We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Just looking for some clarity on DMPs

Comments

-

Personally I think insolvency is an option but not one to rush into.

We can discuss treatment of beneficial interest at a later date0 -

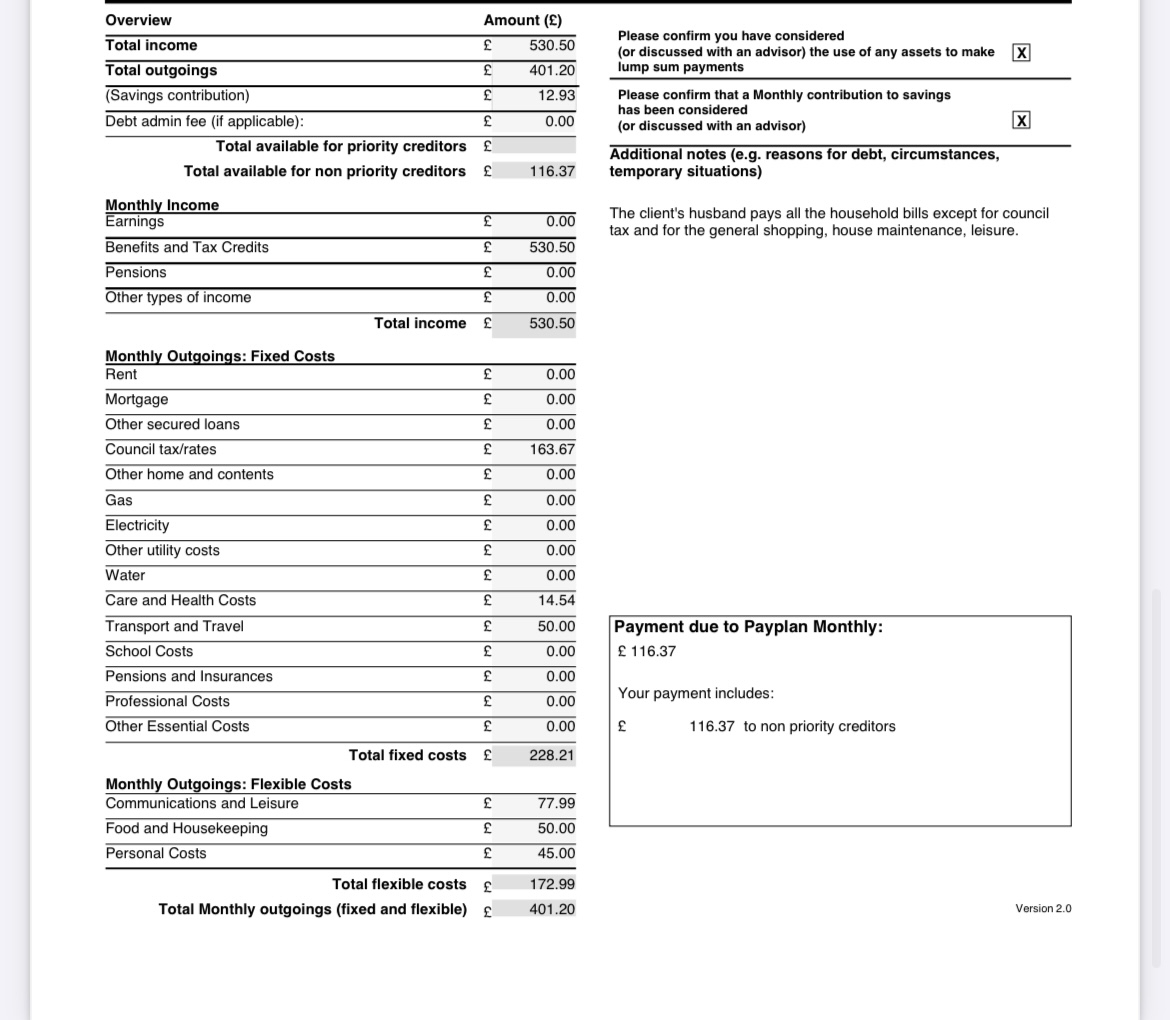

Thank you everyone for your responses.Ok so I spoke with a PayPlan advisor yesterday and she is advising either bankruptcy or Iva but she’s suggesting bankruptcy if the better option. She believes that creditors cannot prove a beneficial interest in my home as its solely owned by my husband, I never paid towards the deposit, never contributed to the mortgage, yes I’ve paid council tax on and off but she said that’s not enough to claim beneficial interest. My husband has never said verbally or in writing that I have a beneficial interest.I’m taking scared about backstory, I’m visiting my local CAB today.The PayPlan officer noted my income, she included carers allowance , child benefit for 1 child which will expire this December, plus council tax reduction, then she deducted expenses came out with a figure of £116 left after essential expenses to go towards debt . She never included my husband’s income but she accepted that my expenses were taken care of by him so didn’t add things like utility bills as expenses that I have to pay.I’ve realised now that I didn’t include my eBay account where we buy and sell items regularly. I know it’s not a proper job but we do make circa £500 a month ( my husband mainly sells in that account but the payment goes into one of my bank accounts which is solely for eBay - we set it to so that we can do a tax return if they ask for it)

ok so I’ll add that to my income but I must admit I was very frugal in my expenses because I was worried I’ll have nothing left for debt repayment.Realistically I think I’ll have £ 350 left then that will reduce to £250 after December.Does that make Iva a better option to bankruptcy

regarding telling my husband, I am considering this, I think it will proper break his heart but that’s something I will have to live with, but in rant to get all the advice first so I can assure him that his assets are safe.Plus can you guys advise on Iva vs bankruptcy. I’ll let know what cab said after0 -

Here is her financial assessment, before the additional £500. I haven’t added my dental and optician expenses

0

0 -

Btw I don’t know why I was nuttymom before I signed in lol0

-

No, it won't. There is only a financial association if they have a joint financial product.gwynlas said:I cannot advise you of how to live your life but your name will be connected by marriage and address to that of your husband so will affect his credit score.

I agree with those that have advised that the husband must be told. Apart from the stress and mental anguish that the OP will undoubtedly suffer from not sharing the burden, one way or another this will impact on the whole family so he has a right to know.0 -

sonnet72 said:Btw I don’t know why I was nuttymom before I signed in lol

I suspect you have multiple accounts for MSE as well.

Anyway, IVA or Bankruptcy, as advised previously, you have insufficient income for an IVA, and no asset to protect, despite what Pay Plan may tell you, your creditors would never agree to it, you need 75% of creditors by percentage of debt, to agree to it, and I don`t think they will.

I would say from experience it would be a waste of everyone's time trying to get that one off the ground, bankruptcy is the only viable choice in your circumstances.

But don`t rush into it, I would try the write off route first, see how that pans out, keep bankruptcy as a last resort rather than a first response.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

Thank you but what’s the right off route?0

-

Ok I know I’m not as clued up as you guys . But this is what I’m thinking. If , actually when I add the additional £500 as my income that makes my total income £1030.50, take off the expenses which stands at £401 on that sheet but I’ve excluded some medical expenses thinking I can do without plus some others-my expenses should be around £630 leaving me £ 400

now my debts WITHOUT interest come to £48k

so, if you divvy the actual amount without interest by 72 months- 6 years it comes to £666

ot over 5 years it comes to £800

so even in the 5 year scenario if I pay back £400 a month that’s at least 50% back to them, better than nothing if I went bankrupt0 -

No you are still not thinking straight, It won't worksonnet72 said:Ok I know I’m not as clued up as you guys . But this is what I’m thinking. If , actually when I add the additional £500 as my income that makes my total income £1030.50, take off the expenses which stands at £401 on that sheet but I’ve excluded some medical expenses thinking I can do without plus some others-my expenses should be around £630 leaving me £ 400

now my debts WITHOUT interest come to £48k

so, if you divvy the actual amount without interest by 72 months- 6 years it comes to £666

ot over 5 years it comes to £800

so even in the 5 year scenario if I pay back £400 a month that’s at least 50% back to them, better than nothing if I went bankrupt

No use putting amounts without interest you need to total up the actual balances.

You can't afford to live on nothing for 5 years, you would be depriving your children and it is not on.If you go down to the woods today you better not go alone.0 -

From Sourcrates's post on page one: "writing to your creditors detailing your situation, and asking them to make a commercial decision and write off what you owe them, as you simply cannot afford to do anything else."sonnet72 said:Thank you but what’s the right off route?1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards