We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Small Pension Pots

Comments

-

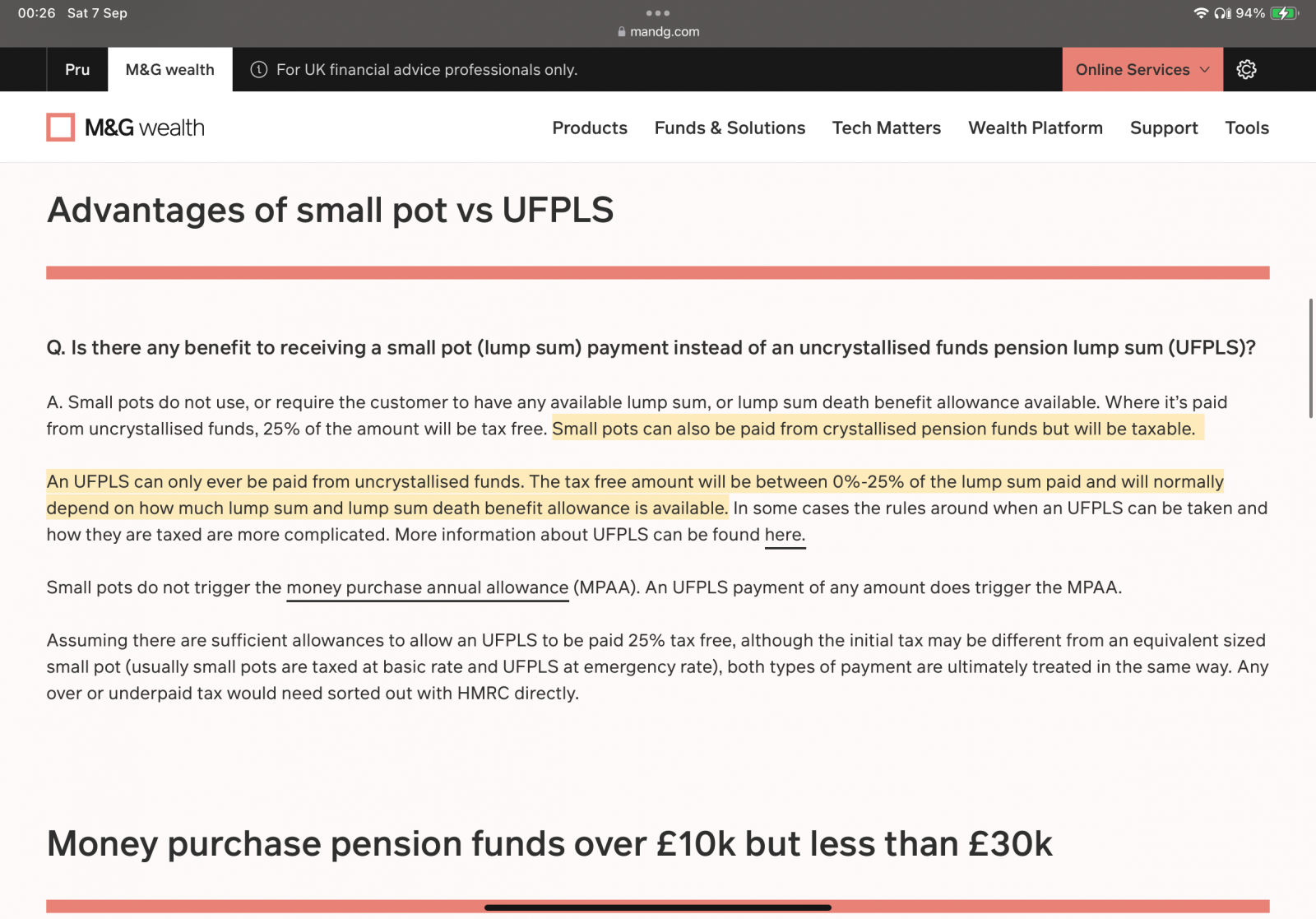

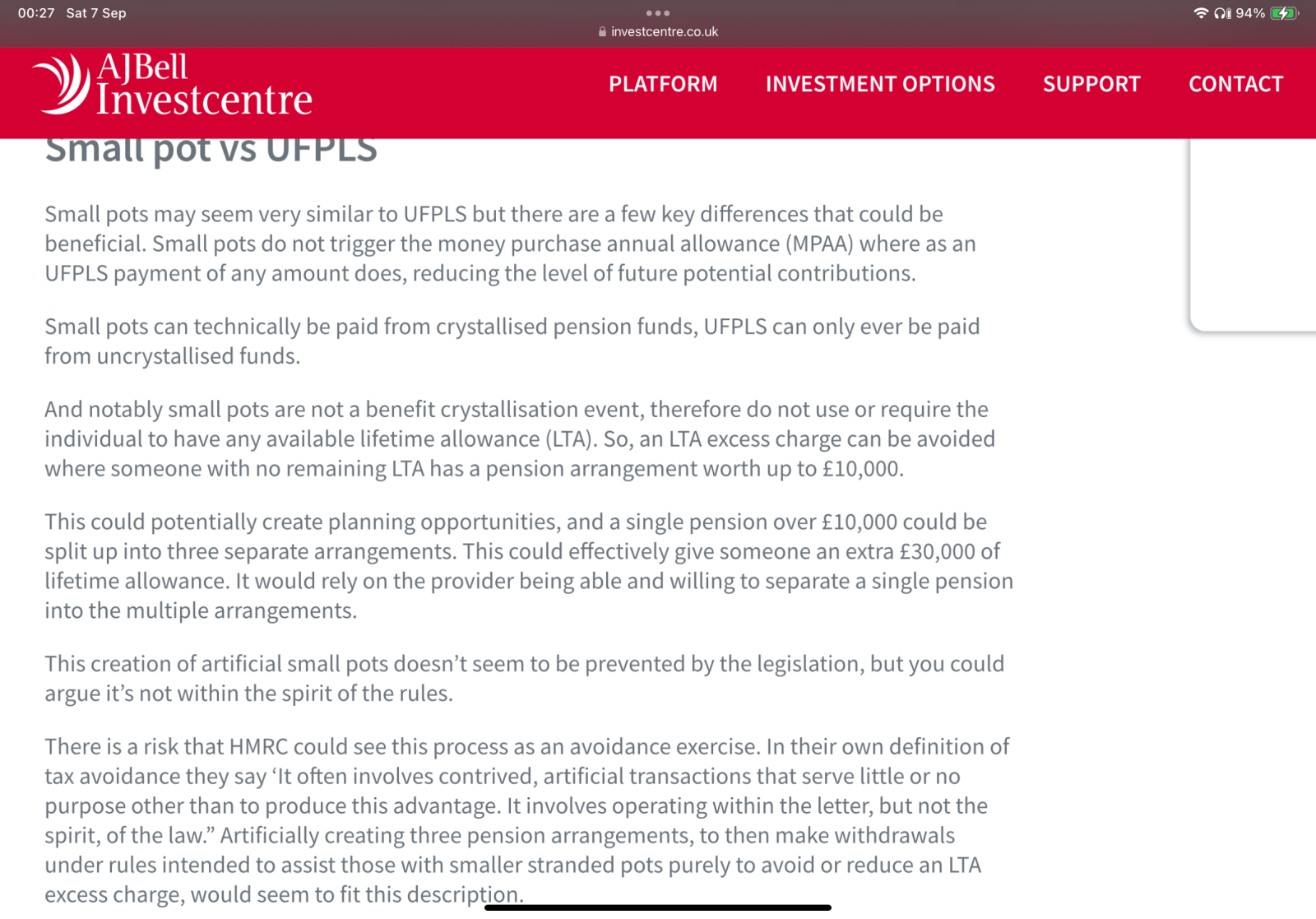

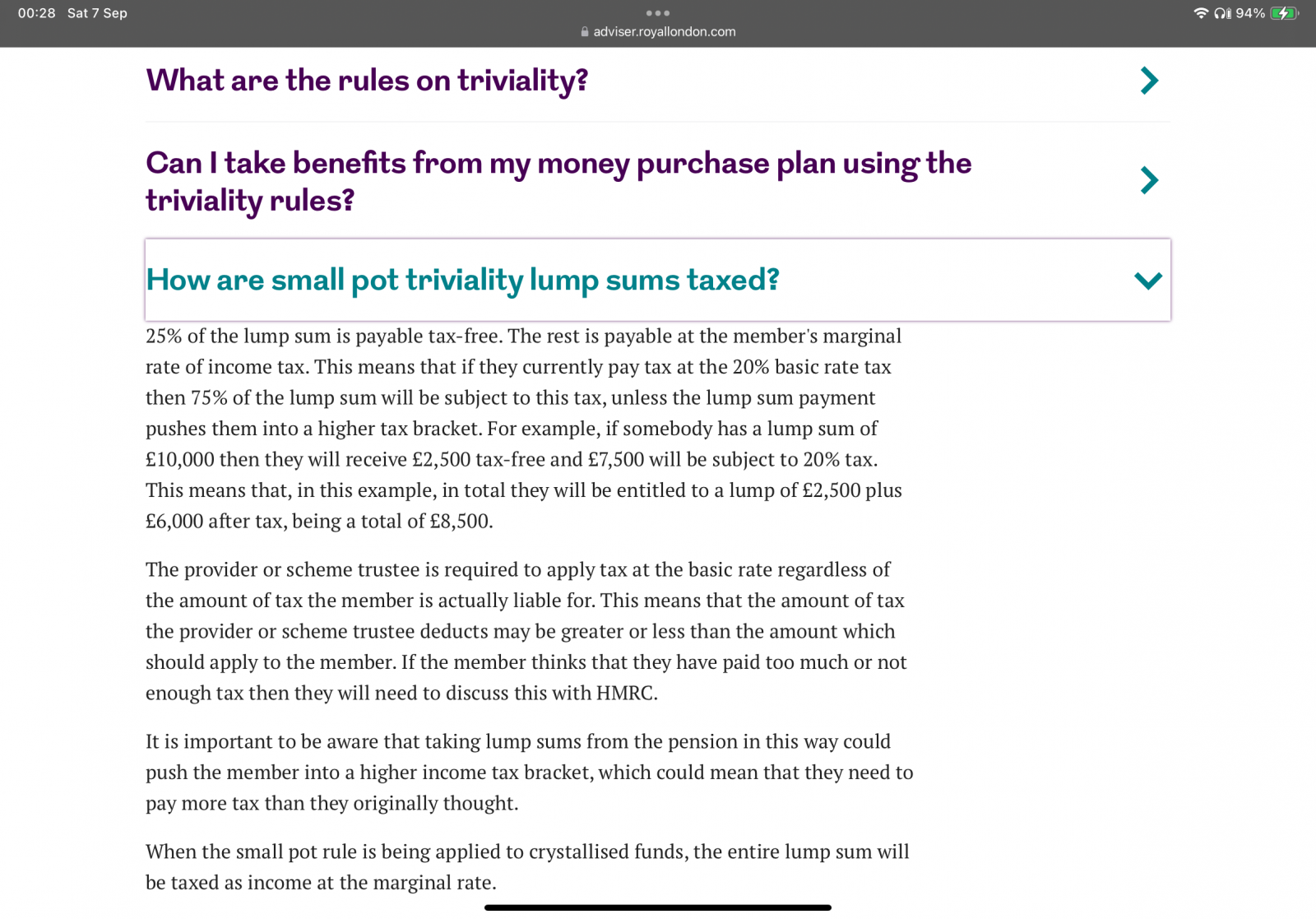

Not trying to be controversial, but it seems like other providers suggest it’s possible to take small pots from crystallised pensions, three examples …

(1) M&G Wealth (2) AJ Bell

(2) AJ Bell

(3) Royal London 1

1 -

It's both interesting and confusing. I also spoke to AJ Bell who said it couldn't be done from crystallized funds, it would be income and trigger the MPAA. I might go back to them and ask why their phone advice contradicts their website! Is that a dig I spy, at pension providers who are happy to split a pension to create three 'artificial' small pots (AJ Bell won't do that) 😄FIREDreamer said:Not trying to be controversial, but it seems like other providers suggest it’s possible to take small pots from crystallised pensions, three examples …

(1) M&G Wealth(2) AJ Bell

(3) Royal London

0 -

Not controversial at all - every day's a school day in pensions! Why not do what Greenwaves has done and contact them direct, asking them to confirm the position, or correct their 'information' IF it's not accurate?FIREDreamer said:Not trying to be controversial, but it seems like other providers suggest it’s possible to take small pots from crystallised pensions, three examples …

(1) M&G Wealth(2) AJ Bell

(3) Royal London

Looking at this (and I've only had time for a quick glance), I suspect there are some very limited circumstances in which this can be done: https://www.gov.uk/hmrc-internal-manuals/pensions-tax-manual/ptm063700#xd_co_f=YjMzMTgxZTMtMTY5NC00ZTJiLWJjZTAtNDA0YzlkNmI5Y2Fk~

Notable that none of the IFAs who post on this website have joined this discussion with their views...it would be really helpful if they did. I'm not an IFA and spend virtually all my time in the world of occupational schemes, but hopefully they are much more hands on with small pots.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

The pension advice service inform me (they had to check with their back office), that an uncrystallized pension 10k or less can be taken as a small pot and not trigger the MPAA. However they also said whether your scheme provider will do that as a small pot is another matter. Each scheme provider makes up their rules within the confines of HMRC rules. But most definitely they said HMRC rules allow it.

This was not their initial advice but I pressed them to look more deeply, quoting HMRC rules and M and G interpretations. They went off to research and check and phoned me back with the above answer.

So it seems you can and you can't dependant on your pension provider.0 -

What about a crystallised pot of £10k?Greenwaves said:The pension advice service inform me (they had to check with their back office), that an uncrystallized pension 10k or less can be taken as a small pot and not trigger the MPAA. However they also said whether your scheme provider will do that as a small pot is another matter. Each scheme provider makes up their rules within the confines of HMRC rules. But most definitely they said HMRC rules allow it.

This was not their initial advice but I pressed them to look more deeply, quoting HMRC rules and M and G interpretations. They went off to research and check and phoned me back with the above answer.

So it seems you can and you can't dependant on your pension provider.0 -

The rule is <= to 10k, therefore a crystallized pot of 10k can be taken as a small pot, but not £10,001.FIREDreamer said:

What about a crystallised pot of £10k?Greenwaves said:The pension advice service inform me (they had to check with their back office), that an uncrystallized pension 10k or less can be taken as a small pot and not trigger the MPAA. However they also said whether your scheme provider will do that as a small pot is another matter. Each scheme provider makes up their rules within the confines of HMRC rules. But most definitely they said HMRC rules allow it.

This was not their initial advice but I pressed them to look more deeply, quoting HMRC rules and M and G interpretations. They went off to research and check and phoned me back with the above answer.

So it seems you can and you can't dependant on your pension provider.0 -

That’s what I thought originally, thanks.Greenwaves said:

The rule is <= to 10k, therefore a crystallized pot of 10k can be taken as a small pot, but not £10,001.FIREDreamer said:

What about a crystallised pot of £10k?Greenwaves said:The pension advice service inform me (they had to check with their back office), that an uncrystallized pension 10k or less can be taken as a small pot and not trigger the MPAA. However they also said whether your scheme provider will do that as a small pot is another matter. Each scheme provider makes up their rules within the confines of HMRC rules. But most definitely they said HMRC rules allow it.

This was not their initial advice but I pressed them to look more deeply, quoting HMRC rules and M and G interpretations. They went off to research and check and phoned me back with the above answer.

So it seems you can and you can't dependant on your pension provider.0 -

Yes, but although HMRC allows it good luck finding a pension provider whose scheme implements it for crystallized funds.FIREDreamer said:

That’s what I thought originally, thanks.Greenwaves said:

The rule is <= to 10k, therefore a crystallized pot of 10k can be taken as a small pot, but not £10,001.FIREDreamer said:

What about a crystallised pot of £10k?Greenwaves said:The pension advice service inform me (they had to check with their back office), that an uncrystallized pension 10k or less can be taken as a small pot and not trigger the MPAA. However they also said whether your scheme provider will do that as a small pot is another matter. Each scheme provider makes up their rules within the confines of HMRC rules. But most definitely they said HMRC rules allow it.

This was not their initial advice but I pressed them to look more deeply, quoting HMRC rules and M and G interpretations. They went off to research and check and phoned me back with the above answer.

So it seems you can and you can't dependant on your pension provider.0 -

I have taken 2 for £10k each from HL so far from uncrystallised pots. Next tax year I will take my third for about £9k (balance after adding £3,600 gross next April). I have about £11k LSA left to do the £3,600 pa top up to age 75 to get the remaining LSA out.Greenwaves said:

Yes, but although HMRC allows it good luck finding a pension provider whose scheme implements it for crystallized funds.FIREDreamer said:

That’s what I thought originally, thanks.Greenwaves said:

The rule is <= to 10k, therefore a crystallized pot of 10k can be taken as a small pot, but not £10,001.FIREDreamer said:

What about a crystallised pot of £10k?Greenwaves said:The pension advice service inform me (they had to check with their back office), that an uncrystallized pension 10k or less can be taken as a small pot and not trigger the MPAA. However they also said whether your scheme provider will do that as a small pot is another matter. Each scheme provider makes up their rules within the confines of HMRC rules. But most definitely they said HMRC rules allow it.

This was not their initial advice but I pressed them to look more deeply, quoting HMRC rules and M and G interpretations. They went off to research and check and phoned me back with the above answer.

So it seems you can and you can't dependant on your pension provider.

However any extras going into pension will be taxed at 40% on withdrawal (DB and annuity from now and SP in 7 years will use up all of 0% and 20% band leaving loads in crystallised pot even after taking full 20% band out as drawdown up to SPA) so not sure if this is worth it.0 -

It is not really the provider making up their own rules.Greenwaves said:The pension advice service inform me (they had to check with their back office), that an uncrystallized pension 10k or less can be taken as a small pot and not trigger the MPAA. However they also said whether your scheme provider will do that as a small pot is another matter. Each scheme provider makes up their rules within the confines of HMRC rules. But most definitely they said HMRC rules allow it.

This was not their initial advice but I pressed them to look more deeply, quoting HMRC rules and M and G interpretations. They went off to research and check and phoned me back with the above answer.

So it seems you can and you can't dependant on your pension provider.

some just do not offer it as demand is low and having the process in place is unprofitable.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards