We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

DB Pension - Options available - either take annual value or transfer to another provider

Comments

-

Good afternoon everyone, thank you again for your replies. Apologies, but the latest replies have gone over my head.

i have found some paper work for this pension. I am not sure if what I have shared is of use, we moved home in 2000 and I haven’t found anything newer yet.

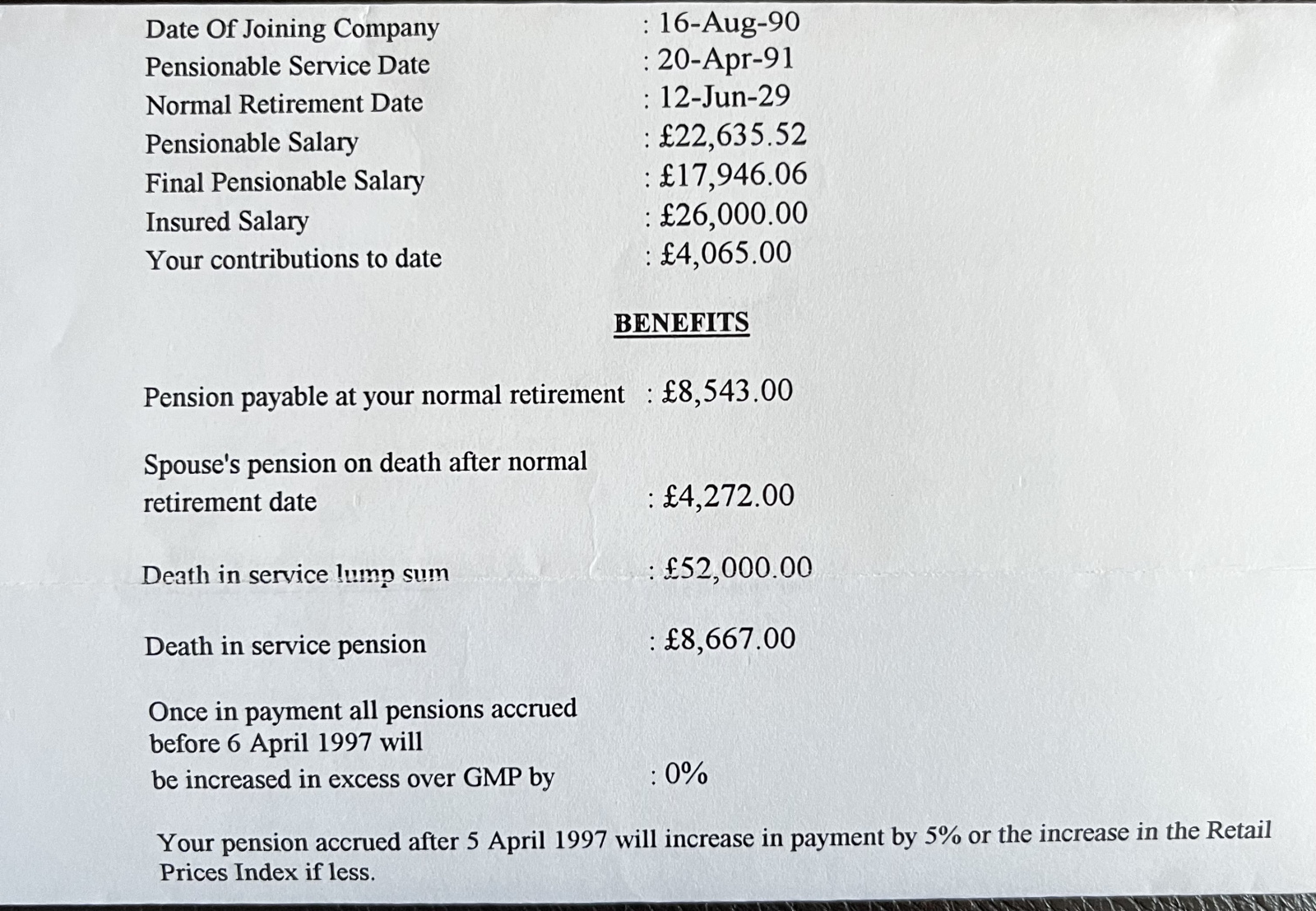

apologies again but I couldn’t work out how to share them in one post. This snip is from a letter with a Summary of Benefits as at 6th April 1998 -

0 -

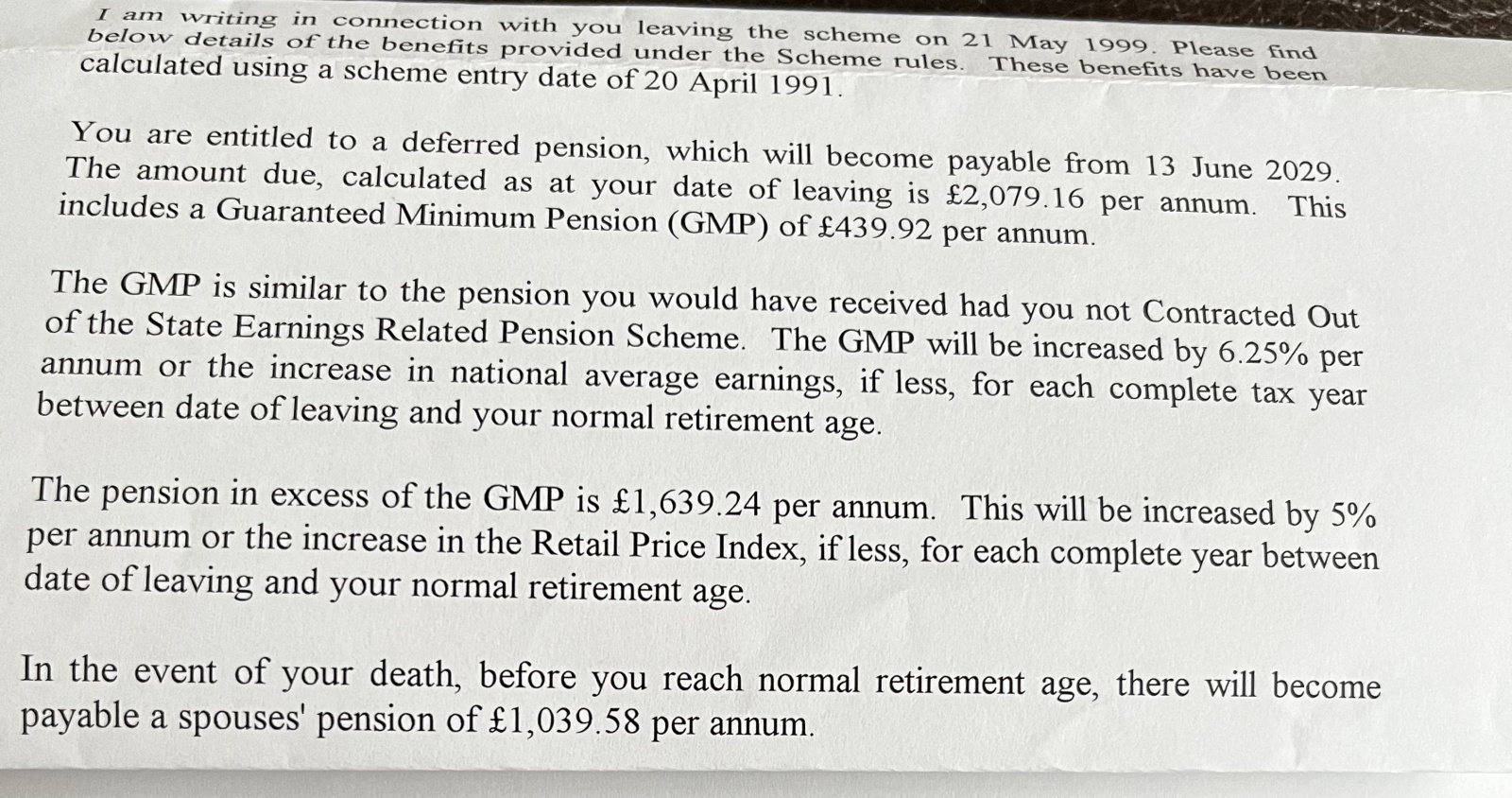

This is from a letter received in July 1999 -

0 -

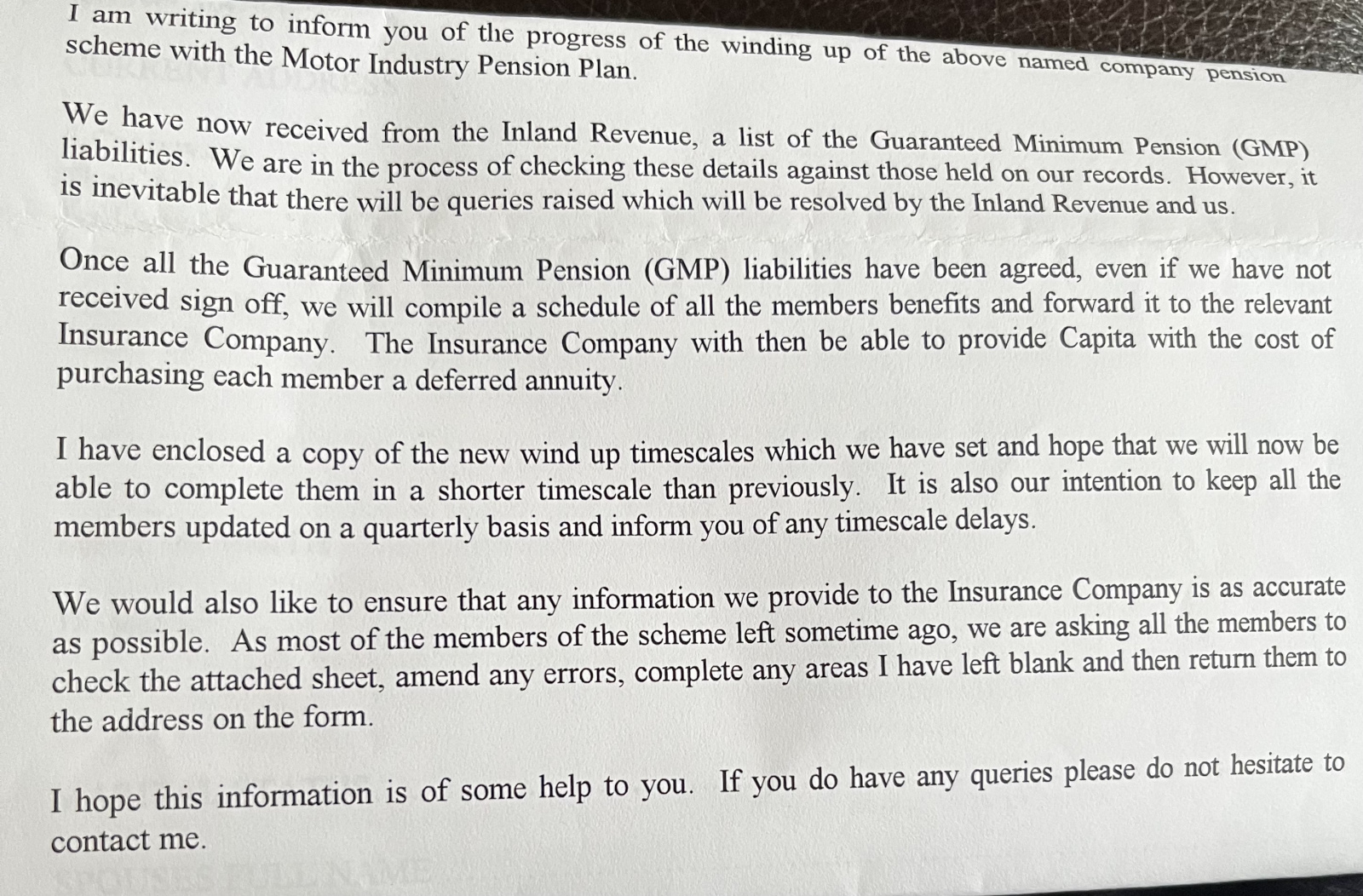

Finally, this is from a letter received in February 2000. -

0 -

As far as I can see, when you left in 1999, the scheme (administered by Capita?) was still open - you were given a statement of deferred benefits on leaving.

However, within a year or so of your departure, the Trustees commenced wind up ( was the Scheme underfunded?)

Pension liabilities (especially the GMP which was the least the scheme had an obligation to provide, see link in my previous) needed to be calculated.

This would enable Capita to approach an insurer regarding issuing pensioners with individual policies to secure their benefits.

These were deferred annuity policies - a S32 (see link in my previous) was one such.

I note that the Scheme normal retirement age was 65 but as a female, your GMP age was 60.

As far as I understand it, what normally happened in such circumstances was that the GMP would revalue under the fixed rate (or by increase in National Average earnings if lower) up to age 60 and after that as explained in the GMP link I provided.

L&G has approached you with regard to commencing the pension at your GMP age.

Do you have the details of the benefits secured under your deferred annuity policy? Presumably you were provided with the policy document?

0 -

Thank you again Xylophone, I really do appreciate your ongoing help.

You are spot on with saying the scheme was administered by Capita, the correspondence I shared above has their details at the bottom of the page.

The business closed at the end of May 1999 as the managing director, and main shareholder, was retiring and he sold off the site to a housing developer. I left one week early to start another job.

i do think there was underfunding, i am frustrated that I cannot lay my hands on any other paperwork yet but i am still looking.Apologies again for my lack of understanding but when you ask “do you have the details of the benefits secured under your deferred annuity policy? Presumably you were provided with the policy document?” Is this a document from when I joined the scheme or one I received after Capita had received and analysed the details they mention in the letter?0 -

Apologies again for my lack of understanding but when you ask “do you have the details of the benefits secured under your deferred annuity policy? Presumably you were provided with the policy document?” Is this a document from when I joined the scheme or one I received after Capita had received and analysed the details they mention in the letter?

Do read through the two links in my previous.

The letter you received in 1999 indicates that the scheme was still open - it has all the appearance of a statement of benefits on leaving the scheme.

If I am interpreting the letter correctly, it seems that at the date of leaving you had

Post 88 GMP £439.92

Excess over GMP £1639.24

These amounts were to revalue in deferment as indicated in the letter.

However. the Trustees of the Scheme decided to enter wind up.

You will note from the above

Key wind-up activities

The key activities you should complete when winding up your DB scheme are:

............

- identifying the remaining non-pensioners’ share of assets and obtaining terms from an insurer to secure those deferred benefits

It appears that the insurer chosen was L&G.

Once this had been done, you should have received a communication from the insurer concerning your deferred annuity policy.

You do mention moving house - possibly the document was lost in the post/in the packing?

The scheme was obliged to pay you at least your revalued GMP at GMP age - if the pension you have been offered is supposed

to represent your revalued GMP, it seems rather low?

https://www.mandg.com/wealth/adviser-services/tech-matters/pensions/types-of-arrangement/section-320 -

Thank you again Xylophone.

It is possible that I am missing paperwork for one of the two reasons you mention. I will certainly continue to look for any additional paperwork.Is it likely that L&G will still have copies of any paperwork I am missing?0 -

I imagine that L&G must have some documentation to support their calculations.

Looking again at the letter of July 1999, the GMP revaluation method is unusual - see

https://www.barnett-waddingham.co.uk/comment-insight/blog/what-is-a-gmp/The GMP must be increased for each complete tax year in the period from leaving pensionable service to retirement or death. COSR schemes can adopt ONE of the following ways to revalue GMP.

The first way uses an index based on National Average Earnings, known as Section 148 Orders or ‘full rate’ revaluation. This is most common in public sector pension schemes. The Secretary of State will publish a Social Security Revaluation of Earnings Factors Order (known as 'Section 148 orders') each year specifying the minimum increase that must be applied to each member’s GMP which is based on National Average Earnings.

The other way to revalue GMPs is the ‘fixed rate' method. This allows for an administrator to calculate the likely amount of GMP payable at retirement as the level of increase is already known. The amount of fixed rate revaluation depends on the date the member left contracted out service

You would have expected that from the outset either the GMP revalued at Fixed Rate OR it revalued at Full Rate , not one or the other depending on which was lower (see above under GMP revaluation).

I think that we must assume that the scheme was underfunded so that the Trustees secured only what they were obliged to, ie the GMP.

It is possible that the S32 you seem to have been issued revalues under the same terms as the original scheme but even if NAE was used throughout, the pension you have been offered seems on the low side - no doubt L&G can clarify.

Or perhaps Firedreamer has the relevant tables.

The method chosen does make a difference - see this from a determination of the Pensions Ombudsman some years ago - it was in respect of the merging of periods of service (not relevant to your case) but the comment on revaluation may well be.· An advantage to keeping the two periods of membership separate is that you can take the pensions at different times. If you join the records you will have one pension and one opportunity to take it.

· One further issue to consider is the effect merging the records will have on your Guaranteed Minimum Pension (GMP). This is the minimum pension that the scheme must provide for contracted-out service before 6 April 1997. The GMP you accrued during your first period of service was £798.72 per annum. At your State Pension Age the Scheme must ensure that the total pension you receive in respect of your first period of service is at least equal to the GMP revalued by 6.25% (fixed rate revaluation) for each year from 5 April 1999 to 5 April 2023. This equals £3422.12 per annum at State Pension Age.

If you decide to merge your records we would have to revalue your GMP by section 148 orders. This method of revaluation is based on the increase in national average earnings and it is therefore impossible to predict what the GMP would be at State Pension Age. As a guide, however, the increase in earnings has not risen above 4% in the past few years and so at present this would result in a lower GMP at State Pension Age. This may well be a lower amount than what your revalued GMP would be for your first period of service if you kept the pensions separate.”

0 -

What has happened to the excess over the GMP payable in 2029?

It cannot just disappear by being covered by increases in the GMP - anti franking regulations see to that.

If there is a pension fund shortfall, the pension fund cannot be wound up - unless maybe the employer has become insolvent. But then the FAS or PPF would apply?

.1 -

Thank you again Xylophone and FIREDreamer.

I will have the opportunity look into the information within your replies later on.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards