We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Ulster Bank will not recognise Lasting Power of Attorney from England

Comments

-

blackbirdsinging said:There are 2 issues, the legal status of LPoAs within different countries of the UK, and the situation of Ulster Bank specifically. I have had a much more helpful response from the FCA.Looking at the FCA of registered companies, there is no independent firm called Ulster Bank registered to provide financial services. There used to be, but no longer.Nat West trade with 10 separate names, one of which is Ulster Bank, and NatWest is clearly a London registered company. I do not think Ulster Bank are now in any position to refuse to accept an English LPoA and insist on a NI registered LPoA, given that they are a London company. The FCA say I should write to NatWest, which I intend to do.That is interesting. I didn't realise Ulster Bank was now just a trading name of Natwest. I thought it was a separate company, like Royal Bank of Scotland plc is separate from National Westminster Bank plc.From the Ulster Bank FCA page:

and from the Ulster Bank Limited annual report prior to that lodged at Companies House:

and from the Ulster Bank Limited annual report prior to that lodged at Companies House: So this a was relatively recent change. Perhaps the person you spoke to was not up to date on developments.0

So this a was relatively recent change. Perhaps the person you spoke to was not up to date on developments.0 -

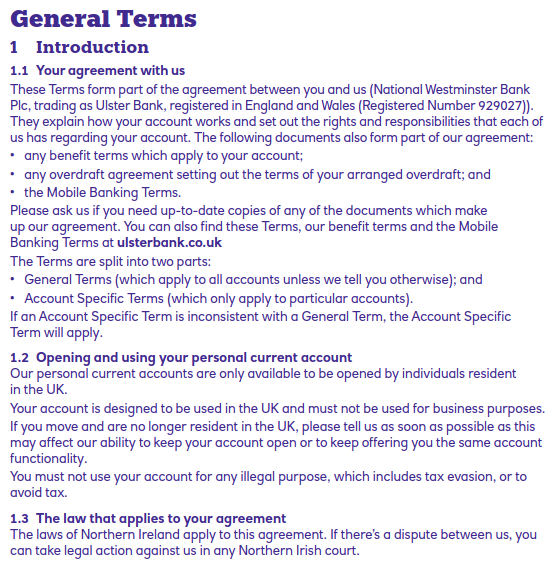

Yep, looks like even since Natwest acquired the business of the now defunct Ulster Bank Limited and is named as a party to the agreement, the governing law clause has not changed (1.3 in this agreement):

This is different than, say, Virgin Money (Clydesdale Bank for the time being), mentioned earlier in the thread, whose governing law clause states that it is dependent on the address of the customer when they enter into the agreement.0

This is different than, say, Virgin Money (Clydesdale Bank for the time being), mentioned earlier in the thread, whose governing law clause states that it is dependent on the address of the customer when they enter into the agreement.0 -

I'm glad we cleared that up, it would have been most unusual for the FCA to get something right!

3 -

I only discovered last year when dealing with matters for my Mother in Law using a newly granted POA that financial organisations are not obliged to honour a POA! This was a small but fully accredited and regulated bank and when I checked with the Prudential Regulation authority I was told that although it is relatively uncommon the bank was not compelled to work with a POA.0

-

I am not convinced things would not be a clear cut as the above posts state. Reproducing the bank T & Cs does not mean they are automatically correct - banks do make errors. The terms paraphrased from above are that the agreement is between myself and Nat West bank, trading as Ulster Bank, registered in London...." It then goes on to say that NI law applies. Why not Turks and Caicos Islands law?Seondly, their complaints procedure is via the FCA. They clearly think it is possible there is a different view than the posts above and is not clear cut.0

-

I think you are right but am going to ask a devil's advocate question.IanManc said:It is absolutely clear cut. The problem here is that your mother has opened and account in Northern Ireland and you won't accept that Northern Irish law applies to it. The UK legal jurisdictions are mutually exclusive. The laws of two (or more) of them can't apply to a single contract because each jurisdiction has different laws of contract and court systems. Ulster Bank has, quite reasonably, stated that the laws of Northern Ireland apply to its contractual relationships with customers and that's what your mother signed up to.

If an English person draws up a contract with another English person which says that it is governed by Turks and Caicos Islands law, would the other be able to sue in an English court or would they have to go to TACI? AFAIK they could sue in England because everyone involved in the contract is English, and the English courts are unlikely to uphold the clause which transfers jurisdiction to a completely unrelated country.

If a bank in Northern Ireland forms a contract with a customer is in England, then they have to pick one jurisdiction or the other and it is reasonable to pick NI.

But in this case, notwithstanding Ulster Bank's former location before it ceased to exist as an independent entity, we seem to have an English bank forming a contract with an English customer. So can the jurisdiction still be transferred outside the country they are both in?

I take your point that Ulster Bank as a brand has the majority of its business and branches in NI. But given that "Ulster Bank" is offering best-buy rates to the whole of the UK, from its office in Bishopsgate, London, is that still a strong enough argument to prevent a recently formed contract between an English bank and an English customer being governed in an English court?

@OP: FAOD I agree with the above, your mother should either register a Northern Irish POA if she wants to continue forming contracts that say NI law applies, or move her money. The discussion above is academic because assuming she still has capacity, it will be much easier to create a Northern Irish LPOA than get the courts to force NatWest to comply with an English one.

If she does not have capacity you will presumably have to apply to Northern Ireland's Office of Care and Protection for authority to manage her affairs in Northern Ireland. (So you would be going to court anyway and it would be sensible to take the less contentious route.)

That is news to me, as my understanding is that an instruction given under an LPOA is legally as good as one from the donor - which is the entire point. Even if it came from the PRA I would want a bit more than their word for it.torchie said:I only discovered last year when dealing with matters for my Mother in Law using a newly granted POA that financial organisations are not obliged to honour a POA! This was a small but fully accredited and regulated bank and when I checked with the Prudential Regulation authority I was told that although it is relatively uncommon the bank was not compelled to work with a POA.

I also wonder if the bank wasn't refusing to acknowledge the POA as such, but doing something narrower in scope such as declining to offer online banking (which they aren't obliged to), or insisting on seeing the LPOA itself rather than accepting the online code.

If a bank failed to honour an LPOA without good reason I would be taking it to the Financial Ombudsman, not the PRA.0 -

This is the simple and sensible answer to the situation.

You've been told how to register the Power of Attorney in order to make it operative in Northern Ireland. If you don't want to do that then either let your mother operate the account herself - which one would think she is capable of doing, seeing she recently opened it - or get her to close it.3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards