We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Easy access & regular savings - working out the maths

Comments

-

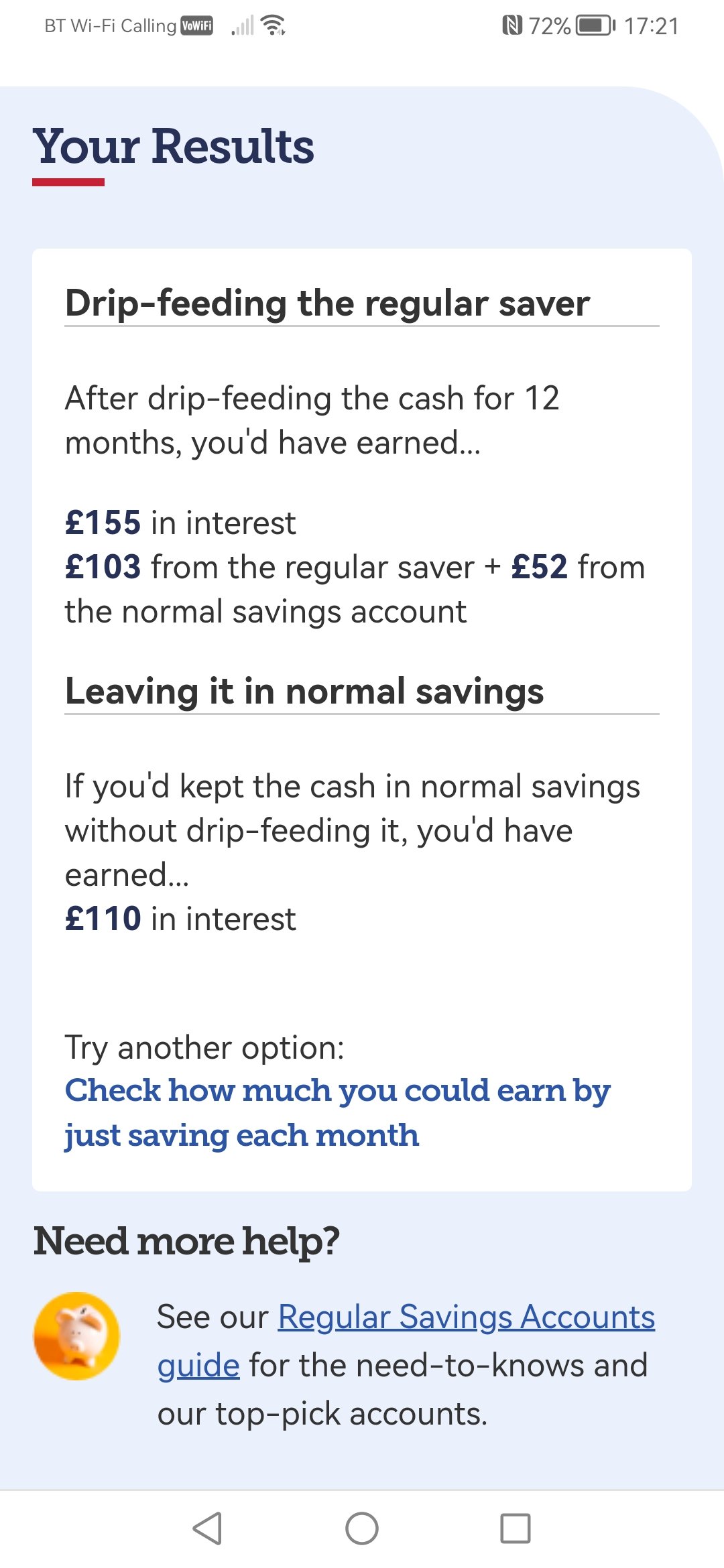

This is from the MSE calculator, using the OP's numbers and the "drip feed" option.3 -

With the amount of information available around this, it surprises me that this subject causes such confusion. 8% is 3.35% more than 4.65% so it’s better.

If you had £1200 and left it in a 4.65% account for a year you would get £55.80 Interest.

If instead you drip fed £100 of that per month into the RS, it would reduce to c£27.90 interest on the 4.65% account but in addition you would get £48 interest on the RS so a total of £75.90 interest. You’re therefore £20.10 better off.

Operating a number of RS accounts in conjunction with EA if you already have a lump sum can be profitable. They are also a good option if yo7 have a fixed sum to save each month.Understand why it’s confusing but the mistake people make is to think of the overall annual interest on a fixed amount over the course of a year rather than breaking it down.6 -

3k a month on Regular savers myself.They are just starting to payout this year, Keep the cash in my Chip ISA.Then fund regular savers on the First of the month, all except First Direct and Coventry.Just over £1300 from regular savers in interest, not sure on Chip yet.1

-

I understand the (minimal) benefit of drip feeding from an EA to a RS, although I don't bother with it personally. Just too much faf.

However, I can see the benefit of putting money into a RS each month from future wages, ie money you don't yet have, but know you will at the end of each month. That side does appear more appealing.1 -

martyp said:

Thanks, I did try that and it came back with £103 for the regular but can't see a comparison with leaving the money in the easy access for a year.friolento said:The MSE calculatorr should give you your answer https://www.moneysavingexpert.com/savings/regular-savings-calculator

The MSE calculator does tell you how much you would make if you left your money in the easy access account

1 -

Have your funds in the accounts paying the highest amount of interest available is the long and short of it. There is obviously a possible tax consideration, when funds inside a cash ISA with a lower rate might beat the net interest outside of the wrapper.

3 -

Any time you have money in an 8% interest account it is earning more than in a 4% or 5% account. Thats really the top and tail of it.7

-

I try to spread my regular savers out, so I have one or more maturing each month, and these then fund the following month's deposits into ongoing regular savers. Money sits in a flexible ISA when its not needed for regular savers, with the proviso that regular savers, after tax, pay at least the same % as the ISA.

And I have 0% debt on credit cards balancing the money in the regular saversI consider myself to be a male feminist. Is that allowed?3 -

Good strategy but must difficult to build. Most of them come sporadically and some of them don't offer any attractive follow up products. I currently run 38 RSs and still have some months of next year uncovered.surreysaver said:I try to spread my regular savers out, so I have one or more maturing each month, and these then fund the following month's deposits into ongoing regular savers. Money sits in a flexible ISA when its not needed for regular savers, with the proviso that regular savers, after tax, pay at least the same % as the ISA.

And I have 0% debt on credit cards balancing the money in the regular savers2 -

Agreed you have to take them when they appear, some are not around for long.allegro120 said:

Good strategy but must difficult to build. Most of them come sporadically and some of them don't offer any attractive follow up products. I currently run 38 RSs and still have some months of next year uncovered.surreysaver said:I try to spread my regular savers out, so I have one or more maturing each month, and these then fund the following month's deposits into ongoing regular savers. Money sits in a flexible ISA when its not needed for regular savers, with the proviso that regular savers, after tax, pay at least the same % as the ISA.

And I have 0% debt on credit cards balancing the money in the regular saversI choose the rooms that I live in with care,

The windows are small and the walls almost bare,

There's only one bed and there's only one prayer;

I listen all night for your step on the stair.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards