We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is the State Pension enough to live on if you are single !!

Comments

-

It’s from the IFS, here:Linton said:

I am sure that you would not want to mislead your readers. I cannot find a reference for the 1/4 of retired peope being millionaires you quote but it would seem that the figures are in wealth/household not per person. However if your look at https://www.nimblefins.co.uk/savings-accounts/average-household-savings-uk you will get a clearer picture:BlackKnightMonty said:Mustbeananswer?? said:

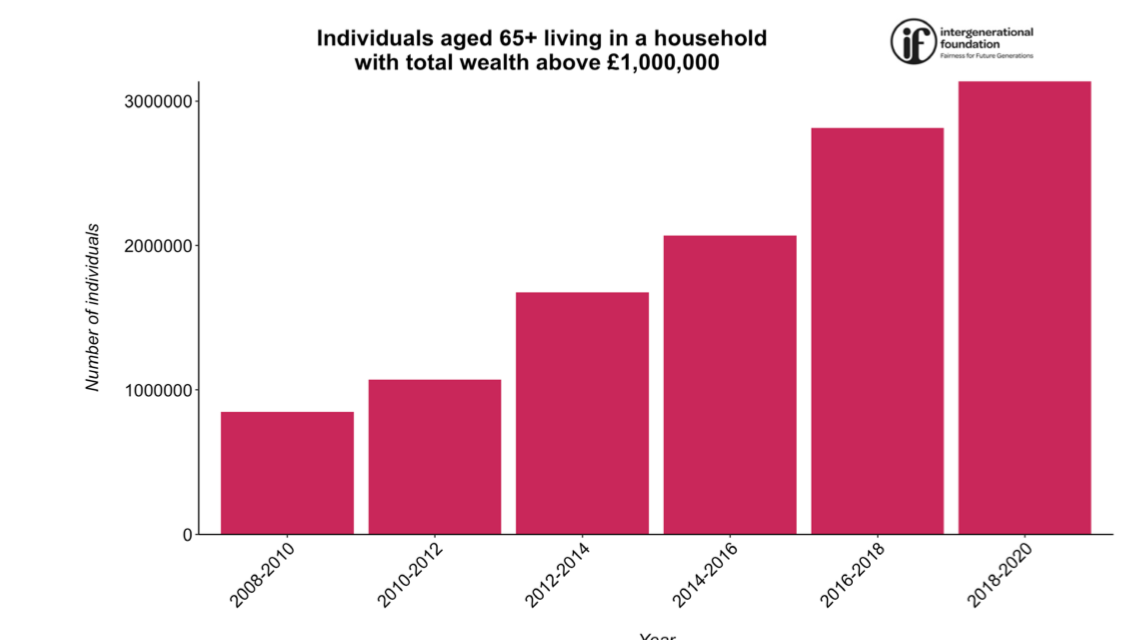

Disgrace....even after a good hike upwards .....In 2024-25, the full level of the new state pension is £221.20 a week or £11,502.40 a year.Pensioners are not given enough just to survive (If they have no other Occupational Pensions in place they are £2500 behind the eight ball) No wonder we have 1.5 million Pensioners in debt Come on England...give us a break ??GibbsRule_No3. said:My SP just about covers my HA rent, as I live in a London Borough, it does not cover my Council Tax, so I'd say no. I do have other pensions and am still working, nearly 70, my choice, for two days a week. Went to a Pension talk last week and they reckon to survive you need £14,000, fairly comfortable was £30,000 and very comfortable was over £40,000 this was based on one person, they did say you did not need to double those numbers for two people. At present with working pay I am just a bit over fairly comfortable and when I stop I won't be as low as surviving, thanks to the other pensions already in payment.And a quarter of all pensioners are millionaires.

Maybe we should means test it and then only those with no other pension provision, or those whom have not been able to make any other retirement provision could obtain a higher SP; perhaps quadruple locked to the NMW/NLW?

Does that sound fair?

For people of age 65+:........

I) The statistics here are in wealth per person, not wealth per household.

2) The wealth includes net value of house. Obviously people who have been paying off mortgages for perhaps and 30 years are going to have much higher net worth of houses than those who have only being doing this for 10 years.

3) The wealth also includes the value of non-state pensions in payment. Clearly a pension that is going to last you say 25 years is going to amount to a large sum of money.

4) Also included is the value of assets such as cars, furniture, ornaments, jewelry etc etc. But one accumulates stuff over the years so the older you are the greater value of stuff.

5) The average liquid wealth eg savings and non pension investments amounts to about £39,200. So hardly rolling in money. Again this is after a lifetime of work.

Now looking at the median annual gross income for people aged 65+ given in: https://www.gov.uk/government/statistics/distribution-of-median-and-mean-income-and-tax-by-age-range-and-gender-2010-to-2011. This gives a figure of about £22K, similar to the minimim wage. This is less than during any 5 year period in the age range 26-64.

Again your story about OAPs living in luxury at the expense of younger people is simply not demonstrated by the statistics.

https://www.if.org.uk/wp-content/uploads/2022/06/pensioner_millionaires_FINAL.pdf

I mention it because one way to raise the SP for those who have no financial wealth as a cushion is to means test it; and effectively the really wealthy pensioners who don’t really need the SP can see that money redistributed.

1 -

That's looks to be household wealth so numbers will be skewed, also I assume that includes all assets, e.g. property which isn't particularly useful as you need to live somewhereBlackKnightMonty said:

It’s from the IFS, here:Linton said:

I am sure that you would not want to mislead your readers. I cannot find a reference for the 1/4 of retired peope being millionaires you quote but it would seem that the figures are in wealth/household not per person. However if your look at https://www.nimblefins.co.uk/savings-accounts/average-household-savings-uk you will get a clearer picture:BlackKnightMonty said:Mustbeananswer?? said:

Disgrace....even after a good hike upwards .....In 2024-25, the full level of the new state pension is £221.20 a week or £11,502.40 a year.Pensioners are not given enough just to survive (If they have no other Occupational Pensions in place they are £2500 behind the eight ball) No wonder we have 1.5 million Pensioners in debt Come on England...give us a break ??GibbsRule_No3. said:My SP just about covers my HA rent, as I live in a London Borough, it does not cover my Council Tax, so I'd say no. I do have other pensions and am still working, nearly 70, my choice, for two days a week. Went to a Pension talk last week and they reckon to survive you need £14,000, fairly comfortable was £30,000 and very comfortable was over £40,000 this was based on one person, they did say you did not need to double those numbers for two people. At present with working pay I am just a bit over fairly comfortable and when I stop I won't be as low as surviving, thanks to the other pensions already in payment.And a quarter of all pensioners are millionaires.

Maybe we should means test it and then only those with no other pension provision, or those whom have not been able to make any other retirement provision could obtain a higher SP; perhaps quadruple locked to the NMW/NLW?

Does that sound fair?

For people of age 65+:........

I) The statistics here are in wealth per person, not wealth per household.

2) The wealth includes net value of house. Obviously people who have been paying off mortgages for perhaps and 30 years are going to have much higher net worth of houses than those who have only being doing this for 10 years.

3) The wealth also includes the value of non-state pensions in payment. Clearly a pension that is going to last you say 25 years is going to amount to a large sum of money.

4) Also included is the value of assets such as cars, furniture, ornaments, jewelry etc etc. But one accumulates stuff over the years so the older you are the greater value of stuff.

5) The average liquid wealth eg savings and non pension investments amounts to about £39,200. So hardly rolling in money. Again this is after a lifetime of work.

Now looking at the median annual gross income for people aged 65+ given in: https://www.gov.uk/government/statistics/distribution-of-median-and-mean-income-and-tax-by-age-range-and-gender-2010-to-2011. This gives a figure of about £22K, similar to the minimim wage. This is less than during any 5 year period in the age range 26-64.

Again your story about OAPs living in luxury at the expense of younger people is simply not demonstrated by the statistics.

https://www.if.org.uk/wp-content/uploads/2022/06/pensioner_millionaires_FINAL.pdfIt's just my opinion and not advice.0 -

There is no skew. This is a lot of pensioner households who can afford not to receive the SP. And thereby boost the SP for others. They might need an equity withdrawal plan, but that’s quite a simple solution.SouthCoastBoy said:

That's looks to be household wealth so numbers will be skewed, also I assume that includes all assets, e.g. property which isn't particularly useful as you need to live somewhereBlackKnightMonty said:

It’s from the IFS, here:Linton said:

I am sure that you would not want to mislead your readers. I cannot find a reference for the 1/4 of retired peope being millionaires you quote but it would seem that the figures are in wealth/household not per person. However if your look at https://www.nimblefins.co.uk/savings-accounts/average-household-savings-uk you will get a clearer picture:BlackKnightMonty said:Mustbeananswer?? said:

Disgrace....even after a good hike upwards .....In 2024-25, the full level of the new state pension is £221.20 a week or £11,502.40 a year.Pensioners are not given enough just to survive (If they have no other Occupational Pensions in place they are £2500 behind the eight ball) No wonder we have 1.5 million Pensioners in debt Come on England...give us a break ??GibbsRule_No3. said:My SP just about covers my HA rent, as I live in a London Borough, it does not cover my Council Tax, so I'd say no. I do have other pensions and am still working, nearly 70, my choice, for two days a week. Went to a Pension talk last week and they reckon to survive you need £14,000, fairly comfortable was £30,000 and very comfortable was over £40,000 this was based on one person, they did say you did not need to double those numbers for two people. At present with working pay I am just a bit over fairly comfortable and when I stop I won't be as low as surviving, thanks to the other pensions already in payment.And a quarter of all pensioners are millionaires.

Maybe we should means test it and then only those with no other pension provision, or those whom have not been able to make any other retirement provision could obtain a higher SP; perhaps quadruple locked to the NMW/NLW?

Does that sound fair?

For people of age 65+:........

I) The statistics here are in wealth per person, not wealth per household.

2) The wealth includes net value of house. Obviously people who have been paying off mortgages for perhaps and 30 years are going to have much higher net worth of houses than those who have only being doing this for 10 years.

3) The wealth also includes the value of non-state pensions in payment. Clearly a pension that is going to last you say 25 years is going to amount to a large sum of money.

4) Also included is the value of assets such as cars, furniture, ornaments, jewelry etc etc. But one accumulates stuff over the years so the older you are the greater value of stuff.

5) The average liquid wealth eg savings and non pension investments amounts to about £39,200. So hardly rolling in money. Again this is after a lifetime of work.

Now looking at the median annual gross income for people aged 65+ given in: https://www.gov.uk/government/statistics/distribution-of-median-and-mean-income-and-tax-by-age-range-and-gender-2010-to-2011. This gives a figure of about £22K, similar to the minimim wage. This is less than during any 5 year period in the age range 26-64.

Again your story about OAPs living in luxury at the expense of younger people is simply not demonstrated by the statistics.

https://www.if.org.uk/wp-content/uploads/2022/06/pensioner_millionaires_FINAL.pdf1 -

The what ball?Mustbeananswer?? said:

Disgrace....even after a good hike upwards .....In 2024-25, the full level of the new state pension is £221.20 a week or £11,502.40 a year.Pensioners are not given enough.They dont have enough even to survive (If they have no other Occupational Pensions in place they are £2500 behind the eight ball) No wonder we have 1.5 million Pensioners in debt Come on England...give us a break ??GibbsRule_No3. said:My SP just about covers my HA rent, as I live in a London Borough, it does not cover my Council Tax, so I'd say no. I do have other pensions and am still working, nearly 70, my choice, for two days a week. Went to a Pension talk last week and they reckon to survive you need £14,000, fairly comfortable was £30,000 and very comfortable was over £40,000 this was based on one person, they did say you did not need to double those numbers for two people. At present with working pay I am just a bit over fairly comfortable and when I stop I won't be as low as surviving, thanks to the other pensions already in payment.0 -

I have downsized already to reconcile an interest only Mortgage...

The next step is to see whether I can find some Part Time Work within walking distance...this has not proved too fruitful yet.Gizzajob??

My new house (Freehold...not a flat) is not Buckingham Palace but has all the amenities I need to survive.When all was settled I have a small Contingency Fund.I am expecting the Full State Pension first payment within days and have approx £300 monthly in occ pens.

I need to knock down my Monthly spend considerably and I think the car will be the first casualty.My worry is that the contingency fund will reduce over time (Im only 66 ).I have been hyperactive since a child and the walls can close in on you.The days and evenings are very long.

My interest Only Mortgage was with Santander and the plight of many with one of their Interest Only Mortgages carried into Retirement is covered in the article attached.

https://www.thisismoney.co.uk/money/mortgageshome/article-3686044/Santander-borrowers-switch-lifetime-mortgage-rates-starting-just-2-96.html

0 -

BlackKnightMonty said:

There is no skew. This is a lot of pensioner households who can afford not to receive the SP. And thereby boost the SP for others. They might need an equity withdrawal plan, but that’s quite a simple solution.SouthCoastBoy said:

That's looks to be household wealth so numbers will be skewed, also I assume that includes all assets, e.g. property which isn't particularly useful as you need to live somewhereBlackKnightMonty said:

It’s from the IFS, here:Linton said:

I am sure that you would not want to mislead your readers. I cannot find a reference for the 1/4 of retired peope being millionaires you quote but it would seem that the figures are in wealth/household not per person. However if your look at https://www.nimblefins.co.uk/savings-accounts/average-household-savings-uk you will get a clearer picture:BlackKnightMonty said:Mustbeananswer?? said:

Disgrace....even after a good hike upwards .....In 2024-25, the full level of the new state pension is £221.20 a week or £11,502.40 a year.Pensioners are not given enough just to survive (If they have no other Occupational Pensions in place they are £2500 behind the eight ball) No wonder we have 1.5 million Pensioners in debt Come on England...give us a break ??GibbsRule_No3. said:My SP just about covers my HA rent, as I live in a London Borough, it does not cover my Council Tax, so I'd say no. I do have other pensions and am still working, nearly 70, my choice, for two days a week. Went to a Pension talk last week and they reckon to survive you need £14,000, fairly comfortable was £30,000 and very comfortable was over £40,000 this was based on one person, they did say you did not need to double those numbers for two people. At present with working pay I am just a bit over fairly comfortable and when I stop I won't be as low as surviving, thanks to the other pensions already in payment.And a quarter of all pensioners are millionaires.

Maybe we should means test it and then only those with no other pension provision, or those whom have not been able to make any other retirement provision could obtain a higher SP; perhaps quadruple locked to the NMW/NLW?

Does that sound fair?

For people of age 65+:........

I) The statistics here are in wealth per person, not wealth per household.

2) The wealth includes net value of house. Obviously people who have been paying off mortgages for perhaps and 30 years are going to have much higher net worth of houses than those who have only being doing this for 10 years.

3) The wealth also includes the value of non-state pensions in payment. Clearly a pension that is going to last you say 25 years is going to amount to a large sum of money.

4) Also included is the value of assets such as cars, furniture, ornaments, jewelry etc etc. But one accumulates stuff over the years so the older you are the greater value of stuff.

5) The average liquid wealth eg savings and non pension investments amounts to about £39,200. So hardly rolling in money. Again this is after a lifetime of work.

Now looking at the median annual gross income for people aged 65+ given in: https://www.gov.uk/government/statistics/distribution-of-median-and-mean-income-and-tax-by-age-range-and-gender-2010-to-2011. This gives a figure of about £22K, similar to the minimim wage. This is less than during any 5 year period in the age range 26-64.

Again your story about OAPs living in luxury at the expense of younger people is simply not demonstrated by the statistics.

https://www.if.org.uk/wp-content/uploads/2022/06/pensioner_millionaires_FINAL.pdf

Not such a simple solution. Equity release in your 70's is limited to about 1/3 of the value of the house. The current average house price is £264K, so you are talking about a lump sum of around £80K-£90K. Hardly enough to give your household £11K/year or more likely 2X£11K per year income to replace SP. Plus ER companies are not prepared to lend money on every house.

Buying an annuity at around 70 equivalent to SP inflation linked until death would cost around £200K/person. According to the ONS as quoted by Nutmeg the average pension pot at 55-64 is currently £107K so being able to afford to pay for SP and still generate sufficient income left to live a reasonable basic life style would be way beyond the means of the large majority of pensioners.

Perhaps circumstances may be different in say 40 years time when the changes to pensions brought in over the past 10 years will be having a significant effect on pensioner wealth but in a much shorter time perod, no way.

0 -

The problem with those auto enrolment pension is the implication that they will be enough when even a basic calculation shows that they will not be. With the number of job changes now & the few months at the beginning of each without payments in that will be another shortfall. The rate is only 8% which to work would have to be paid from age 16. How many people now start work at 16?

0 -

If you u means test state pension, people will just make sure they don't try too hard. The same way couples earning four times my salary between them will make sure that they can still claim child benefit that they don't need.

In fact it could have larger implications for the economy too, as people stop striving to earn more. It would just be seen as another tax, and people like to avoid tax.

The governments current plan of keeping the personal tax allowance low is doing a great job already of taxing people who have made an effort to have more income in retirement!Think first of your goal, then make it happen!0 -

If they had higher wages, they wouldn't need benefits. Do you not understand that lots of people on benefits have jobs?BlackKnightMonty said:

Or maybe expect/take less benefits/services?kimwp said:

Wages need to be higher for people to pay more tax.BlackKnightMonty said:

This is the situation today. Back in 1977 only 37% pf households took more from benefits/services than they contributed in ALL taxes. Today it has risen to 53.8%; and will hit 60% in the 2040’s at this trajectory. With so few net contributors it is unrealistic to expect a reducing minority of wealthy people to sustain everyone else.Altior said:

Not really in my opinion, although many people don't like to look at it that way, the state pension is part of the welfare framework. Welfare should be the last resort.Mustbeananswer?? said:

Thats deffo a bit harsh Alitor...Nobody knew what life was going to throw at people.Most of us have had to Duck and Dive a bit to get to this point???Altior said:

Surviving is enough if people expect others to fully fund their lifestyle. They have had 40-50 years of adulthood to prepare for this stage of their life.badmemory said:With no debts & no mortgage then probably yes. The real question of course is is surviving enough. Then as you age & maybe not as nimble as you were are you likely to need a gardener or cleaner to help out. What happens when cooking from scratch every day becomes a problem. But a better chance on the new state pension than on the basic state pension

There is no miracle, no fantasy, no magic wand. If the state pension was high enough for people to live comfortably, and allow for discretionary spending then lots more people would not bother saving up/ build up capital to sustain their lifestyle in retirement, and expect others to pay for it.

Also how do you think people should take less services? Not get ill so they don't use the NHS? Not work out so they don't use the council gym?Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.0 -

It’s pretty simple actually. Means testing will consider all your assets and taper SP accordingly. The more you have, the less you get.Linton said:BlackKnightMonty said:

There is no skew. This is a lot of pensioner households who can afford not to receive the SP. And thereby boost the SP for others. They might need an equity withdrawal plan, but that’s quite a simple solution.SouthCoastBoy said:

That's looks to be household wealth so numbers will be skewed, also I assume that includes all assets, e.g. property which isn't particularly useful as you need to live somewhereBlackKnightMonty said:

It’s from the IFS, here:Linton said:

I am sure that you would not want to mislead your readers. I cannot find a reference for the 1/4 of retired peope being millionaires you quote but it would seem that the figures are in wealth/household not per person. However if your look at https://www.nimblefins.co.uk/savings-accounts/average-household-savings-uk you will get a clearer picture:BlackKnightMonty said:Mustbeananswer?? said:

Disgrace....even after a good hike upwards .....In 2024-25, the full level of the new state pension is £221.20 a week or £11,502.40 a year.Pensioners are not given enough just to survive (If they have no other Occupational Pensions in place they are £2500 behind the eight ball) No wonder we have 1.5 million Pensioners in debt Come on England...give us a break ??GibbsRule_No3. said:My SP just about covers my HA rent, as I live in a London Borough, it does not cover my Council Tax, so I'd say no. I do have other pensions and am still working, nearly 70, my choice, for two days a week. Went to a Pension talk last week and they reckon to survive you need £14,000, fairly comfortable was £30,000 and very comfortable was over £40,000 this was based on one person, they did say you did not need to double those numbers for two people. At present with working pay I am just a bit over fairly comfortable and when I stop I won't be as low as surviving, thanks to the other pensions already in payment.And a quarter of all pensioners are millionaires.

Maybe we should means test it and then only those with no other pension provision, or those whom have not been able to make any other retirement provision could obtain a higher SP; perhaps quadruple locked to the NMW/NLW?

Does that sound fair?

For people of age 65+:........

I) The statistics here are in wealth per person, not wealth per household.

2) The wealth includes net value of house. Obviously people who have been paying off mortgages for perhaps and 30 years are going to have much higher net worth of houses than those who have only being doing this for 10 years.

3) The wealth also includes the value of non-state pensions in payment. Clearly a pension that is going to last you say 25 years is going to amount to a large sum of money.

4) Also included is the value of assets such as cars, furniture, ornaments, jewelry etc etc. But one accumulates stuff over the years so the older you are the greater value of stuff.

5) The average liquid wealth eg savings and non pension investments amounts to about £39,200. So hardly rolling in money. Again this is after a lifetime of work.

Now looking at the median annual gross income for people aged 65+ given in: https://www.gov.uk/government/statistics/distribution-of-median-and-mean-income-and-tax-by-age-range-and-gender-2010-to-2011. This gives a figure of about £22K, similar to the minimim wage. This is less than during any 5 year period in the age range 26-64.

Again your story about OAPs living in luxury at the expense of younger people is simply not demonstrated by the statistics.

https://www.if.org.uk/wp-content/uploads/2022/06/pensioner_millionaires_FINAL.pdf

Not such a simple solution. Equity release in your 70's is limited to about 1/3 of the value of the house. The current average house price is £264K, so you are talking about a lump sum of around £80K-£90K. Hardly enough to give your household £11K/year or more likely 2X£11K per year income to replace SP. Plus ER companies are not prepared to lend money on every house.

Buying an annuity at around 70 equivalent to SP inflation linked until death would cost around £200K/person. According to the ONS as quoted by Nutmeg the average pension pot at 55-64 is currently £107K so being able to afford to pay for SP and still generate sufficient income left to live a reasonable basic life style would be way beyond the means of the large majority of pensioners.

Perhaps circumstances may be different in say 40 years time when the changes to pensions brought in over the past 10 years will be having a significant effect on pensioner wealth but in a much shorter time perod, no way.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards