We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

First Direct 7% con

Comments

-

Up to £300pm. It could be £250Bigwheels1111 said:Organgrinder said:I'm a maths teacher and might use this as a test question.

Last Direct advertise a savings rate that pays 7% interest per annum. You are allowed to pay £250 into your account each month. John says at the end of the year he'll have earned £210 in interest. Explain why John is incorrect.£300 a month.HSBC is £250I consider myself to be a male feminist. Is that allowed?1 -

I only had 13 this year, all RS maxed out.surreysaver said:

Up to £300pm. It could be £250Bigwheels1111 said:Organgrinder said:I'm a maths teacher and might use this as a test question.

Last Direct advertise a savings rate that pays 7% interest per annum. You are allowed to pay £250 into your account each month. John says at the end of the year he'll have earned £210 in interest. Explain why John is incorrect.£300 a month.HSBC is £250

Can’t wait to renew as many as possible.

Don’t see the point if not maxed out, those that are over 5.5% that is.0 -

Since everyone has already pointed out the OP's mistake (I swear this thread comes up every week), I think I'll try add something else useful - how to double check it yourself (though most regular savers already tell you what interest you should expect to receive on the product page).

The easiest way would be going to a calculator site, for example: https://www.thecalculatorsite.com/finance/calculators/compoundinterestcalculator.php

Then enter: Initial investment £0, interest rate 7% yearly, years 1, deposit amount £300, deposits made at beginning, compound interval yearly. If you've typed it in correctly, it yields £136.50 in interest.

If you want to try calculate it yourself in something like Excel, you could open a blank spreadsheet and:

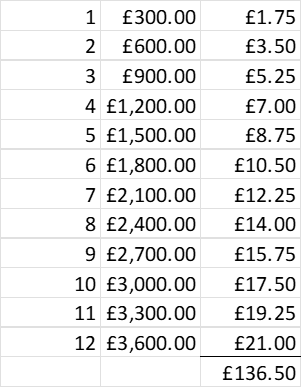

1. In cell A1:A12, enter the month number. E.g. A1 = 1, A2 = A1+1, and drag it down to A12

2. In cell B1:B12, enter the balance. E.g. B1 = £300, B2 = B1+300, and drag it down to B12

3. In cell C1, enter the interest generated each month. E.g. =FV(0.07/12,1,-B1,0,1)-B1 and drag it down to C12

4. In cell C13, enter =SUM(C1:C12) to show the interest total.

This clearly shows you the interest earned in each month (I've linked below just to make sure we're on the same page).

As you can see you earn £21 in interest only in the twelfth month because it's the only month you have the full £3,600 in the account. If you had £3,600 in the account for all 12 months, only then would you would earn 12x£21 = £252 (which is 7% of £3600).

Lastly, as an even quicker but less accurate method (and as people have said in this thread), as your balance goes from £0 to £3600 over the year, you could take the value in the middle as the average balance (£1800) and apply 7% to that, 1800 x 0.07 = £126.

Know what you don't1 -

No, calculating interest and compounding interest (effectively paying it while the product is open) are two completely different things. This account does not compound interestdanny13579 said:surreysaver said:There's not going to be any compound interest because it doesn't pay interest monthly

Is this not compound interest?

Know what you don't0 -

99% of the time they don't respond, but you get the odd 1% who come back to double/triple down.Zanderman said:

Not least as, in many similar previous cases, the OP may never respond so we don't even know if our multiple and multi-corrected efforts are worth it.MisterMotivated said:I find if funny how, in these threads, so many people feel the need to explain clearly how regular savers work and that the OP has misunderstood, despite the 5+ posts before theirs all explaining clearly how regular savers work and that the OP has misunderstood

I'm only commenting because I'm bored ^^Know what you don't0 -

It depends where else the money is. 5.5% in a regular saver is equivalent to 4.4% after tax if you've exceeded your PSA. In which case its worth maxing out an easy access ISA first. All depends upon your own personal circumstances.Bigwheels1111 said:

I only had 13 this year, all RS maxed out.surreysaver said:

Up to £300pm. It could be £250Bigwheels1111 said:Organgrinder said:I'm a maths teacher and might use this as a test question.

Last Direct advertise a savings rate that pays 7% interest per annum. You are allowed to pay £250 into your account each month. John says at the end of the year he'll have earned £210 in interest. Explain why John is incorrect.£300 a month.HSBC is £250

Can’t wait to renew as many as possible.

Don’t see the point if not maxed out, those that are over 5.5% that is.

I stopped opening regular savers until the beginning of this tax year for tax reasonsI consider myself to be a male feminist. Is that allowed?1 -

PSA doesn’t really apply to me.surreysaver said:

It depends where else the money is. 5.5% in a regular saver is equivalent to 4.4% after tax if you've exceeded your PSA. In which case its worth maxing out an easy access ISA first. All depends upon your own personal circumstances.Bigwheels1111 said:

I only had 13 this year, all RS maxed out.surreysaver said:

Up to £300pm. It could be £250Bigwheels1111 said:Organgrinder said:I'm a maths teacher and might use this as a test question.

Last Direct advertise a savings rate that pays 7% interest per annum. You are allowed to pay £250 into your account each month. John says at the end of the year he'll have earned £210 in interest. Explain why John is incorrect.£300 a month.HSBC is £250

Can’t wait to renew as many as possible.

Don’t see the point if not maxed out, those that are over 5.5% that is.

I stopped opening regular savers until the beginning of this tax year for tax reasons

I only get carers allowance 4k a year.

Although I’m getting close to the limit of £18.570 due to interest.

I make my money work as hard as I can.

Fixed rate bonds for 5 and 7 years.

2 nice three year ISA,S

Emergency fund and yearly interest was kept in Santander at 5.2%.

Now Chip 5.1% isa.

On the first of the month 12 regular savers pay, 3k in total.

As I use FD I can be overdrawn until 23.45pm that day without and fees.

I let FD pay them all.

So I make a manual payment at some point in the day to stay in credit.

This maxes my interest and rates.

I want more regular savers but not enough have higher rates.

Plus I’ve completely run out of spare cash.

In a real emergency I can raid one isa as fee is only £400 for 20k.

Works for me.

I would be horrified if I had to pay tax again

0 -

Though it's never been proven he said it or indeed, one of the many variations of the supposed statement*. No written documentation of this statement was ever done during his life, he died in 1955 but the first recorded report of this statement was in 1983 in the New York TimesColdIron said:AmityNeon said:ColdIron said:danny13579 said:surreysaver said:There's not going to be any compound interest because it doesn't pay interest monthly

Is this not compound interest?

No. Compounding only happens when interest is credited to the account and is able to compound. In this case the interest is only added at the end of the term. That's why the AER and Gross are the same

That's rather peculiar wording from FD though, as if to imply 'interest earned on previous days' is a separate element to the account balance allowing for compounding, despite the matching rates.

Yes, I agree, poor wording. However the mechanics of compounding have been plain for centuries if not longerAlbert Einstein called it the eight wonder of the world“Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it."

*the greatest invention in human history"

"the greatest invention of mankind,"

"the greatest invention of all,"

"the most significant invention of the nineteenth century"

"the most powerful force in the universe,"

"more complicated than the theory of relativity."Sam Vimes' Boots Theory of Socioeconomic Unfairness:

People are rich because they spend less money. A poor man buys $10 boots that last a season or two before he's walking in wet shoes and has to buy another pair. A rich man buys $50 boots that are made better and give him 10 years of dry feet. The poor man has spent $100 over those 10 years and still has wet feet.

2 -

I did ponder at one point opening lots of regular savers to push most of my cash in over the first couple of months, then reducing the contributions to the minimum, which would actually gain more interest than maxing them.Bigwheels1111 said:

I only had 13 this year, all RS maxed out.surreysaver said:

Up to £300pm. It could be £250Bigwheels1111 said:Organgrinder said:I'm a maths teacher and might use this as a test question.

Last Direct advertise a savings rate that pays 7% interest per annum. You are allowed to pay £250 into your account each month. John says at the end of the year he'll have earned £210 in interest. Explain why John is incorrect.£300 a month.HSBC is £250

Can’t wait to renew as many as possible.

Don’t see the point if not maxed out, those that are over 5.5% that is.

(In the end, there were so many hoops of direct debits and pushing money through current accounts to open them all for fairly small gains that I just stuck with the ones that took minimal set up effort).

Bit surprised tbh that you can satisfy all the requirements with £4k take-home!Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.0 -

He also said it was OK to quote him if it was to make an important point

") 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards