We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

What's your portfolio?

Comments

-

I have a S&S ISA which is made up of the following 7 ETFs -

19% Xtrackers MSCI Nordic (distributing)

17% iShares Digital Security (distributing)

16% iShares MSCI Poland (accumulating)

14% Amundi Prime Japan (distributing)

14% L&G Clean Water (accumulating)

14% Amundi Global Gender Equality (accumulating)

6% iShares S&P Small Cap 600 (distributing)0 -

If you want global bond exposure but to have everything in the safe haven of the USD, AGGU/SAGG seem to let you have your cake and eat it. Presumably your answer would be "yes, but a diet of only cake is not healthy."masonic said:

There will be a lot of debt issued outside the US that is denominated in USD, and including that (rather than going for US Treasuries and corporates only) will improve your yield but provide the same currency effects, at the risk of credit spreads widening on those holdings during stress conditions. Global unhedged bonds, when paired with global cap-weighted equities, give rise to a lower ulcer index and higher baseline return in GBP than if you used intermediate duration gilts or US treasuries or combinations of the three. HSBC Global Strategy seems to use their own house global government and global corporate bond funds, and the version appears to be USD-hedged. iShares offers AGGU and SAGG, both at the same 0.1% OCF. Coming back to your question around the general (inc Monevator) recommendation to GBP-hedge, this is in the context of volatility reduction. So as with many things, it's different strokes for different folk, and some might prioritise a smooth ride, whereas others want an efficient frontier.aroominyork said:The factsheet for AGGG says 18.52% of holdings are US - although the top ten only total 52% with Germany in tenth place at 2.08%. Maybe HL's 31.24% for the US is more accurate. In either case, does this mean the 'rush to USD protection' only applies to 20%-30% of the holdings?Edit: This iShares site (Exposure breakdowns > Geography) says US 40.24% but the question stands.0 -

aroominyork said:

If you want global bond exposure but to have everything in the safe haven of the USD, AGGU/SAGG seem to let you have your cake and eat it. Presumably your answer would be "yes, but a diet of only cake is not healthy."masonic said:

There will be a lot of debt issued outside the US that is denominated in USD, and including that (rather than going for US Treasuries and corporates only) will improve your yield but provide the same currency effects, at the risk of credit spreads widening on those holdings during stress conditions. Global unhedged bonds, when paired with global cap-weighted equities, give rise to a lower ulcer index and higher baseline return in GBP than if you used intermediate duration gilts or US treasuries or combinations of the three. HSBC Global Strategy seems to use their own house global government and global corporate bond funds, and the version appears to be USD-hedged. iShares offers AGGU and SAGG, both at the same 0.1% OCF. Coming back to your question around the general (inc Monevator) recommendation to GBP-hedge, this is in the context of volatility reduction. So as with many things, it's different strokes for different folk, and some might prioritise a smooth ride, whereas others want an efficient frontier.aroominyork said:The factsheet for AGGG says 18.52% of holdings are US - although the top ten only total 52% with Germany in tenth place at 2.08%. Maybe HL's 31.24% for the US is more accurate. In either case, does this mean the 'rush to USD protection' only applies to 20%-30% of the holdings?Edit: This iShares site (Exposure breakdowns > Geography) says US 40.24% but the question stands.Haha, it probably would be. Hedging is imperfect and only works against forex movements. It doesn't protect against prices falling when the risk premium demanded for the underlying debt instruments increases because of their credit rating and fact they aren't actually denominated in USD. So I would not emphasise the safe haven aspects, rather it is the negative correlation that I'd be seeking. I prefer for my decisions to be data driven and I do not know if any studies have used such an esoteric asset as compared with the traditional local currency hedged or unhedged global variants, so some more research is probably warranted.If you play around with asset classes on Portfolio Finder (after selecting your home country as UK and switching from global ex-US to developed world), you'll be led into combinations that involve mixtures of equities vs a combination of US treasuries and gold. Switching to the portfolio matrix tool and adjusting this to something like 50% global blend, 10% global small cap value, 30% long US treasuries and 10% gold starts to resemble an inoffensive mix that could be said to improve upon the 60:40 portfolio, though less diversified in fixed interest. Problem is gold is looking pricey, so perhaps one to consider the next time it plummets. It is interesting that exchanging any amount of the US treasuries for 10 year gilts or global bonds makes the portfolio worse on a number of metrics.1 -

I don't disagree but l felt the shares were very cheap at the time of purchase. 55K job losses by 2030 and peak capex on our full fibre rollout suggests profits will improve significantly over time. The boards future strategy makes me very confident that further value will prevail.MX5huggy said:

😮 wow that’s a bold strategy.inflationbuster said:I am retired and hundred percent of my SIPP is in BT shares. It’s not 100 of my pension as l have a 2nd pension (company).0 -

A moment ago you said "Global unhedged bonds, when paired with global cap-weighted equities, give rise to a lower ulcer index and higher baseline return in GBP than if you used intermediate duration gilts or US treasuries or combinations of the three." (What's the third?). Doesn't that conflict with "It is interesting that exchanging any amount of the US treasuries for 10 year gilts or global bonds makes the portfolio worse on a number of metrics."?0

-

aroominyork said:A moment ago you said "Global unhedged bonds, when paired with global cap-weighted equities, give rise to a lower ulcer index and higher baseline return in GBP than if you used intermediate duration gilts or US treasuries or combinations of the three." (What's the third?). Doesn't that conflict with "It is interesting that exchanging any amount of the US treasuries for 10 year gilts or global bonds makes the portfolio worse on a number of metrics."?The three were global unhedged, intermediate gilts and US treasuries (paired with global cap-weighted equities). That's without gold. The inclusion of even a small allocation to gold reduces the ulcer index significantly, far more than the difference achievable through substitutions within bonds. What's interesting is that in the presence of 10% gold, the average and baseline return order switches to US > global > UK. However, you do give up a small proportion of the reduction in ulcer index gained through the addition of the gold. I suspect there is a diversification effect that is shared between gold and a currency diversified mix of bonds. Exposure to a variety of currencies would probably insure against periods where the US (or UK if using gilts and/or local currency hedging) has issues that don't have a domino effect over ROW, but gold tends to work in global crises too. The data used for this analysis goes back to 1970, so covers a variety of economic environments, but is less complete (but somewhat more comprehensive) than other sources.TL;DR: Global unhedged looks more favourable if you want to keep things simple and aren't tempted to include gold in your asset mix, otherwise US treasuries tick more boxes.

1 -

With gold I've never got past the "no prospect of change in inherent value" argument but at the current price it's a no-go anyway. I'll have a good think about moving hedged global aggregate bond index and gilt index into unhedged global (although it messes with the CGT avoidance thread!). Many thanks as ever, masonic - you plug the bowlhead gap!

PS. I'm trying to work out, for those of us who are underweight US equities, whether unhedged bonds reinforce or offset that bias. I think they reinforce it?

PPS. Or maybe not. A strong US economy lifts its stock market and might strengthen the dollar. A stronger dollar increases the Sterling value of unhedged bonds so might partially offset the underweight equities. (It's complicated, this stuff...)0 -

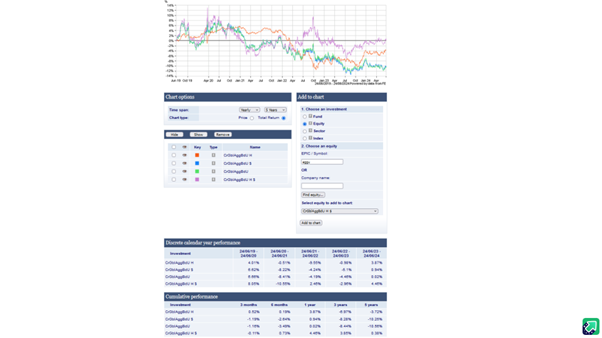

So looking at the options (sorry for the small image - I am not good at this) all four of which hold the same underlying assets:AGBP/green is the hedged versionAGGG/blue is unhedged and priced in USDSAGG/green is unhedged and priced in GBPAGGU/purple is fully hedged to USD and priced in USD.AGGU seems to be the ultimate 'USD safe haven' fund. AGGG is priced in USD so (at least on Interactive Investor) you are hit with a chunky forex margin rate charge (1.5% on amounts under £25k). SAGG is the Sterling version so it seems the best option.

0 -

Interesting thread, something I haven't really considered for a while. Turns out the split of assets falls like this:

Category Percent GIA 34% ISA 9% JISA 2% PENSION 11% SAVINGS 26% GILTS 17%

* The GIA is essentially global index funds plus about 10-15% active bits.

* The ISAS are a mix of about 50% global index and 50% active - mostly punts all over the place, the vast majority have not done too well! - Hence the GIA being mostly passive

* JISAS are mostly passive Global index funds, some active bets

* Pension is actually managed by Scottish Widows but quite low fee, will get round to moving it over to a SIPP at some point!

* Gilts mature in 2025,6,8 and are intended as savings proxies

* Savings are a mix of fixes up to 5 years, easy access, premium bonds, current accounts etc

Best fund of the bunch? RL Global Equity Select - 50% return so far. Sadly the whole team have left the fund pretty recently, so the future is uncertain to say the least!

1 -

I use that fund too and heard about the team leaving. I'll have a look at their new offering when it surfaces and probably move funds to there. It's one of the reasons many people don't like active funds - you do need to keep an eye on them!ChilliBob said:

Best fund of the bunch? RL Global Equity Select - 50% return so far. Sadly the whole team have left the fund pretty recently, so the future is uncertain to say the least!1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards