We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

DB Pension - Options available - either take annual value or transfer to another provider

Comments

-

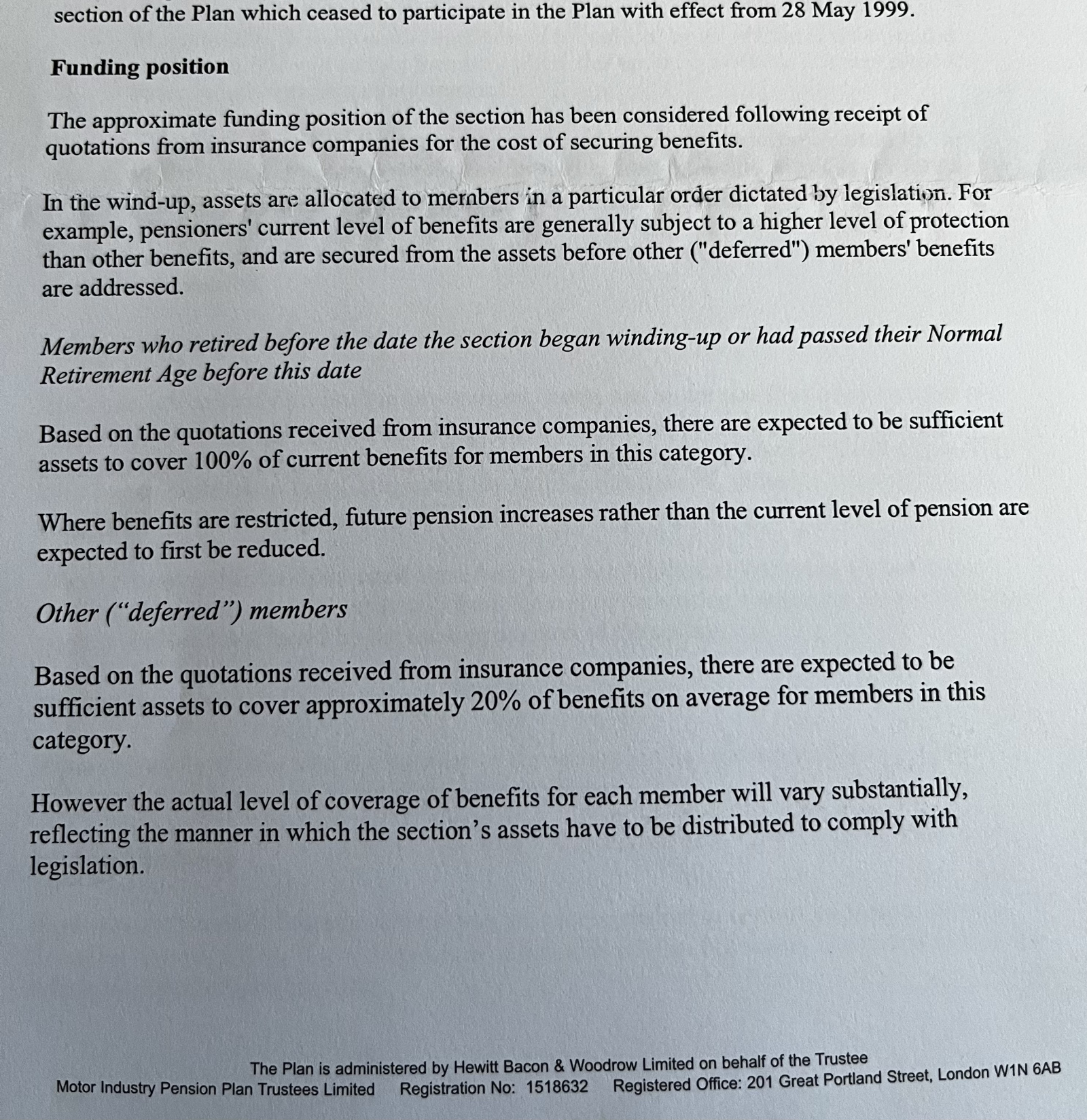

If there is a pension fund shortfall, the pension fund cannot be wound up - unless maybe the employer has become insolvent. But then the FAS or PPF would apply?

I am hazarding a guess that there was enough in the fund to cover the pensions of those who were already retired and just the revaluing GMP for the deferred pensioners who had them?

In 2000 (date of wind up) that would be all those who had accrued benefits pre 6/4/97.

You will note that there could be few who had accrued benefits after this date as it seems the sponsoring employer was in the process of closing down in mid 1999.

Capita indicates (2000) that "most members of the scheme left some time ago".

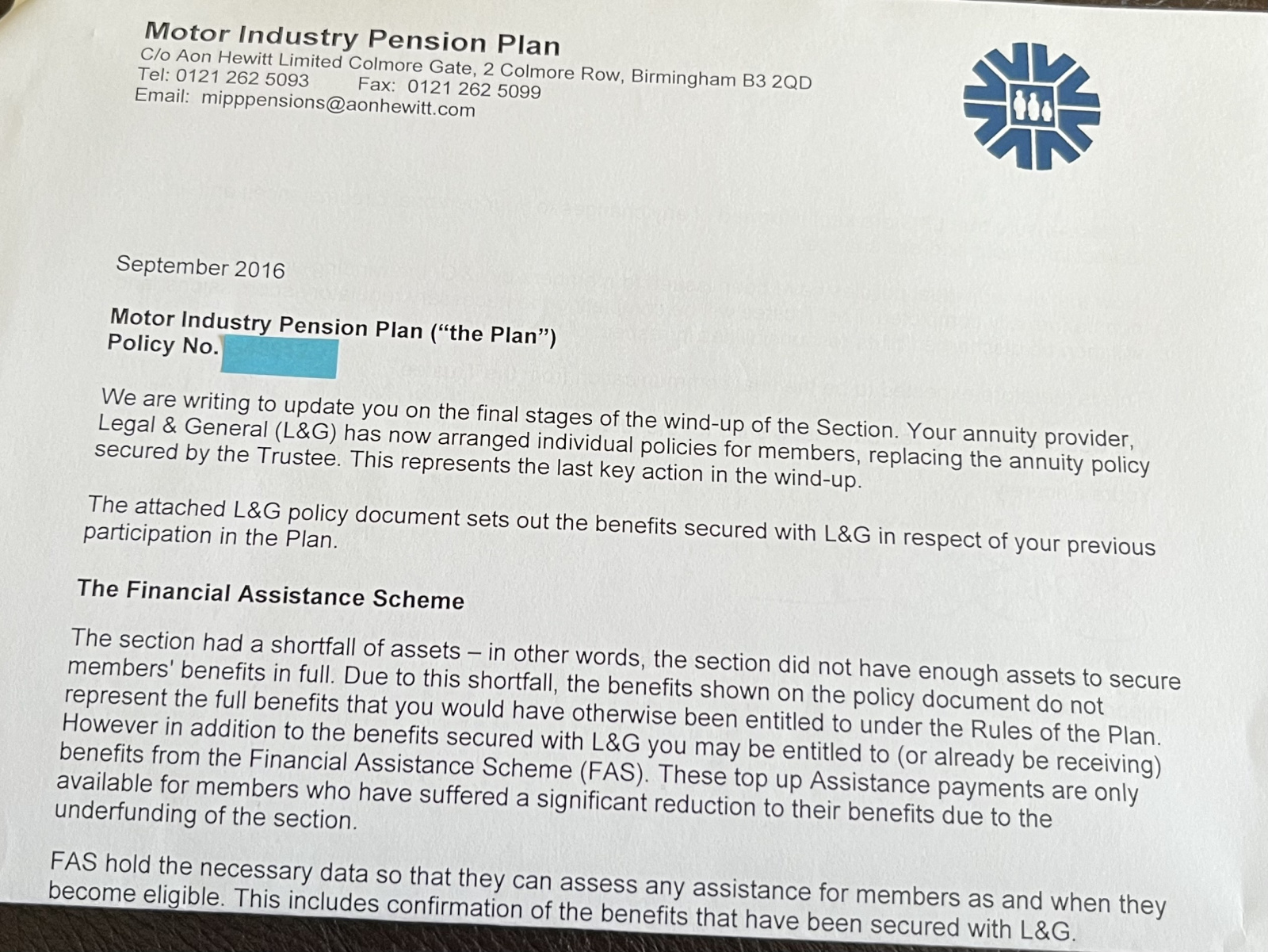

Capita arranged for L&G to provide the deferred members with S32 policies (?) - where there was a GMP the amount paid into the policy had to cover at least the GMP liability.

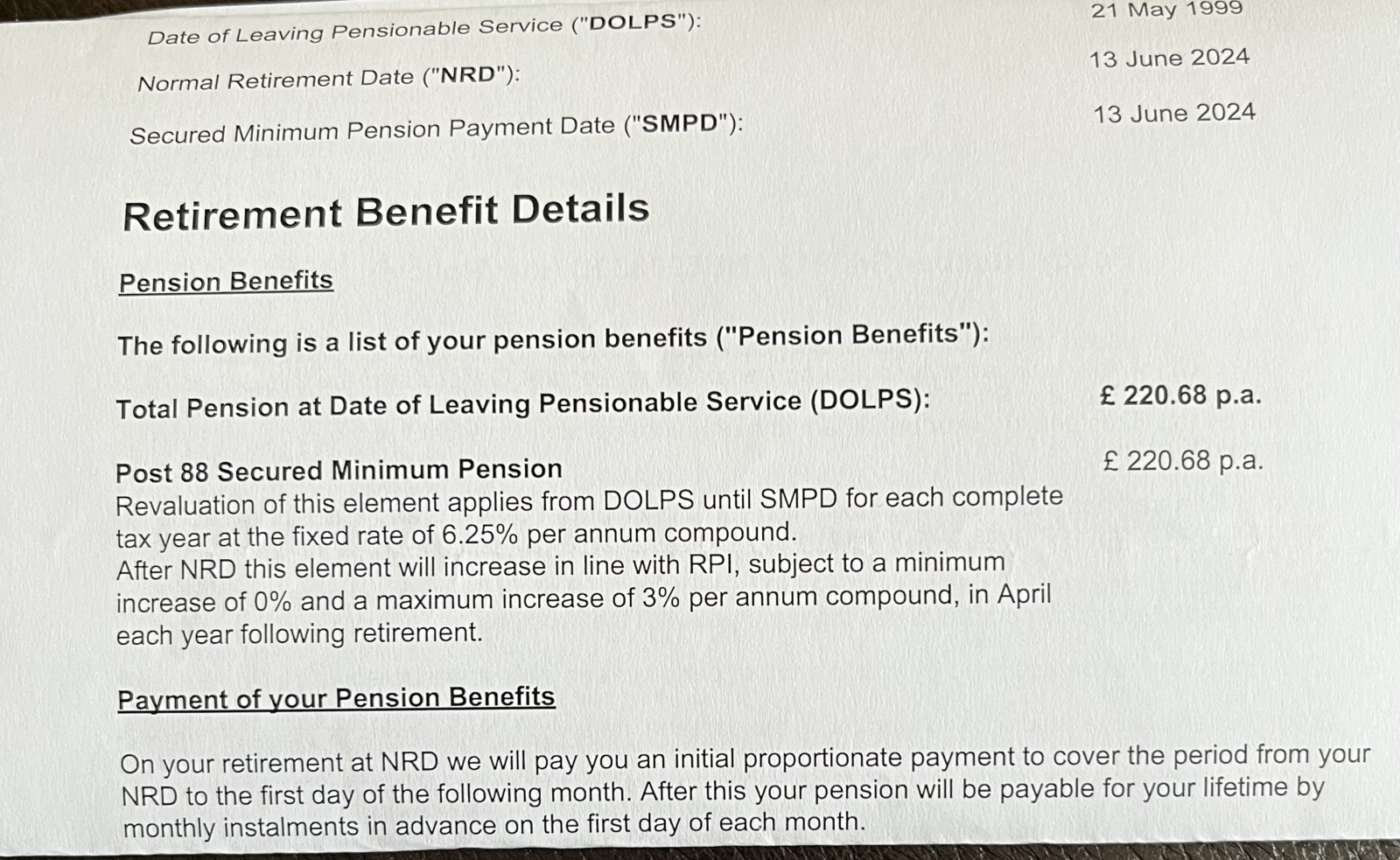

According to Scheme Rules, the revaluation could be no higher than the Fixed 6.5% and no lower than Full Rate.

The GMP (all post 88) was £439.92 at DOL in May 1999.

It has revalued for 25 years to age 60 (in 2024).

Do you happen to have a table for the result if Full Rate had been used for all years?

Again I am assuming that since the policy secured only the revalued GMP, there was no point in L&G's waiting waiting until NRA (65) to offer the pension.

This is only guesswork - obviously the OP can get the full facts from L&G.

0 -

I make it £1,885.00 if fixed rate and £953.38 if full rate (factor of 2.168). And yes, the slight discrepancy with the £945.00 previously quoted is bugging me...xylophone said:According to Scheme Rules, the revaluation could be no higher than the Fixed 6.5% and no lower than Full Rate.

The GMP (all post 88) was £439.92 at DOL in May 1999.

It has revalued for 25 years to age 60 (in 2024).

Do you happen to have a table for the result if Full Rate had been used for all years?

1

1 -

I make it £1,885.00 if fixed rate and £953.38 if full rate (factor of 2.168). And yes, the slight discrepancy with the £945.00 previously quoted is bugging me...

Thank you, hyubh

Oh dear, it's not much to show for eight years in a contributory DB Scheme is it?

At least it's post 88....

0 -

There should also be an excess over GMP - that benefit should have been secured somewhere.xylophone said:I make it £1,885.00 if fixed rate and £953.38 if full rate (factor of 2.168). And yes, the slight discrepancy with the £945.00 previously quoted is bugging me...Thank you, hyubh

Oh dear, it's not much to show for eight years in a contributory DB Scheme is it?

At least it's post 88....

EDIT: Which periods do FAS and the PPF apply?1 -

Good afternoon everyone. Thank you for your replies and your patience.

I have found some additional paperwork which I hope will add clarity. Here is an extract from a letter received in November 2006. 0

0 -

Here is an extract from a letter received in September 2016 -

0 -

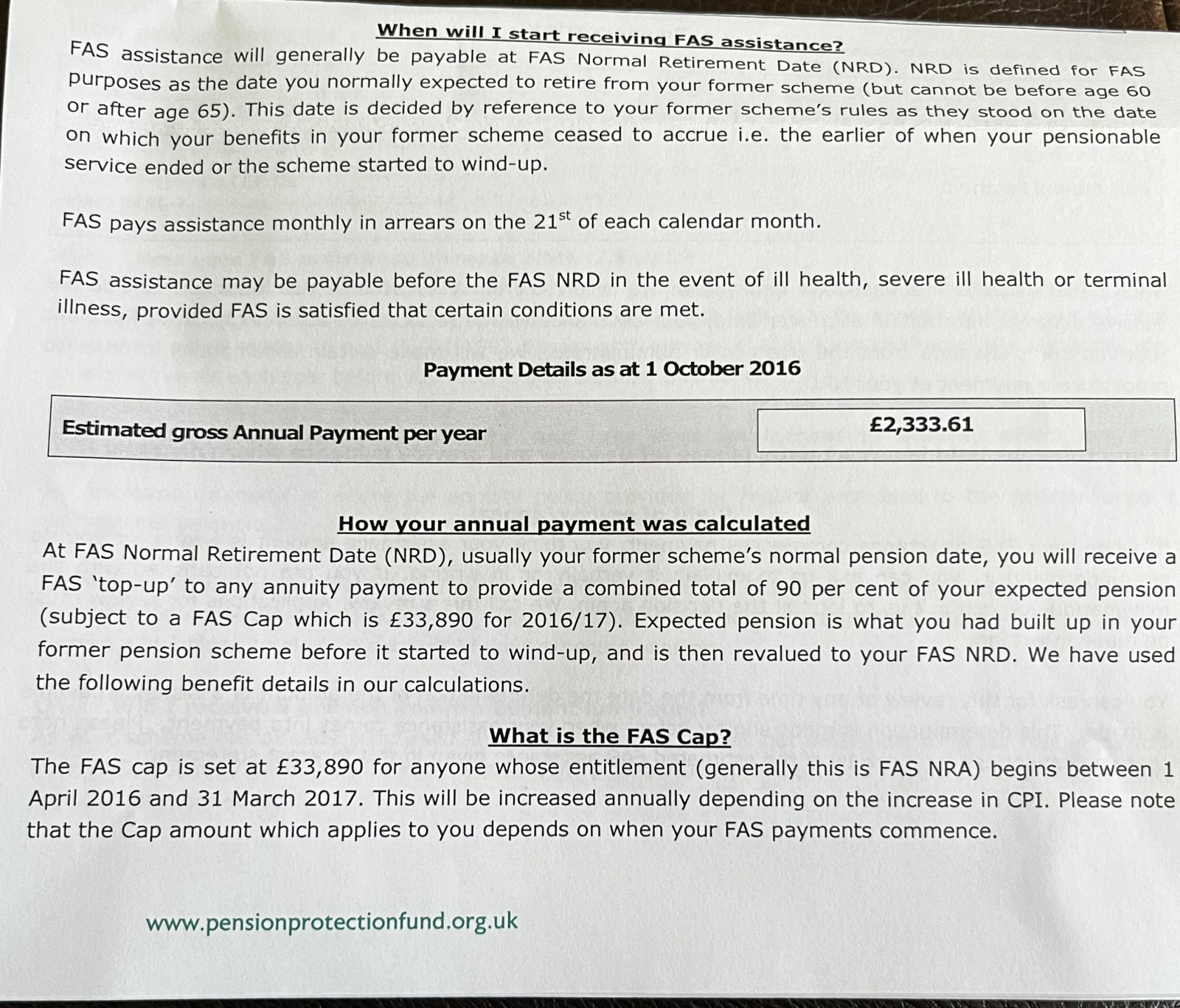

Here is an extract from a letter received from Financial Assistance Service in October 2016 -

0 -

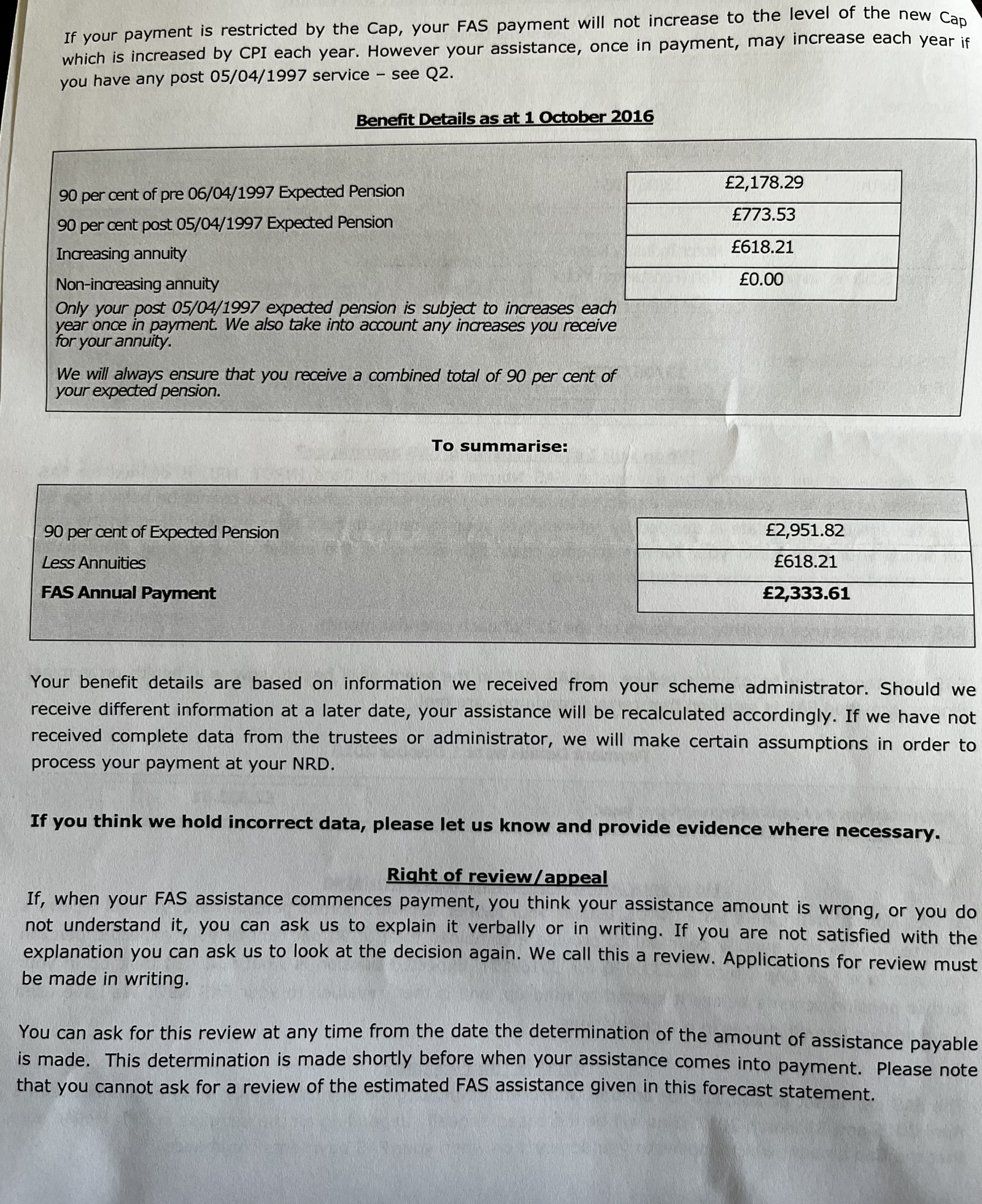

Here is a further extract from the FAS dated October 2016 -

0 -

Here is an extract from a letter from L&G in September 2016-

0 -

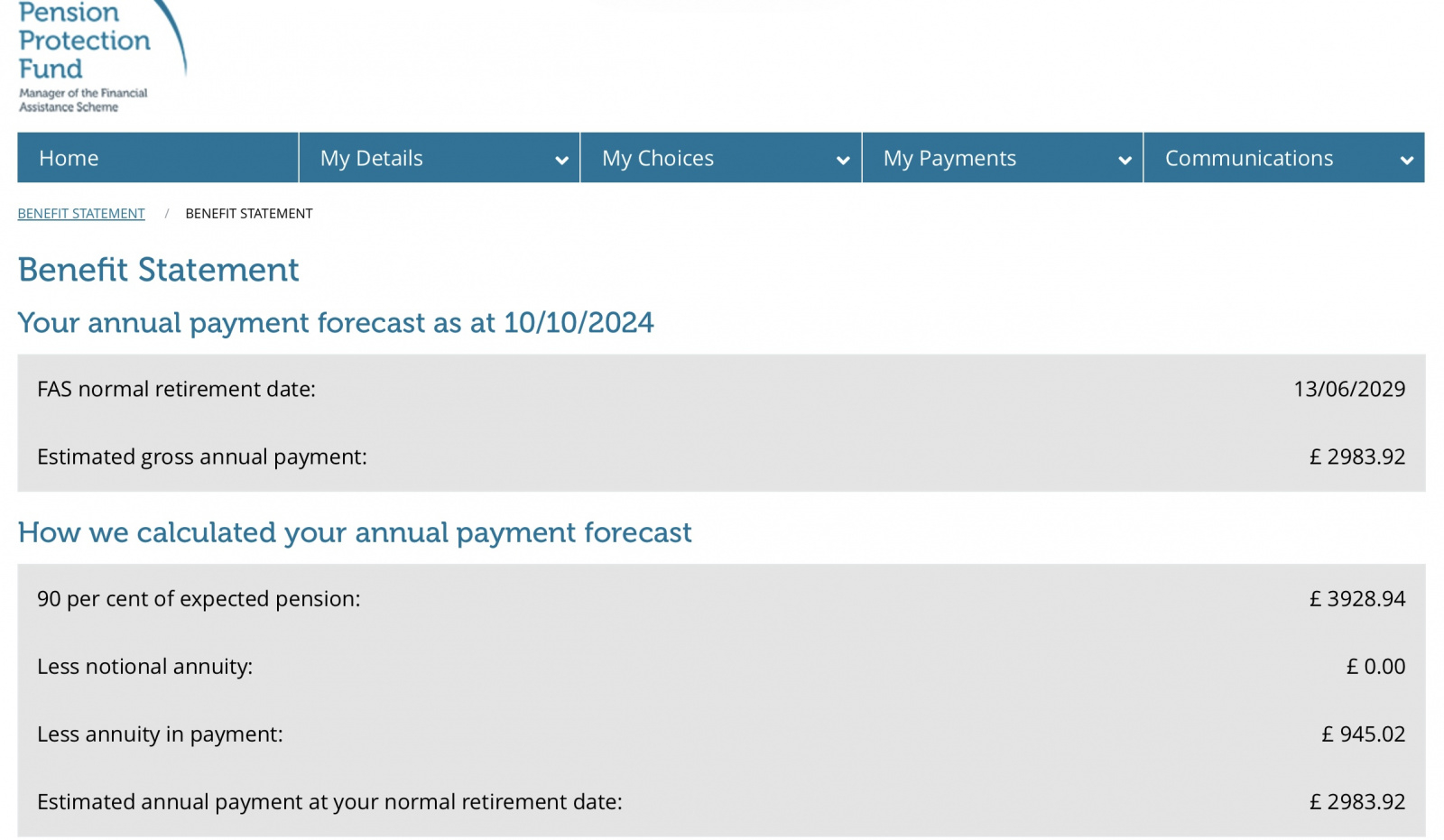

I have just created an account on the FAS members website and can see the following information -

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards