. No risk of lock out for a year.CricketLady said:Good morning all,

I need to withdraw £3000 from my Halifax regular saver which is due to mature on the 11th (Tuesday) as I have a big bill to pay today. I managed to withdraw £3000 from my Bank of Scotland (well, £2999, I left £1 in for the interest to have something to "stick to" when it gets added on at maturity, also on Tuesday) but with my Halifax I only have the option to RENEW.

If I renew does that mean I'll be able to get my cash out and start again with another £250 or will that £3000 stay in the account until 11th November 2026?

I definitely need this cash and can't wait till Tuesday so is there a better way to access the £3k?

Sorry for silly question but CricketLady has definitely reached a certain age!

And sending you all lots of love xx1 -

Only works on the website and not in the app though, when I last did it a few years ago.ColdIron said:

There is a prominent 'Renew' button beside the account on the Halifax Landing pages71hj said:

So is there like a "renew" button to press or is it renew in the sense that we use the word in this forum and there's a process to follow that leads to renewal. (if this makes sense! )Kim_13 said:

Halifax don't allow withdrawals, early closure/renewing only. If you renew the whole balance is immediately available in the Easy Saver or whatever you renew to, whereas requesting closure might well lead to manual intervention being required and slowing down the process.soulsaver said:

Salutations. Are you overthinking, perhaps? Why not just w/d the £3k? It''ll get due interest paid on the 11th and you're good to go for another year, by whatever means. No risk of lock out for a year.CricketLady said:Good morning all,

I need to withdraw £3000 from my Halifax regular saver which is due to mature on the 11th (Tuesday) as I have a big bill to pay today. I managed to withdraw £3000 from my Bank of Scotland (well, £2999, I left £1 in for the interest to have something to "stick to" when it gets added on at maturity, also on Tuesday) but with my Halifax I only have the option to RENEW.

If I renew does that mean I'll be able to get my cash out and start again with another £250 or will that £3000 stay in the account until 11th November 2026?

I definitely need this cash and can't wait till Tuesday so is there a better way to access the £3k?

Sorry for silly question but CricketLady has definitely reached a certain age!

And sending you all lots of love xx0 -

I deposit to Newcastle Monument from different account. Manchester is the only one in my RS collection that requires deposits from nominated account.Speculator said:

The only regular saver accounts that I hold that require deposit from nominated accounts are my Manchester and my Newcastle Monument account. (but not my 5.25% Newcastle reg)francoghezzi said:

I prefer to pay from the nominated account in order to avoid any problems and because, frankly, I don't remember which BS accept payments even from other sources. So I prefer the easy way, but it is just personal. I edited my post to make sure that this is clearer . Wherever your money comes from the on line banking should be updated at some point todayKim_13 said:

You mentioned nominated accounts, but I wasn’t aware that funds had to come from the nominated account? I nominated the account the cheque came from as I thought that would be easier but would rather pay in from another account going forward if possible.francoghezzi said:SCOTTISH BUILDING SOCIETY SO

Just had a chat with a nice lady at the Scottish BS regarding the timing to update the online banking with the standing orders from nominated bank accounts. It looks that is normally taking 48 hours. So for those still wondering if their money sent last week-end or during Sunday night safely landed the best advice is to check the on line portal at some point today and remember this quite slow process for the months to come (and brace yourselves when it comes to the deposit on the first of January :-) )1

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.1K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards