We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Bonds and Misery

Comments

-

Nice to finally see some shortish duration I/L Gilt fund options available.

0 -

Yes, thanks.Bobziz said:

Have you considered creating your own single gilt ladder rather than a fund?leosayer said:My approach to bond is to only hold GBP Gilt funds that have an average duration that I am comfortable with, based on my time horizon which is 12 years.

I have enough volatility and currency exposure on my global equity fund holdings, so I don't feel I need corporate bonds, foreign government bonds or currency exposure.

As a result, I currently only hold IGL5: iShares UK Gilts 0-5yr UCITS ETF GBP (Acc) which has an average duration of just over 2 years - a bit less than I'd like.

I'm considering extending the duration and adding index-linked gilts with some allocation to:

- iShares Up to 10 Years Index Linked Gilt Index Fund (avg duration 5.4 yrs)

- Legal & General All Stocks Gilt Index Trust (avg duration 8.3 yrs)

Right now I'm holding off until I have a better understanding of the post-budget income / pension / ISA tax regime and whether I take to retirement in April as well as I expect.

One additional complication is that most of my retirement savings are in a DC master trust that has limited investment options. It is linked to a DB scheme so realistically, I can't change allocations until I commence my DB, probably in 2026.1 -

Active bond funds for me, as I feel there is value to be had from being selective and I don't have time to do that. It didn't help when they all dropped a couple of years ago but have been great since. Just one example is Royal London Sterling Extra Yield Bond, returns after their higher charges have been good.

1 -

I wondered when interest rates do eventually start falling will bond prices in funds such as life strategy start increasing straight away or is this already factored in because of the expectation that lower rates are on the way?

0 -

There was some increase around the time rates started to fall, but it could easily have been missed.P933alilli said:I wondered when interest rates do eventually start falling will bond prices in funds such as life strategy start increasing straight away or is this already factored in because of the expectation that lower rates are on the way?

0 -

Gazzabloom : I am seeing several threads like this on bogleheads and reddit --> almost implying bonds no longer have a place in a portfolio. I am guilty of starting the thread in a very negative note as well, full of panic.

I thought the point of bonds is not to add risk. That's why one is supposed to go for "quality" i.e govt bonds of developed economies and avoid corporate bonds. And when equities tank, there is supposedly a "flight to quality" so these bonds would benefit, giving your portfolio a cushioning effect. By adding bonds in your portfolio, you are not adding risk, but you have another positive return asset class which is not correlated with equities, and that's the free lunch. This is the theory anyway. Occaminvesting's classic bond article recommends intermediate term govt bonds.GazzaBloom said:I have toyed with the bonds funds puzzle for a few years after not holding any and still don't. I decided to accumulate cash instead to go alongside equity index funds.

My conclusion, which feels right for me is that cash (currently earning 5% BOE base rate) is my retirement “risk-off” money alongside my small DB pension.Money I want to invest and take risk with goes into equity index funds. I don't really see any point placing “risk” money in bonds funds. If I want risk it's equities, if I want low or no risk it's cash. Simple.

If you hold cash, you wont get the portfolio cushioning effect when equities tank, right ? yes cash returns 5% now but that's why we need to get into bonds now, right, so that if interest rates fall, our bonds would go up in value ? If not now when would you buy bonds then ?

I agree with your second post about VAGS, the one stop solution for bonds, although it has corporates.

The mistake I made was never buying bonds at all. I kept buying equities but I didn't go gung-ho on equities either. But I contributed heavily into pension and had it in the default company fund of 70% stocks, 30% bonds, but when it reached £1 million I moved to cash last year since I wanted to take the 25% out. Bad decision as the market went up a lot after that.

But at any rate, I now have a very large portfolio of which close to 50% is in equities and the rest is in cash. The cash part can easily fund 25 years of expenses at today's UK expenses for a comfy life. I am hesitant to move all of this into bonds (VAGS) in one shot. I am 56 and considering FIRE. Ideally I should have glided, owning both stocks and bonds and gradually easing from stocks to bonds.

Thanks

0 -

BlisteringBarnacles said:Gazzabloom : I am seeing several threads like this on bogleheads and reddit --> almost implying bonds no longer have a place in a portfolio. I am guilty of starting the thread in a very negative note as well, full of panic.

I thought the point of bonds is not to add risk. That's why one is supposed to go for "quality" i.e govt bonds of developed economies and avoid corporate bonds. And when equities tank, there is supposedly a "flight to quality" so these bonds would benefit, giving your portfolio a cushioning effect. By adding bonds in your portfolio, you are not adding risk, but you have another positive return asset class which is not correlated with equities, and that's the free lunch. This is the theory anyway. Occaminvesting's classic bond article recommends intermediate term govt bonds.GazzaBloom said:I have toyed with the bonds funds puzzle for a few years after not holding any and still don't. I decided to accumulate cash instead to go alongside equity index funds.

My conclusion, which feels right for me is that cash (currently earning 5% BOE base rate) is my retirement “risk-off” money alongside my small DB pension.Money I want to invest and take risk with goes into equity index funds. I don't really see any point placing “risk” money in bonds funds. If I want risk it's equities, if I want low or no risk it's cash. Simple.

If you hold cash, you wont get the portfolio cushioning effect when equities tank, right ? yes cash returns 5% now but that's why we need to get into bonds now, right, so that if interest rates fall, our bonds would go up in value ? If not now when would you buy bonds then ?

I agree with your second post about VAGS, the one stop solution for bonds, although it has corporates.

The mistake I made was never buying bonds at all. I kept buying equities but I didn't go gung-ho on equities either. But I contributed heavily into pension and had it in the default company fund of 70% stocks, 30% bonds, but when it reached £1 million I moved to cash last year since I wanted to take the 25% out. Bad decision as the market went up a lot after that.

But at any rate, I now have a very large portfolio of which close to 50% is in equities and the rest is in cash. The cash part can easily fund 25 years of expenses at today's UK expenses for a comfy life. I am hesitant to move all of this into bonds (VAGS) in one shot. I am 56 and considering FIRE. Ideally I should have glided, owning both stocks and bonds and gradually easing from stocks to bonds.

Thanks

Bonds are not risk free and a bonds fund can be as volatile as equities at times but can take a lot longer to recover. When I want "risk-off" I want to see something that doesn't go down in value. That's cash or STMMFs for me not bonds. I see bonds as an equally risky proposition as equities, maybe more so, just not as volatile most of the time and with notably lower returns.

I retire at the end of this year with less money than you have but I am at 80/20 equities/cash but with around 19% of annual living expenses covered by a small DB pension, which you could view as a "bonds" substitute.

50% cash seems too much for me, do you really need 25 years worth of retirement living expenses being eroded by inflation? I will be holding 4 years worth of expenses as cash against a 9 year retirement gap to state pension. Once our SPs kick in we will be pretty much covered for living expenses with those and the DB pension.

If I was comfortable with the returns 50% equities was giving me in relation to my needs then I would definitely consider moving some of that 50% cash, have you considered a partial annuity? or buying a small property? If you really want to put some of it to work in bonds then start drip feeding it across into VAGS monthly.

I wouldn't see any need to keep any more than 10 years of expenses as cash, enough to fill the gap to state pension. The rest can be put to work in the asset class you are most comfortable with.1 -

BlisteringBarnacles said:Gazzabloom : I am seeing several threads like this on bogleheads and reddit --> almost implying bonds no longer have a place in a portfolio. I am guilty of starting the thread in a very negative note as well, full of panic.

I thought the point of bonds is not to add risk. That's why one is supposed to go for "quality" i.e govt bonds of developed economies and avoid corporate bonds. And when equities tank, there is supposedly a "flight to quality" so these bonds would benefit, giving your portfolio a cushioning effect. By adding bonds in your portfolio, you are not adding risk, but you have another positive return asset class which is not correlated with equities, and that's the free lunch. This is the theory anyway. Occaminvesting's classic bond article recommends intermediate term govt bonds.GazzaBloom said:I have toyed with the bonds funds puzzle for a few years after not holding any and still don't. I decided to accumulate cash instead to go alongside equity index funds.

My conclusion, which feels right for me is that cash (currently earning 5% BOE base rate) is my retirement “risk-off” money alongside my small DB pension.Money I want to invest and take risk with goes into equity index funds. I don't really see any point placing “risk” money in bonds funds. If I want risk it's equities, if I want low or no risk it's cash. Simple.

If you hold cash, you wont get the portfolio cushioning effect when equities tank, right ? yes cash returns 5% now but that's why we need to get into bonds now, right, so that if interest rates fall, our bonds would go up in value ? If not now when would you buy bonds then ?

I agree with your second post about VAGS, the one stop solution for bonds, although it has corporates.

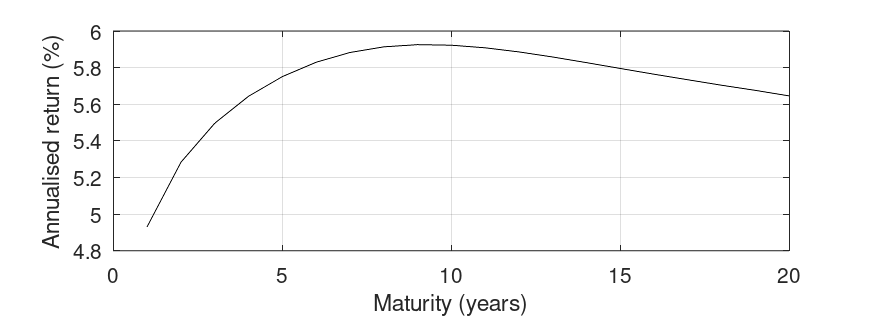

For interest, the historical annualised nominal returns (over the period 1915-2024 assuming no new money or withdrawals) for UK gilts as a function of maturity is given in the following figure*

The return peaks at maturities just under the 10 year mark and has a steeper decline at shorter maturities than longer ones. In other words, holding short duration gilts (or cash) produced a long-term return of just over 1 percentage point below gilts of intermediate maturities.

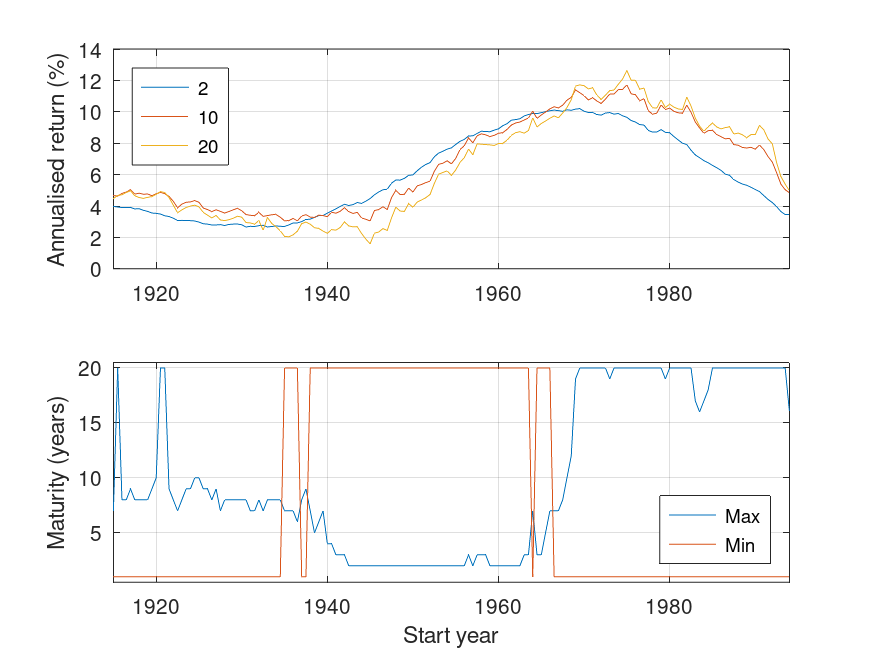

It is unlikely that anyone will invest in gilts for over 100 years, so a more realistic test is to look at shorter periods. In the following graph*, the annualised nominal return over 30 year rolling periods for gilts of 2, 10, and 20 years are shown in the top panel and the maturity which had the highest ('max') and lowest ('min') annualised return in the lower panel.

Looking at the upper panel, returns have certainly changed over time in the last 100 years or so, from values around 2% to 5% pre-WWII to a peak of 12% for 30 year periods starting in the mid-1970s.

Looking at the lower panel, in the period pre-WWII, with some exceptions, intermediate maturities (around the 8 year mark) did best and the lowest maturity (1 year) worst. In the period between WWII and the early 1960s, long bonds (20 year maturities) had the worst returns and shortish maturities (about 2 years) did best - this is because at the end of that period, yields increased dramatically and led to drops in price for long bonds (sound familiar?). Finally, in the period after about 1970, long maturities did best and short ones worst as the high yields of the 1970s gradually unwound and the bond bull market was in full swing

Anyway, a big problem with UK bond funds is that the standard one ('all stocks') that is commonly available had a duration that was too long in the run up to 2021 and shorter ones were not readily available (there were a few 0 to 5 year ones) and, of course, MMF of various (shortish) durations. As mentioned upthread, the addition of new funds following the 0 to 10 year gilt index might allow people to hold a more 'intermediate' maturity than previously. Those unaware that they were holding funds of the 'over 15 year' type (often used as lifestyling pre-annuity purchase) have been particularly caught out (as a few threads here testify) if their intention was drawdown and not an annuity.

So, IMV, the lessons that should be learnt is that care needs to be taken over the duration of the bond funds held and the mean duration of all fixed income (including cash) considered. Too short a duration (including cash) and the long-term returns will be lower, too long and the price volatility will be high, so 'intermediate' (however that is defined, but 5 to 15 years for UK gilts had roughly the same rerturns with the shorter end having less volatility) may be the goldilocks region.

Of course, it is impossible to say which duration will win out over the next 30 years.

* All calculations based on gilt yield curves calculated by Ellison and Scott (https://lbsresearch.london.edu/id/eprint/1204/1/AEJMacro-2018-0263.R1_Ellison_Scott_manuscript.pdf) until 1970 and the BoE yield curves after 1970. The returns are calculated based on buying the gilt at a given maturity (e.g., 10 years) at par and then, 6 months later, exchanging it for a gilt of the original maturity. While not a bond fund (although I can calculate those too), it is similar to how returns have been calculated for a limited range of maturities of US bonds by SBBI and UK gilts by Barclays.

6 -

It would be very informative to overlay inflation and the base rate on the annualised return time series plot.Looking at the tables and charts below really puts the data in context.A longer view of RPI is available hereI'm not old enough to remember what savings rates were like during those double digit bank rate years, but if similar to today, then I wouldn't discount cash as equivalent to the short end of the bond yield curve.1

-

Analysing bond duration along the yield curve versus holding cash assumes that growth is the priority. That's not why I hold cash. I hold it for certainty, liquidity and stability.

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards